India is experiencing yet another power crisis. In the last week of April, the daily peak power shortage rose to 10,778 megawatt (MW). Power deficits reached 5% of overall supply at the national level, while a few states experienced steep deficits ranging up to 15%. To deal with the scarcity, distribution utilities (discoms) resorted to loadshedding — rationing supply hours for households and economic activities, usually unannounced. Such power supply disruptions not only hurt economic activities and productivity, but also impinge on essential services and human well-being.

Though India claims to have achieved power adequacy (officially, the annual national power deficit has been below 0.5% for the last six years), periodic shortages remain a predictable phenomenon. Coal fuels more than 70% of the electricity generated in India. Monsoon-induced coal production slowdowns and consequent power shortages are more or less annual events in India. Since 2006, there have been 10 instances when more than 50 power plants reported critically low coal stock. India experienced such a power crisis in October 2021.

However, an early summer power shortage is unprecedented. While the situation may appear to have improved in May with a small drop in demand and a ramp up in generation, the system is running under acute stress. 1As on 22 May 2022, total coal inventory at plant sites was 32% of normative stock, while non-pithead plants had only 24% of normative stock, and 106 plants were under the critical mark. As electricity demand is projected to grow, these shortages could occur more frequently through the year if they are not addressed adequately now.

What explains this early summer power shortage? How is it different or linked to monsoon shortages? As we answer these questions, we trace the structural roots of persisting power shortages in India. We analyse immediate government responses to the crisis and their consequences and identify priorities for a long-term solution that are consistent with energy transition.

Roots of the power shortage

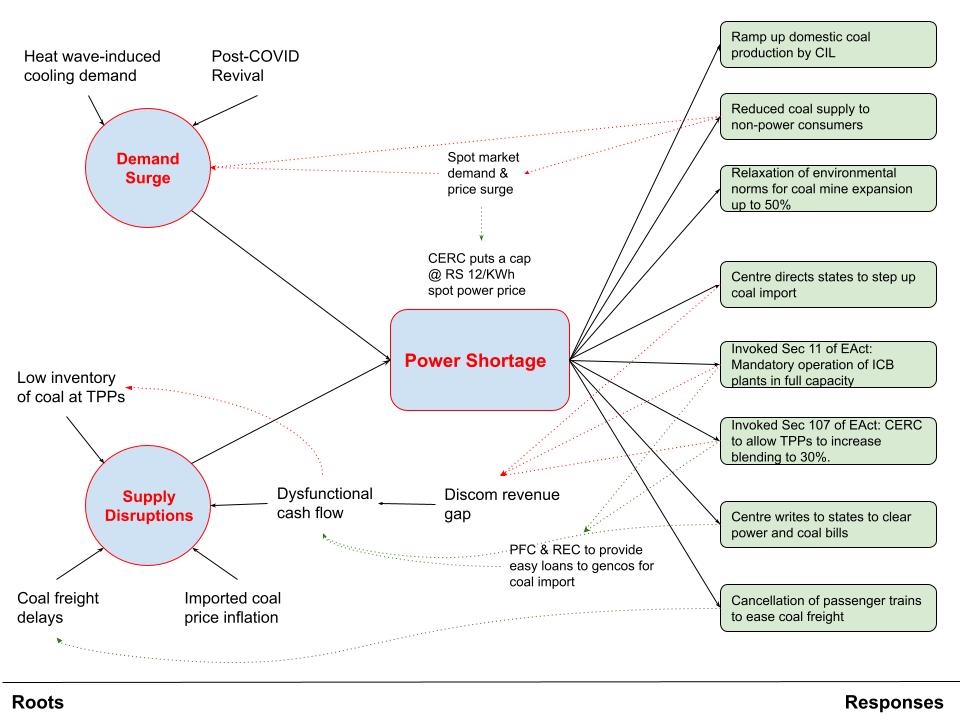

Simply explained, any shortage is a consequence of demand and supply mismatch. Electricity is no exception. The current power shortage is a combined effect of a demand surge and supply disruption (Figure 1).

A surge in demand for cooling purposes was caused by the heat wave and a revival of economic activities after Covid-19 disruptions. The daily energy requirement increased to nearly 4,800 million units (MU). The average daily energy requirement in April 2022 was 4,512 MU compared with 3,941 MU in April 2021, a 14.5% growth, while year-on-year demand growth is normally around 5%. Indeed, the growth in one month, from March to April 2022, was 6.5%.

Ideally, India could have managed the demand surge by ramping up generation. India’s 236 gigawatt (GW) thermal power plants (TPPs) had a plant load factor of 72% in April, significantly below their capability. Generation capacity was not the constraint.

Rather, the plants did not have an adequate inventory of coal to meet the power demand. While power plants are required to maintain a stockpile of 12-17 days at pithead plants and 20-26 days non-pithead plants depending on the month of the year 2Following the last shortage in October 2021, coal stocking norms were eased to reflect monthly electricity demand trend as well as domestic coal availability. Earlier, power plants were required to maintain a stock for 15-30 days, depending on their distance from mines, throughout the year. , on 21 April, the coal stock of 62% of the plants had fallen below the critical mark, with inventories of less than 25% of the normative stock. More than 50 plants had stocks below 10% of the norm.

In 2021-22, Coal India increased its production by 4.4% and increased its supply to the power sector by 21.4% to 540.4 MT from 445 MT in 2020-21.

Does this imply a coal production problem? The coal ministry has denied any shortfall in production. Coal India Ltd’s (CIL) production increased by 27.2% in April 2022 from a year ago. By the end of the month, CIL had a stock of 56.7 million tonnes (MT), enough to fuel all power plants for more than three weeks. In 2021-22, CIL increased its production by 4.4% and its supply to the power sector by 21.4%, to 540.4 MT from 445 MT in 2020-21. One of the few benefits of reduced railway passenger volumes during Covid-19 was the ease of transporting coal throughout the country.

A shortage of railway rakes partly explains why the coal stock at mines has not reached the plants on time. 3Railways pass the blame to private contractors at plant sites who use JCBs for unloading coal and in the process damage the interior of the wagons. Before the private operators, the unloading was done manually. Railways lists about 10,000 damaged coal wagons, and repairing each wagon costs Rs. 5 to Rs. 10 lakh. But the reason for not maintaining a normative stockpile at plants goes deeper. Discom leakages and their inability to recover costs have resulted in dysfunctional cash flow in the system. The outstanding dues of discoms to generation companies (gencos) are more than Rs 1 trillion. The cash crunch prevents gencos from procuring the requisite amount of coal on time — most mining companies, including CIL, require advance payment for any coal delivered. Thus, the chronic insolvency of discoms is transmitted to upstream supply chains.

Most of the country’s coal is mined in the eastern (Jharkhand, Orissa, West Bengal) and central regions (Chhattisgarh, Madhya Pradesh), but our power generation capacity, particularly in the last 20 years, has developed close to large industrial centres in states such as Maharashtra, Gujarat, Tamil Nadu, and Karnataka. Because of this spatial mismatch, hundreds of millions of tonnes of coal have to be moved from the coal belt to these areas via road and rail. For this supply chain to work properly, mining companies need to coordinate with coal transporters (road and rail) and consumers to ensure that the mined coal lying in coal yards is evacuated promptly.

This has been a perennial problem in India over the last decade because most power generators work under tight financial pressure and cannot pay for months of coal in advance. In the 1990s, when most mining, power generation, and distribution was with the governments, such financial issues would often be resolved behind closed doors, where different arms of the state would trade favours with each other. CIL would supply coal in advance without payment and National Thermal Power Corporation (NTPC) would supply power in lieu of promises for future payment. While such deals still happen, it is much more difficult for CIL and the NTPC to justify such forbearance, given that they are publicly listed companies and profit motivates them much more than it did three decades ago.

The present power crisis was further exacerbated by disruptions in international commodity prices across the board (oil, coal, gas, metal, and so on). Imported coal prices have gone up almost three times in the last year and have more than doubled since the start of the Russia-Ukraine war. India annually imports more than 150 million tonnes, equivalent to 20-25% of the coal used for power generation. These imports are split between power plants built specifically for imported coal (17.6 GW) and power plants running primarily on domestic coal, which blend small amounts of imported coal (10%) to improve plant power output (72 GW).

The higher costs of imported coal cannot be easily passed onto consumers in normal conditions. This was the reason why many of the Mundra-based private power plants ran into serious financial trouble.

Since the majority of India’s power capacity is in the form of long-term power purchase agreements (PPAs), the price of most power in this country is regulated and revised only once every two or three years. The higher costs of imported coal cannot be easily passed onto consumers in normal conditions. This was the reason why many of the Mundra-based private power plants ran into serious financial trouble. When Indonesia increased its coal prices in the mid-2010s, it destroyed the unit economics of many power plants, which had not anticipated a fuel cost escalation while bidding for these projects.

Regulated markets always struggle to deal with such unexpected increases in input prices. Not surprisingly, after commodity prices began rising in March 2022, many of the imported coal-based power plants have preferred to either not run at all or run at very low levels — they would lose money for every unit of power produced. Inflation in imported coal and gas prices has also contributed to captive power generators shutting down generation and switching to the spot market. By late March, spot prices in the power exchange hit Rs 20 per kilowatt hour, the prevailing ceiling price.

The power shortage points to a lack of effective resource planning by distribution utilities or discoms. Resource planning is used by discoms to meet the forecasted peak demand and total energy requirements of all their customers. Instead, given a legacy of shortages, political and economic expediencies have historically determined whose lights stay on in India. Even with adequate capacity, utilities have failed to undertake the resource planning that allows them to keep everyone’s lights on, even in times of shortage.

Figure 1: Causes and State Responses to Power Shortage in India

Reactive state response

The power crisis has received serious public, media, and political attention. The union home minister held a meeting with the ministers of power, coal, and railways to take stock of the crisis and discuss measures to ease the situation. The union government has taken multiple steps to manage the power shortage crisis (Figure 1). In this section, we look at what has been done and what its consequences will be for India’s power sector.

First, to ease the disruption in supply, CIL ramped up its production and increased supplies to power plants. Despite outstanding dues from a number of gencos, CIL registered a 16% growth in supplies to power plants in April 2022, compared with April 2021. Second, in a complementary measure, the environment ministry eased norms for expanding mining, in order to achieve higher production. Mines that have been granted an expansion of 40% can increase their production by 50% without public consultation or an environmental impact assessment. Third, Indian Railways cancelled multiple passenger trains (42 trains for 20 days, amounting to nearly 1,100 trips) to facilitate movement of coal from mines to plants. Fourth, the increased coal supply to power plants came at the cost of cutting down supplies to non-power sector consumers, including captive power plants. Fifth, the centre wrote to the states pointing out how lack of basic payment discipline was causing supply problems. It asked them to clear their outstanding dues to gencos and coal companies. Simultaneously, the power ministry is working on a scheme to liquidate the outstanding dues by allowing the discoms to pay their dues to gencos in up to 48 monthly instalments without any late payment surcharge. 4The ministry estimates that discoms can save around Rs. 198.33 billion on late payment surcharge. Finally, the Central Electricity Regulatory Commission (CERC) has proposed to impose a deterrent charge on power plants for failing to maintain normative coal stock. The commission, in a staff paper on computing deterrent charges, seeks to penalise the defaulting plants by reducing their annual fixed charges.

While the centre claims there is no shortfall in domestic coal production and has taken measures to ramp up production and transportation in the short term, it is also pushing hard to increase coal imports. It first urged the states to step up coal imports and build inventories to meet power demand until 2025, which is when private mines will start production. Subsequently, emergency provisions of the Electricity Act 2003 have been invoked to make uptake of imported coal binding on utilities and states.

Anticipating a further surge in electricity demand and a peak demand of 220 GW through the summer months, the centre has invoked Section 11 of the Electricity Act, which allows the government to compel companies to operate and maintain their power plants in accordance with its directions. This is targeted at the 17.6 GW imported-coal-fired plants, of which only 10 GW are operational at a low capacity utilisation because of lack of compensation for imported coal or because some plants are under bankruptcy proceedings. The government has also constituted a committee to determine the benchmark tariffs for power generated through high-cost imported coal. The centre has invoked Section 107 of the Act, directing the Central Electricity Regulatory Commission to allow power plants to blend up to 30% imported coal until March 2023 without seeking the consent of their buyers. Simultaneously, it has set a deadline of 31 October 2022 for the states to place orders for the 10% imported coal required for blending. Defaulters will be penalised by an increased import requirement of 15%.

While the Centre claims there is no shortfall in domestic coal production and has taken measures to ramp up production and transportation in the short term, it is also pushing hard to increase coal imports.

On directives of the centre, state-owned banks and non-banking financial companies (NBFCs, like the Power Finance Corporation [PFC] and the Rural Electrification Corporation [REC]) are lined up to lend to power plants across the country to help with their working capital requirements to import coal. While these measures may bring life to some stressed power plants, not all of them are satisfied with the temporary new tariffs notified by the government committee, which still may not cover all their costs.

These immediate measures taken by the centre are wide ranging and demonstrate the value placed on energy security. However, these responses are largely reactive, and seek to address only the symptoms of deep and structural fault lines. While some of these steps are justifiable as immediate responses, the solutions do not pay attention to long-term remedies, contradict the long-term vision of the sector, and exacerbate the sector’s challenges in many ways.

Increased infusion of imported coal has serious cost implications. For example, a 30% blending requirement is projected to inflate the unit cost of those plants by up to Rs 1.50.

First, prioritisation of coal imports as the primary strategy is at odds with the central government’s vision of reducing coal imports to make India energy self-reliant. Among other consequences the U-turn brings in policy uncertainty to a sector that is heavily dependent on private and global investments.

Second, the solution will likely exacerbate the problem. Increased infusion of imported coal has serious cost implications. For example, a 30% blending requirement is projected to inflate the unit cost of those plants by up to Rs 1.50. This, in turn, will worsen the liquidity crisis for discoms, whose ability to recover costs is already limited. It will inflate their outstanding dues to gencos, which are already at the centre of the crisis. If the discoms manage to pass these costs on to customers, it will inflate electricity bills for all, including the poorest, and may thus affect energy access security.

Third, while a shortage can also be addressed by managing end use, all the responses are directed at ensuring supply adequacy. Some advisories and pushes towards demand management and responsible electricity usage during the shortage would have had no extra cost.

Why governments respond in a reactive fashion and choose short-term solutions can be explained by the political incentive structure. Periodic power shortages and their management have been opportunities to leverage political legitimacy. At every instance of a power crisis, states blame the centre’s inefficiency in coal allocation and dispatch; the centre blames states’ inability to pay upstream suppliers; and opposition parties blame misgovernance and mismanagement by the ruling parties. The result is always band-aid solutions to suppress the crisis, not answers that will fix structural fault lines.

Towards a long-term solution

The risk with the current, short-term approach is that we may lose the opportunity to pay for a long-term shift in risks to the power sector. Early summer power shortages are unprecedented, but not necessarily unforeseeable, and may be part of a future pattern. The annual power shortage could turn into a prolonged season of scarcity. Structural solutions to address the persisting power shortages are not only complex and long-term, but also aligned to conditions for a transition to a 21st century energy system.

There are a few priorities to keep in mind while headed in that direction. First, while coal’s share in India’s energy mix will see a gradual drop, there is no doubt it will dominate India’s power generation for the foreseeable future. It is important to ensure adequate infrastructure and enabling ecosystems for the optimal use of India’s only plentiful fossil fuel resource. For example, a dedicated freight corridor has been considered to ease transporting coal. One hopes this project finally sees the light of day.

Markets are not sufficient to run the ecosystem, especially given that the legacies of state intervention persist in the sector.

Second, actors in the coal-power value chain always bicker while trying to make a profit somewhere. Without external intervention, a spirit of cooperation is not clear or present between these actors, fighting for their own survival in India’s commercial and bureaucratic ecosystem. Consequently, inter-ministerial committees, the Prime Minister’s Office (PMO), and sometimes the Cabinet Secretariat have had to coordinate to ensure that coal is mined, transported, and used in power plants without much friction. Without some kind of cooperative federalism, this system can fall apart very quickly.

This coordination problem will become more complex over the coming decades as private participation in these spheres increases. 5Private and commercial mining is supposed to grow quickly over the next decade. Almost 20% of domestic coal moves by road on trucks run by private transporters, and smaller private generators often get the short end of the stick when it comes to timely coal supply or payment by discoms. Markets are not sufficient to run this ecosystem, especially given that the legacies of state intervention persist in the sector. It needs professionals who work exclusively on logistics and inter-agency coordination to make sure that the system keeps running smoothly. While such professionals exist in many agencies (Coal India, Indian Railways, the coal ministry, NTPC, and the like), it does not seem like the central coordination role has been working well lately — firefighting seems to be more common than proactively solving problems. To ensure that such shortages do not become a fixture of Indian summers, there needs to be a dedicated institution to address these problems.

Third, resource planning in the sector must evolve from predictable growth projections to prepare for uncertain demand and supply patterns. Even as energy transition disrupts demand and supply options, climate-induced extreme weather events will increase the stress on the system. Dealing with these uncertainties will require robust processes for resource planning at the utility and system levels, which factor in the effects of climate change and extreme weather events along with techno-economic changes.

Fourth, the economic viability of the electricity system, particularly the distribution business, has been a longstanding policy priority. Despite sustained interventions, commercial losses and insolvency have been persistent in electricity distribution, causing disruptions in the value chain. The urgency to make the electricity industry economically viable has been heightened by the growing need for private capital.

But putting cost recovery upfront, along with periodic bailout options, is misplaced. At the root, the poor finances of discoms are further affected by an unwillingness to pay for low-quality power. This vicious cycle must be broken by increasing the economic benefits of power and increasing the paying capacity of consumers. Moreover, given the persistent state of poverty in India and the recent Covid-19-induced spike in it, it is highly unlikely that subsidy pressures in electricity will be eliminated in the near future. These subsidy demands are largely concentrated in a few low-income states with limited fiscal space to meet these demands.

Having achieved the physical conditions for universal access, India should pivot to a “productive power” approach towards electrification, which empowers and enables the poor to pay for better quality service through productive use of electricity. India can thus achieve two objectives critical to distribution — economic viability and access security for the poorest. First, by boosting rural demand, and thus, bringing down per unit cost to supply. Second, by enhancing rural employment opportunities and household incomes, and thus augmenting people’s ability to pay for electricity.

Finally, what seems to be clear is that the electricity system is approaching an era of greater uncertainty. Coal-based power generation is not as reliable as it has been historically, particularly in the light of unpredictable international commodity prices and perennially unreliable domestic logistics ecosystems. At the same time, variability and intermittency-related problems will likely increase in the power grid as renewable energy starts making up a greater part of India’s power generation. Regulators and system operators will be essential to enabling a smooth energy transition, but we have seen how lack of coordination between market-monitoring entities can have disastrous consequences. We can only hope that the institutional response to these shortages instils a sense of cooperation among rival sectoral agencies.

Ashwini K. Swain is a fellow at Centre for Policy Research, New Delhi. Rohit Chandra is a visiting fellow at Centre for Policy Research and an assistant professor at the School of Public Policy, IIT-Delhi.

The real crisis facing India’s power sector