The 2020 pandemic hit two sources of constant engagement for the Indian public: cinema and cricket. Both are slowly reviving as we get used to the ‘new normal’. However, while they were missing, a totally unimagined source was providing drama and frenzy for spectators: Indian banking. In the memorable words of Bill Lawry, former Australian cricket captain turned commentator: “It is all happening here.”

The Indian banking sector had started buzzing much before the pandemic, with rising Non-Performing Assets, failures of commercial banks, failures of non-banks and housing finance companies, frauds, and mergers of public sector banks. During the pandemic, several big borrowers were not being able to repay loans, leading to loan moratoriums. There was the added masala of boardroom battles, as in Yes Bank, and of shareholders firing directors and promoters at Lakshmi Vilas Bank and Dhanlaxmi Bank. Even as depositors eyed banks with nervousness, there was a googly from an unexpected corner. A committee of the Reserve Bank of India (RBI) suggested that the central bank could consider allowing corporates to become promoters of banks, a controversial measure that has been opposed for a long time.

The Banking Regulation Act, 1949 continues to define RBI’s present-day policy […] this history shapes responses to the current crisis.

In all this drama, RBI has become the central point of discussion. Some have praised the central bank for intervening and protecting depositors’ funds, while others have criticised the central bank for not being proactive and for allowing failures to develop over time.

Most commentators have ignored the fact that RBI has taken these decisions based on the existing legal structure. The Banking Regulation Act, 1949 continues to define RBI’s present-day policy. In this piece, we analyse the evolution of banking regulation in India and reflect on how this history shapes responses to the current crisis.

Banking regulation in India: Learning through crises

Mark Twain famously said, “History does not repeat itself but often rhymes”. This is quite true when we compare banking crises over time not just in India but even across economies.

Banks fail due to a set of common microeconomics factors: low capital and reserves, greed for high profits, poor governance, and frauds. A common macroeconomic factor is that banking typically follows the business cycle. Banking grows sharply as the economy starts to grow, but as the growth cycle reverses there are high Non-Performing Assets (loans which have defaulted) and losses.

What makes each crisis unique is that the political economy and overall economic conditions vary across times.

Before the establishment of RBI in 1935, banks entered and exited the system freely without any regulation. Modern banks in India were initially governed under the Joint-stock Companies Act, 1857 and later by the Indian Companies Act, 1913. Imposing company law on banking left several regulatory gaps, which were quickly exploited by the banks. The RBI, after it was established, pointed out the need to have separate legislation for the sector as banking had its own idiosyncrasies.

The central bank had a steep learning curve from the two spectacular banking failures that changed the regulatory landscape.

The advent of RBI led to changes, but the central bank had a steep learning curve from the two spectacular banking failures that changed the regulatory landscape. The failure of the Travancore National and Quilon Bank (TNQ Bank) in 1938 was due to both political and economic reasons (RBI 1970). But the existing laws were not adequate for the RBI to be a lender of the last resort to the bank or to restructure the bank. Following this, the-then RBI governor James Taylor prepared a proposal in 1939 for legislation on the lines of acts in US, Canada, and select European countries. World War II and Independence delayed the acceptance of the proposal and the Banking Regulation Act had to wait till 1949.

The new act limited the use of ‘bank’ and allied terms to a specific set of institutions, prescribed minimal capital and reserve requirements, and banned the practice of common directors across banks and lending to directors. It also gave RBI powers of inspection over banks and to suspend operations of banks if they could not honour their debts.

The second crisis came in 1960 when RBI was shaken by the failure of the Palai Central Bank (RBI 1998). Like TNQ Bank, this bank too was from the erstwhile princely state of Travancore, which had by then become part of Kerala. Unlike in the case of TNQ Bank, RBI had more time to handle the crisis at Palai Central. It gave time to the bank management to resolve the concerns of misgovernance and bad loans. However, the bank management ignored RBI advice. The bank was large and its failure created a run on several such banks in Kerala.

Following the failure, in the mid-1960s, RBI got additional powers to enforce amalgamations and to quickly 'de-license' banks. Earlier, moratoriums were requested by banks, but now RBI could impose moratoriums. It could also force mergers of weak banks with stronger banks (a strategy RBI has used multiple times into the present). The government also instituted the Deposit Insurance Act in 1961 to protect savers’ accounts, which helped stall bank failures and infused confidence in the banking system.

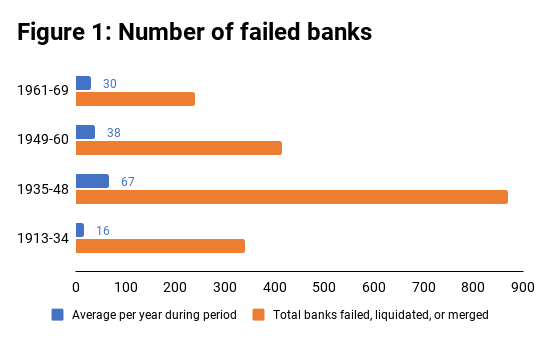

After the Banking Regulation Act, failures almost halved during the period 1949-60. The regulatory regime put in place following the collapse of the Palai Central Bank further lowered the number of failed banks.

These developments had a marked effect on bank stability. On an average 16 banks failed every year between 1913 and 1934, before the establishment of RBI. This increased four times to 67 during the period 1935-48. After the Banking Regulation Act, failures almost halved during the period 1949-60. The regulatory regime put in place following the collapse of the Palai Central Bank further lowered the number of failed banks.

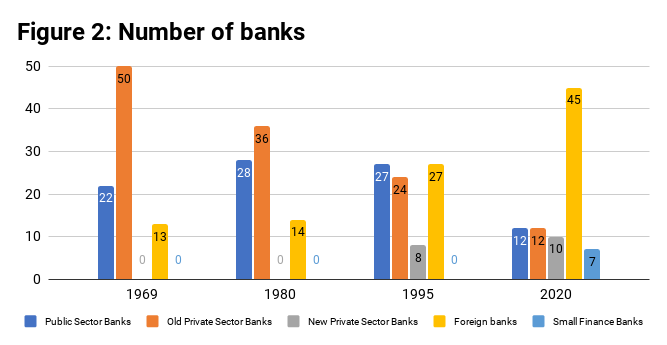

In 1969 and 1980, the government nationalised major banks and stopped licencing new banks. RBI also continued to weed out weaker private banks by merging them with larger ones. The number of private banks declined to 24 in 1995 from 50 in 1969. No new banks came up until after the economic reforms of 1991.

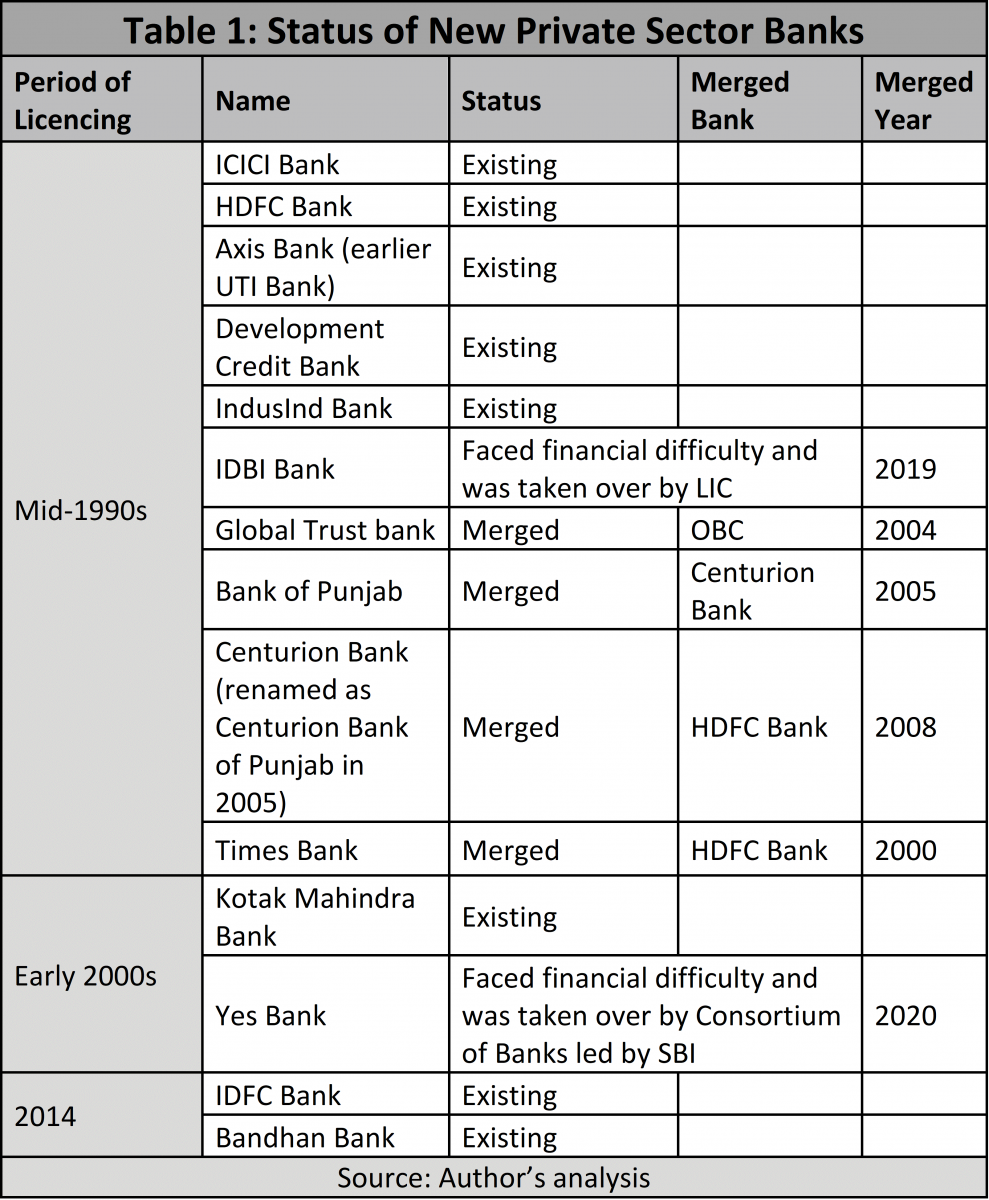

In 1994 the RBI licenced 10 new private sector banks. The experience with them has been mixed with both failures and successes. Five of them have had financial difficulties. Of the five, four were merged with other banks: Global Trust Bank (GTB), Bank of Punjab, Centurion Bank (renamed as Centurion Bank of Punjab in 2005), and Times Bank. GTB in particular led to infamy for both promoters and regulation. The bank was mired in lending to stockbroker Ketan Parekh, who was accused of manipulating the stock market. The fifth, IDBI Bank, was recently taken over by LIC but has continued to maintain its identity.

RBI licenced four more banks in the 2000s, including Yes Bank which last year was hit by a crisis and was taken over by a group of banks led by SBI. Overall, of the 14 new private banks licenced since 1994, four do not exist anymore and two others were taken over by other financial institutions and banks following financial troubles. So, we continue to have 10 banks in the new category.

Fast forward to today’s crisis

The current banking crisis also rhymes with previous crises.

The crisis is similar on account of microeconomic and business cycle factors. The reasons for failure too are similar to those in the past. Indian banking expanded significantly in the 2004-08 period, tracking high growth in the Indian economy. There was a minor blip due to the 2008 crisis. However, as the economy recovered quickly, the banking sector continued to grow. Slowing economic growth in 2012-2013 brought problems to light as NPAs began to rise. The NPA problem was revealed to be worser that expected after the RBI’s Asset Quality Reviews in 2015.

The difference this time is that the crisis is not limited to commercial banks. It started with public sector banks but has quickly engulfed cooperative banks, NBFCs and housing finance companies, and the new and old private banks. Each of these categories has its own story.

The new private sector banks are the biggest thorn in the current crisis. These banks were licenced amidst huge hype and expectations, yet nearly half of them have run into financial trouble.

In the high growth phase, public sector banks were pushed into giving loans to the infrastructure sector and industrial projects with long gestation periods. This was partly because the development financial institutions established to fund these activities, such as ICICI and IDBI, had been converted to regular banks. The push was also to showcase India’s potential as an investment destination where infrastructure plays a crucial role. Loans to these projects, which take long periods to complete and generate returns, worsened the banks’ assets-to-liabilities mismatches (the bulk of bank deposits are short-term deposits). Once the business cycle reversed and the UPA-2 government got mired in several scams, many projects were stalled. This led to rising NPAs at the banks.

The reversal of the business cycle was not the lone factor for PSBs’ woes. There were several cases of frauds and misgovernance. While this led to finger-pointing at RBI’s regulatory role, former RBI governor Urjit Patel in 2018 highlighted that RBI could do little to regulate PSBs. The finance ministry has had control over regulation and appointments at PSBS since bank nationalisation. This dual regulatory structure was problematic earlier as well but has shown its real weaknesses in the current crisis.

The weakness in cooperative banks is on account of another kind of dual regulation, where powers are divided between RBI and state governments. This had fed the usual villains of misgovernance and frauds. While RBI has been cleaning up the cooperative banks for a while now, the crisis at the large Punjab & Maharashtra Cooperative bank has led to renewed attention.

Old private sector banks suffered from a different dual problem: of promoters also acting as directors. Promoter-directors directed all major decisions in the bank, from appointing board members to employment to credit decisions. RBI has been cleaning up governance in these banks. But there is a long way to go, as seen in cases of Lakshmi Vilas Bank and Dhanlaxmi Bank, where the shareholders voted out senior management following crises.

But the new private sector banks are the biggest thorn in the current crisis. These banks were licenced amidst huge hype and expectations, yet nearly half of them have run into financial trouble. The case of Yes Bank was especially shocking as it was once a cynosure of Indian banking and boasted of profession management. In its failings though, Yes Bank resembled an old private sector bank where the promoter controlled everything around the bank.

Unlike other banking institutions, RBI had full powers to regulate and supervise Yes Bank. It is not clear how the regulator allowed the bank’s faults to emerge in the first place. It was ironical that a consortium led by State Bank of India, the oldest public sector bank, had to bail out one of the country’s newest banks.

The current crisis has elements of previous crises yet is different as it is more broad-based.

Large Non-Banking Finance Companies like IL&FS failed from misgovernance and from funding several dubious projects. IL&FS believed it was ‘too big to fail’, facing the same fate as Lehman Brothers which thought similarly. Smaller NBFCs suffered as banks were their largest source of funds. With banks in crisis, they restricted lending to NBFCs, almost a repeat of the 2008 crisis. Housing Finance Companies like Dewan Housing Finance Corporation failed for similar reasons as IL&FS. This sector was regulated by National Housing Bank, yet the blame was placed on RBI.

The above analysis shows how the current crisis has elements of previous crises yet is different as it is more broad-based. Both the central government and RBI have responded to the crisis in their own ways.

The government’s approach has been ad-hoc. It instituted a Banking Boards Bureau to appoint senior management of PSBs, but the finance ministry continues to intervene. The government infused capital in PSBs and merged smaller PSBs with larger ones to lower the number of PSBs to 12 from 27. To infuse confidence amidst depositors, the government hiked the deposit insurance on savings accounts to Rs 5 lakhs from Rs 1 lakh. RBI has been given more powers, including the regulation of HFCs and greater oversight of NBFCs. Dual regulation for cooperative banks may soon end. However, there is still no solution in sight for ending the dual regulation of PSBs.

The RBI has had several institutional changes. It is streamlining its regulation and supervision functions. The central bank is building a new cadre of specialized banking supervisors to look at risks across different bank types and not see commercial, cooperative and NBFCs in silos. As risks transfer quickly across markets and banking types, it is important supervisors see risks similarly as well.

“The Reserve Bank's powers are not [...] a substitute for the efficiency and integrity of the managements themselves.”

RBI has also established a College of Supervisors “to augment and reinforce supervisory skills among its regulatory and supervisory staff.” The college is supported by an Academic Advisory Council comprising bankers and academicians to benchmark the supervisory practices with the best in the world. RBI has also issued a paper on improving governance in Banks and asked all banks to appoint a Chief Compliance Officer in their respective organisations.

Final thoughts

The current crisis is a reminder of two, often forgotten, aspects of banking.

First, banking crises are not new and come in different shapes and sizes. They can surprise you even when the economy is doing well, in the 2008 crisis in case of global banks and the post-2008 crisis in case of Indian banks.

Second, regulation evolves with developments and failures in banking. The Banking Regulation Act, with its amendments between 1949 and 1960, continues to be the main tool with the RBI to handle the current crisis. There is a need for a more comprehensive review of the act to identify gaps and look towards the future. The banking industry is changing dramatically with the advent of technology and future risks could be from different sources.

Even with all these changes, we must realize that there is only so much any law or regulator can do. The Eastern Economist in 1949 termed Banking Regulation Act as a “colossal burden that a single institution is being called upon to have in policy-making as well as day-to-day administration of the country’s banking system” (Cited in RBI 1970). These words continue to be true as RBI now has additional powers to regulate NBFCs and HFCs. Yet despite these powers, the words of former RBI governor HVR Iyengar in 1960 tell us that RBI can only do so much:

“The Reserve Bank's powers are not [...] a substitute for the efficiency and integrity of the managements themselves [...] In the final resort, if a management does not listen to advice and chooses to be recalcitrant and it is felt that continued pressure would be useless, the Reserve Bank would have no option but to close down [the bank] in the interests of the depositors. But this decision involves a delicate balancing of several factors, some of them operational, some psychological.” (Cited in RBI 1998)