The unicorn, a fabled beast found on seals from the Indus Valley and in the heraldry of European royalty, has a new avatar in the digital economy. Digital startup firms which are valued at a billion-plus dollars are termed unicorns, apparently because of their rarity. Now, they are plentiful as deer, with more than 1,000 firms worldwide. India has its own share of unicorns. The Indian government proudly announced the addition of 44 unicorns valued at US$94 billion in 2021. The Economic Survey 2021-22 had a total of 83 unicorns, valued at US$277 billion as of January 2022. Since then, the count has gone up to 100, valued at more than US$330 billion (Invest India 2022).

The digital economy, powered by information and communication technology (ICT), has affected the way goods and services in the economy are produced, traded, and consumed. Digitalisation is seen as a general purpose technology — like the steam engine, electricity, or computers — which can fundamentally change the way economic activities are organised, unleashing substantial productivity gains. In addition, it has far-reaching social and cultural externalities. With more than 800 million internet users and smartphones, India is viewed as the next major destination for investing in a digital future.

Digitalisation and technology have created an ecosystem of startups. ICT has been the prime mover in this but, equally important if not more so, is the role of finance. Vast pools of global finance are pouring in to fund new ventures. 'Digitech' firms have grown at a dizzying pace from business ideas to billion-dollar companies in less than five years. They have generated a level of enthusiasm bordering on euphoria, and India’s hopes now seem to rest on dreams of a digital economy.

The digital economy is ubiquitous in urban India. From ride-sharing cabs, consumer goods, ...to travel and entertainment, a range of goods and services are bought online using electronic or digital payments.

These developments raise some critical questions about the nature and scope of the present phase of the digitalisation. It also raises questions about the role of global finance and the ways in which the startup economy is funded.

Digital economy startups

The digital economy is ubiquitous in urban India. From ride-sharing cabs, consumer goods, groceries, and food to travel and entertainment, a range of goods and services are bought online using electronic or digital payments. Less visible but gaining in importance are online services for health, education, information technology (IT), logistics, and business supply chains. However, the online market is still relatively small. India’s share of retail e-commerce in 2021 was a mere US$84 billion in a global market of US$4.9 trillion, but it is growing, alongside digital financial services. 1A 2019 report estimated a customer base of 90 million households, of which very rich and affluent households were estimated at 33million, followed by 57million dubbed as an aspirational class (BCG 2019).

The major markers of the digital economy are online platforms and the digitisation of data. It is no surprise that IT spending globally accounts for US$4.2 trillion in data centres, enterprise software, IT, and communications systems. Fintech, which is a bridge between technology, e-commerce, and finance, is another major sector accounting for nearly US$200 billion in revenue worldwide.

Digitalisation and the powerful network effects of online platforms combine to optimise the use of economic resources. With very little investment in physical infrastructure, digitechs are both aggregators and distributors of products and services. E-commerce, transport, and logistics can bring together hundreds of wholesale retail operators across cities and regions. Digitised data enables near infinite divisibility of services. For instance, payments can be made in very small units at low marginal cost to achieve a large consumer base. 2In China, companies like Ali Pay and ANT financials grew to a huge scale by providing micro-level credit and payment services. Insurance products can be created in small on-demand or usage-based units, such as auto insurance based on usage miles or house insurance for short rentals Prasad (2021, pp. 81-82).

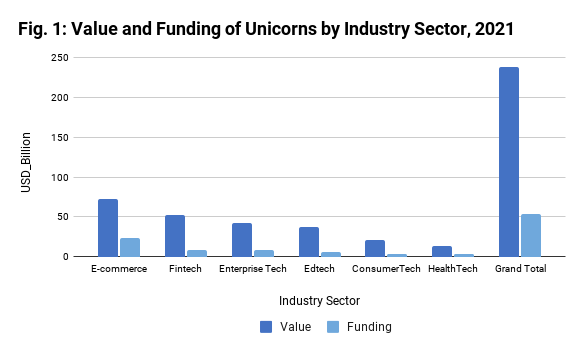

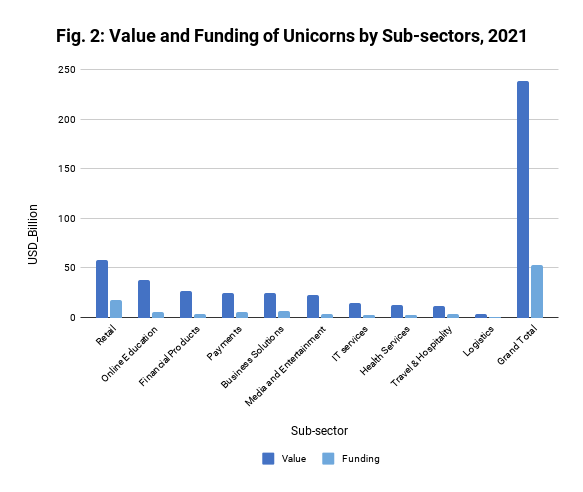

An analysis of 80 unicorns in India (Figure 1) shows that investment is the highest in e-commerce, followed by fintech and other sectors. These are further divided among sub-sectors such as retail, online learning, payments, financial services, business solutions, media and entertainment, and other services (Figure 2). 3EdTech is an outlier due to the weight of one firm, Byju’s, valued at US$21 billion and with a funding of US$1.5 billion.

Measuring the value added of a digital economy is not easy. 4G20 (2018) has developed a toolkit for developing measurement indicators of a digital economy, still a work in progress. However, estimates for the US and China vary between 7.5% to 10% of their gross domestic product (GDP) (Poenisch 2022). One measure is the amount of investment. In India, the cumulative investment in digital startups was approximately US$112 billion or equal to 4% of nominal GDP in 2021. Estimates of job creation vary but the most widely stated numbers are of 0.5 million direct and 3.5 million indirect jobs over a 10-year period (NASSCOM 2021; Startup India 2020; Bain India Report 2021).

Global finance has played a big role in the development of the digital economy worldwide. This is also true of India, which has received substantial inflows of foreign capital to finance digitechs. What lies behind these inflows could be described as the financialisation of global capital.

Global finance capital and digital India

Krippner (2005: 174) defined the phenomenon of financialisation of global capital as “a pattern of accumulation in which profits accrue primarily through financial channels rather than through trade and commodity production.” Global finance capital is manifested in different forms as private equity (PE), hedge funds, or venture capital (VC) besides large pools of more regulated funds such as pension funds and mutual funds.

In terms of size, financial capital is huge. The World Inequality Report (WIR 2022) estimates that the top 1% of the global population collectively owned around US$340 trillion in wealth in 2021. 5Derived from Table 7.1 (WIR 2022: 76, 139). Total global wealth is estimated at US$710 trillion or around six times the global output (world GDP). Excluding land, property, and other non-fungible assets, the bulk of the financial assets of the top 1% are invested as part of global finance capital. The share of private wealth is currently estimated at around 550% to 600% of the national income in high-income countries. The same is true of emerging markets. The share of private wealth to national income in India, China, Russia, and Brazil, rose to astonishing levels with an even greater concentration of wealth in the top 10% of the population. (WIR 2022: 76-77).

Indeed, financial investments yield substantially higher returns with considerably lower risk than the uncertain prospects of making profits in the real economy...

In terms of its scope, the deployment of financial capital is global, and it is organised around financial asset classes through a complex web of shadow banking institutions, institutional investors, investment funds, and private wealth and equity management groups. Global finance seeks to maximise its return through financial investment rather than in real investment. Indeed, financial investments yield substantially higher returns with considerably lower risk than the uncertain prospects of making profits in the real economy, and are less affected by economic cycles in the host economy. Private equity thrives, especially during economic downturns, and returns from funds even during the tough years of 2002 and 2009 were in the 17% to 21% range, above the long-term average of 16% (Bain 2021a: 5).

The management of global financial capital is concentrated in a small number of global financial institutions, including global banks and non-bank asset managers. This reinforces the tendency to focus on a narrow range of financial assets (Gabor 2018). Global asset managers have in recent years tended to flock to alternative investments, which include venture funds.

Despite the lull induced by the pandemic, the march of global capital continues. 'Buyout dry powder', meaning deployment ready funds, is at an all-time high of US$1.09 trillion. As global finance looks at multiple avenues to invest, interest in emerging markets is high. As a KPMG report has it, “It is not inconceivable that the $200 billion threshold is breached in the near future" (KPMG 2021: 17).

For foreign direct investment (FDI), using private equity or venture capital routes seem to be better options. The realised returns on PE funds expressed as a gross pooled multiple on invested capital (MOIC) averaged 2.2 times over 2015–2020, which would imply a return of US$220 for every US$100 invested over a five-year period. These investments have outperformed public markets around the world, particularly in the Asia-Pacific region (Bain 2021a).

India is increasingly a hot destination for FDI investments in venture capital and private equity funds. India ranks third in the world in the number of startups crossing the billion-dollar value threshold. Ironically, well-performing stock markets, in addition to direct investments, also make for attractive VC investments, as they provide a profitable exit route.

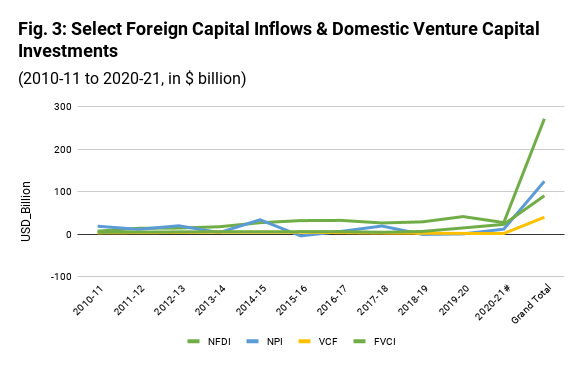

In India, around 750 institutional investors are involved in venture funding. The share of foreign venture capital investors (FCVI) has risen sharply over the years (Figure 3). At the same time net FDI and net portfolio inflows to equity, debt, and other capital market instruments has declined in relative terms. Foreign investments (FVCI), which were relatively flat from 2010–11 to 2018–19, showed a steep rise over the next three years. Net FDI, which was earlier largely invested in public stocks and other capital market instruments, shifted substantially towards alternative investment funds. Investments in stocks seem to have shifted towards portfolio investments, which are, not surprisingly, highly volatile. The share of domestic venture capital funds (VCF) in early stage funding of startups has declined. It remains to be seen if the post-pandemic revival will continue on the same trajectory, as industry reports suggest.

In an about-turn from attempts to regulate shadow banking after the global financial crisis in 2008, multilateral agencies and national governments now view private finance as the principal means of development.

Active encouragement from governments and central banks, along with post-pandemic fiscal and monetary policies, has meant that the hunger for investment and high returns has only been aggravated. In an about-turn from attempts to regulate shadow banking after the global financial crisis in 2008, multilateral agencies and national governments now view private finance as the principal means of development. A meeting of G20 digital economy ministers in January 2020 declared digitalisation as a key development goal for emerging markets: “As our societies and the global economy digitalise, there are ever greater opportunities to advance standards of living through human-centric, data-driven, and evidence-based policy” (G20 2020).

An Indian Government scheme, Startup India, had recognised some 66,000 startups as of February 2022. Liberalised regulations for investment in startups allow venture and private equity funds to raise capital from foreign and domestic sources to invest, leverage, or borrow against securities, invest in financial securities, including derivatives, and do short-term trading (SEBI 2012).

Financing, valuation, and exit of venture capital

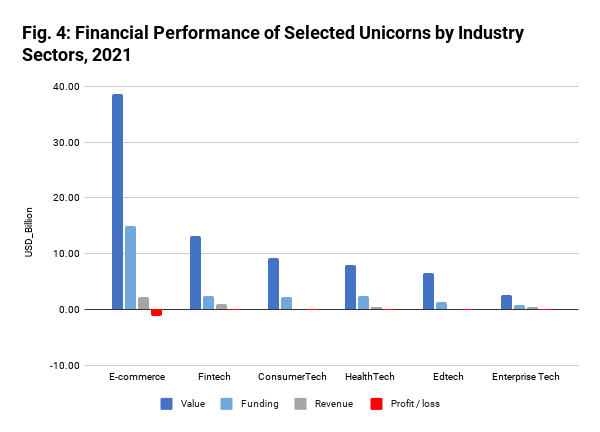

The valuation of an enterprise plays a critical part in its funding. In theory, the value of a firm would depend on various factors, including its capital and debt structure, cash flows, and past and future earnings, in addition to external factors such as the market and the economy. However, the financing of digital startups is different because the value of a firm is more often based on the level of its financing rather than its revenue or profitability. An analysis of the financial performance of a sample consisting of two-thirds of all high-value startups (unicorns) across different industry sectors cumulatively had low returns in proportion to their value or funding and negative returns in the financial year 2021 (Figure 4). A more detailed year-wise analysis would further indicate that most of the startups had attracted substantial financing despite successive periods of negative returns.

Around US$53 billion invested in the unicorns were cumulatively valued at US$238 billion (Figure 1). The concentration of financing in e-commerce and fintech, which is more than 50% of the total funding, suggests a strategy of quick wins and high returns rather than a long-term commitment to innovation. According to recent industry calculations, Brazil ranks first in terms of retail e-commerce developments with a compound annual growth rate (CAGR) of 20% while India ranks fifth with a projected CAGR of 18.5% between 2022 and 2025. 6Global: e-commerce retail sales CAGR 2022-2025 | Statista In contrast, startup funding in countries such as the UK, Israel, and Switzerland tends to focus on leading-edge technologies in bio-tech, med-tech, and clean tech besides fintech and IT, with a focus on frontier technologies such as gene therapy, artificial intelligence (AI) and robotics (Swiss Venture Capital Report 2022).

Venture financing is a continuous process of simultaneously funding and exiting, by rolling over funds from one entity to another. As these firms are privately held, funding and shareholder agreements are opaque. Venture financing is a stacked deck, where different venture funds come in at successive stages to acquire a stake in the firm while earlier funds may either continue or cash out of the deal. Financing involves different combinations of equity and debt. Typically, the share of venture capital in a high-value startup would be around 70% to 80%, with the founders, employee stock ownership plans (ESOPs), and other shareholders accounting for the rest.

Typically, a venture capital fund would sell out its stake when a firm went public through an IPO, usually under the glare of publicity and with inflated share premiums.

The realisation of returns is through a process euphemistically described as an exit. 7Every report of on venture capital funding has a description of the exit landscape. A key credo of venture capital is charting the exit landscape before venturing. Between 2015 and 2020, the top seven global VCFs in India raised approximately US$9.5 billion, deployed US$7.3 billion in several venture deals, and realised an exit value of US$12.6 billion. This amounts to a total return of 72% or a CAGR of more than 18% on investment over an average holding period of four years. 8Calculated from Bain (2021b); figure 27, p. 32 and figure 25, p. 30. Ventures have been immensely profitable despite 2020 being a difficult year for some sectors of the digital economy.

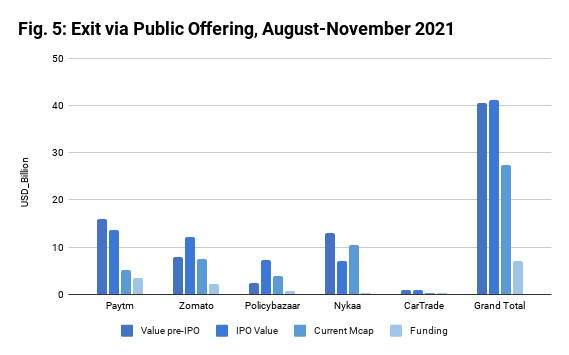

Exits are multi-layered activities. Typically, a venture capital fund would sell out its stake when a firm went public through an IPO, usually under the glare of publicity and with inflated share premiums. Paytm, Zomato, and Nykaa are some recent high-profile examples of such IPOs. Exits also occur by secondary sales, leveraged buyouts, or by other means. Venture financing has an obvious interest in higher valuation, regardless of cash flow or the future prospects of the firm. Exits enable venture funds to make their profits irrespective of whether the enterprise succeeds or fails in the long run.

Figure 5 illustrates the exits of five digitechs through public offerings or IPOs following their public listing in the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE) between August and November 2021. The pre-IPO value sets the stage for pricing of the shares and this is closely linked to the most recent financing round. The numbers show a highly profitable exit, with the potential return on investment averaging 5.8 times the funding value, and in individual cases by a more substantial multiple. A closer look at the pattern of financing shows that a significant part of the funding occurred closer to the date of public issue, enhancing both the pre-IPO valuation and the return on investment. 9For Zomato, 85% or US$1.8 billion of the total funding of US$2.1 billion occurred between 2017 and 2021, of which US$850 or 40% was funded between December 2020 and July 2021 before the IPO on 23 July 2021. For Paytm, the story was similar with US$1.5 billion invested in 2018-19 and US$1 billion subscribed by PE investors in November 2021, a week prior to its IPO on 10 November 2021. The duration of investment, for at least a significant part of the investment, was four years or less, indicating highly profitable disinvestments for the venture capital funds involved. However, it may have been a different story for the retail investors, judging by the current market capitalisation at the end of April 2022.

Financing, valuation, and exit are intrinsically linked, creating a cycle of accumulation through purely financial channels. Venture investments earn high returns regardless of the success or failure of the funded entities.

Future of digitalisation

The digital economy will continue to expand in all sectors of the economy. Digitalisation could potentially exert powerful positive externalities in the economic and social spheres to improve education, the environment, and health services. However, the inflow of global capital to emerging markets is largely directed towards consumption by the affluent, where returns are quicker and higher. This is an important consequence of the phenomenon of financialisaton of global capital.

The idea of innovation is ... misleading. Most e-commerce and fintech firms usually replicate business ideas learnt elsewhere.

Supernormal profits, and opaque financing and valuation are the main ingredients of this phenomenon. The hype about technology and data tends to obscure the essential point that it is mostly about commercialising them. The idea of innovation is equally misleading. Most e-commerce and fintech firms usually replicate business ideas learnt elsewhere. The motivation for quick profits is stronger than long-term investments in meaningful technologies, and research and development, especially going by the current trends seen in India. The digital economy’s contribution may well fall below expectations.

While tax incentives and regulations are aimed at attracting global investment, there needs to be more transparency in the financing and ownership structure of the startups. Guard rails are required to discourage excessive financial speculation. Regulation and oversight might also be needed to nudge digital economy firms towards a wider dispersal of benefits to society.

Acknowledgement: I wish to acknowledge the research support provided by Pawan Anil Thorat, Pune.

Kaushik Jayaram is a former central banker who worked for many years in an international financial organisation.