Since May 2020, India and China have been in their worst face-off in decades along the Himalayas, yet another stark reminder that the world’s two most populous nations have a fragile relationship. When 20 Indian jawans lost their lives in clashes with China’s People’s Liberation Army, the fault lines in India’s economic relationship with its northern neighbour were out in the open. Passions are running high in India; shrill demands have been made for boycotting Chinese products and prohibiting investments.

There are two issues here. First, how feasible or practical is it to boycott Chinese products altogether, given that India has developed a significant level of dependence on imports from China? Second, we need to understand the circumstances leading to a level of dependence that has not developed over a short period of time. It took China a good part of the past decade and a half to slowly but surely capture the Indian market in a very broad range of products. The question then is if the Indian economy can reduce its dependence on China, at least in the medium term.

1. Patterns of India-China trade since the early 2000s

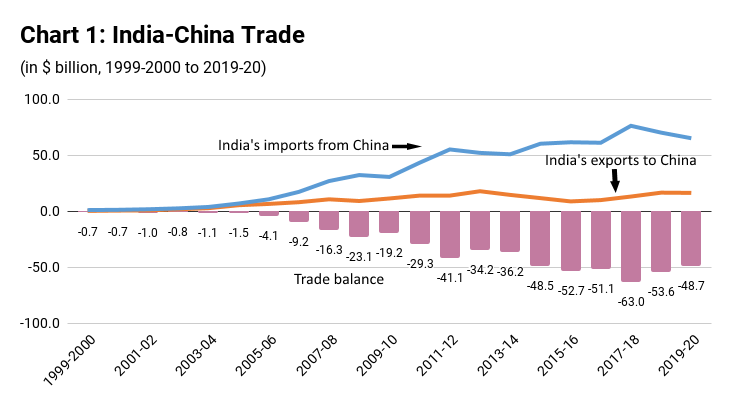

Imports from China began expanding quite rapidly from 2003–04 (Chart 1). In 2019–20 (April-March), China accounted for nearly 14% of India’s imports and was by far its largest source of goods imports.

Prior to 2003–04, India’s imports from China totalled less than $3 billion and the trade deficit was less than $1 billion. Over the next five years, India’s imports from China increased to $32.3 billion in 2008–09 and with exports expanding relatively slowly to about $10 billion, the imbalance in India-China trade widened to $23.1 billion that year. Over the next decade, China’s exports to India more than doubled to reach $76.4 billion in 2017–18. India’s exports to China also grew but neither consistently nor rapidly. They were $13 billion in 2017–18. The trade deficit with China that year was a massive $63 billion, nearly 40% of India’s overall trade deficit in goods.

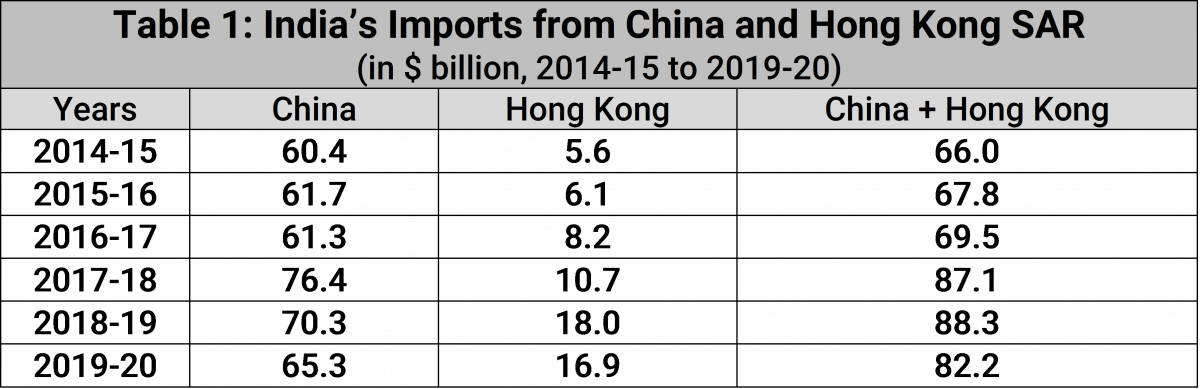

The decline in India’s imports from China in recent years may not imply an actual reduction in the sourcing of products from China, since coinciding with this reduction, imports from Hong Kong have seen a significant increase. Hong Kong has long served as a gateway for the distribution of China’s products to the rest of the world, importing products from China and re-exporting them to their final destinations. An earlier study reported that during 1988 and 1998, 53% of China’s exports were distributed via Hong Kong (Hanson and Feenstra 2001). In more recent years, some reports have indicated that there are other motivations, including tax avoidance, for routing Chinese exports through Hong Kong (Van Der Kamp 2016). The recent increase in India’s imports from Hong Kong needs to be also seen in this light.

Table 1 shows that since 2014–15, India’s imports from Hong Kong have consistently increased. Aggregate imports from China and Hong Kong have increased every year other than 2019–20, including in a couple of years (2016–17 and 2018–19) when imports from China alone dipped. In other words, the growth in imports from Hong Kong has more than compensated for the recent decline in the imports from China. Thus, when the sentiments in India were against China following the 2017 Doklam dispute with India, Hong Kong began to be used to tranship products manufactured in China. (The decline in imports from both China and Hong Kong in 2019–20 could perhaps be attributed to the supply chain disruptions in February and March 2020 when the Covid-19 pandemic was at its peak in China as well as Hong Kong.)

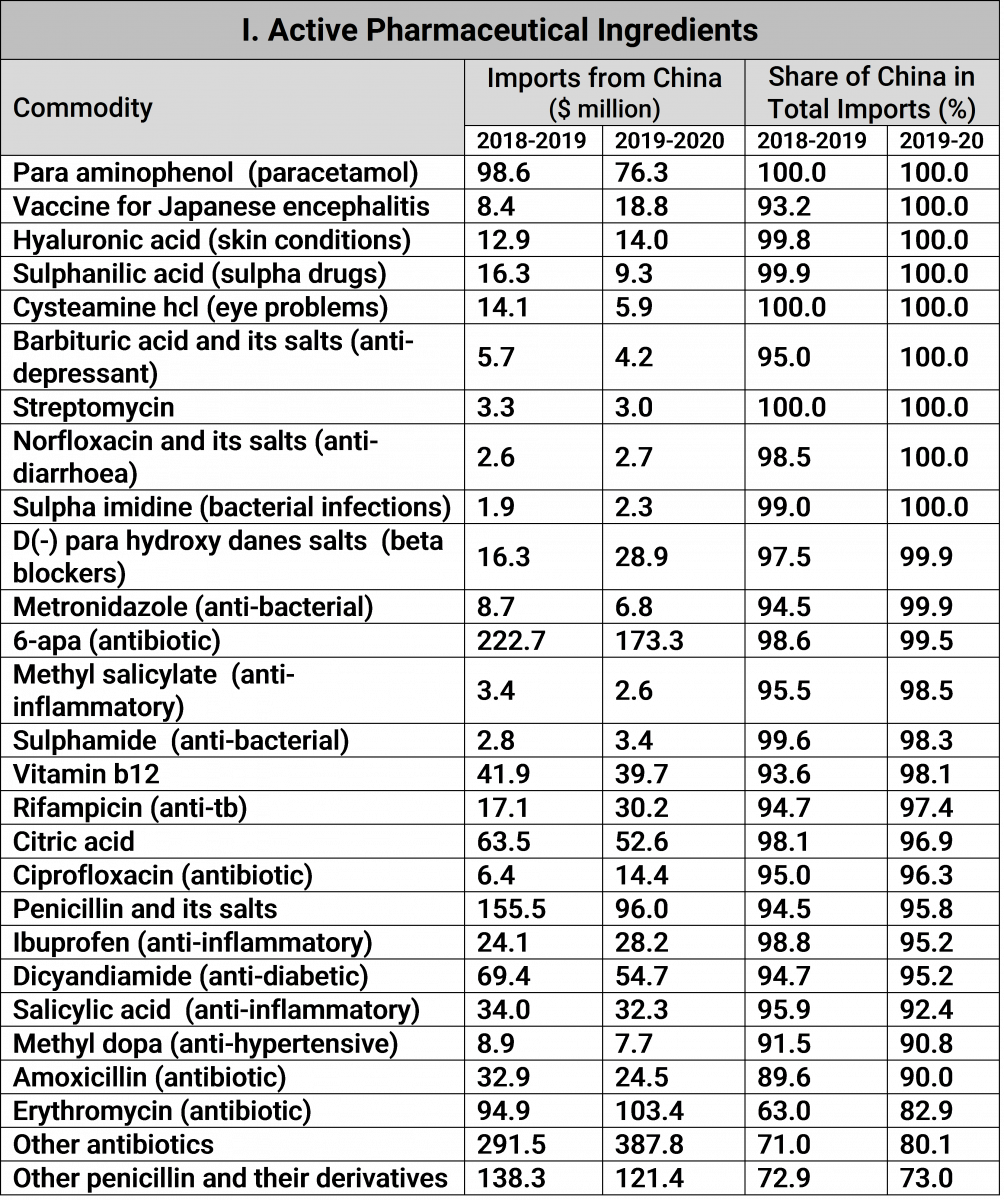

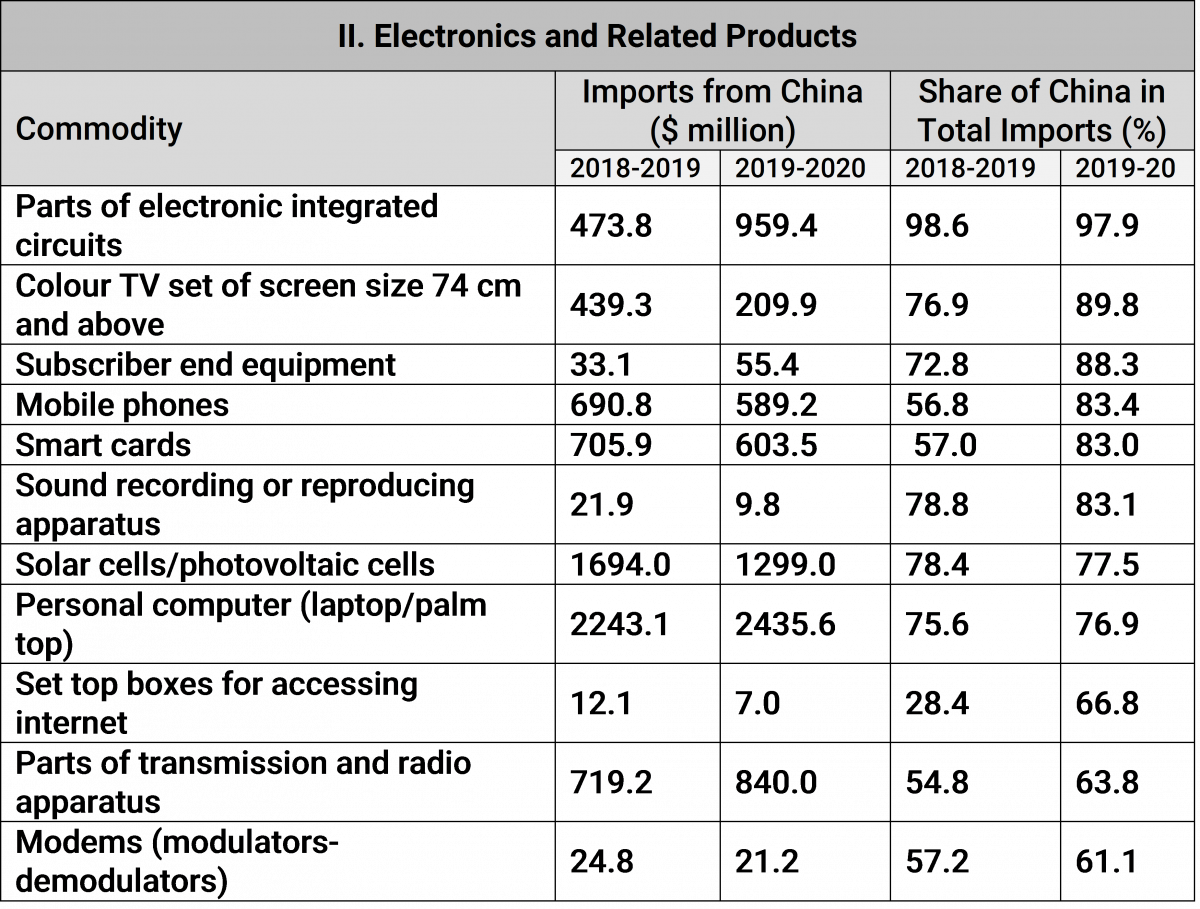

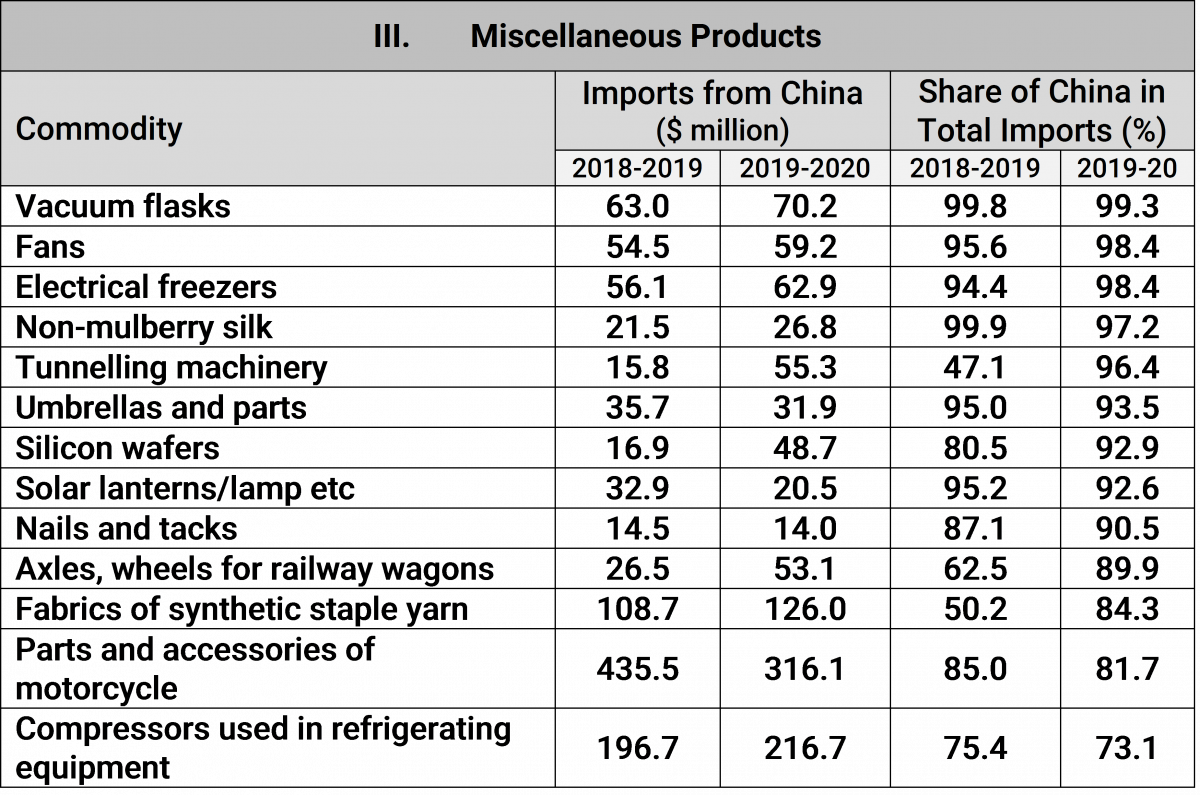

India’s depends on China for the supply of a wide range of products, from the simplest of products like nails/tacks and umbrellas to sophisticated electronic products and pharmaceutical intermediates. (See the Annex Tables I-III for details of the extent of Chinese domination in a long list of products.) But it is India’s reliance on Chinese imports in two product groups, namely, telecom and electronics products, and pharmaceutical intermediates (Active Pharmaceutical Ingredients or APIs), which is particularly disconcerting given the criticality of these sectors for the Indian economy. The Chinese domination in the imports of telecom and electronics products has increased manifold over the past few years after the government initiated the Digital India programme in 2015, “a flagship programme of the Government of India with a vision to transform India into a digitally empowered society and knowledge economy.” More important is India’s dependence on China for APIs, which have helped the Indian generic manufacturers provide cheap medicines not only in India but to many countries in both the developing and developed worlds. Due to its deep penetration in the global markets, the Indian industry has acquired the sobriquet of the “pharmacy of the world”.

Imports of telecom and electronic equipment from China have been quite significant. There is a common perception that fairly large volumes of mobile phones are sourced from China. This is indeed the case. In 2019–20, more than 83% of imports of mobile phones were of Chinese origin (see Annex Table III). But the fact that during the same year, nearly 90% of colour TV sets imported into the country were from the same country should surprise most. India continues to also depend substantially on imports of Chinese telecom transmission equipment.

[T]he dependence of India’s pharmaceutical industry on China shows that the “pharmacy of the world” has fairly weak foundations..

The syndrome of dependence on China is considerably worse in the case of APIs (Annex Table I). In recent years, India has been relied exclusively on China for imports of APIs for paracetamol, the common antipyretic and anti-inflammatory medicine. Similarly, India has been completely dependent on China for the imports of streptomycin and has very high levels of dependence on other antibiotics like ciprofloxacin and amoxycillin. China has also been supplying the APIs for rifampicin, used for treating several bacterial infections including tuberculosis. Besides these medicines, more than 95% of imports of penicillin in various forms have been from China. Imports of other major APIs for which largely come from China include semisynthetic penicillin (6-aminopenicillanic acid) and ibuprofen, a common medicine used for treating pain, fever and inflammation of various kinds, including arthritis. APIs of many other critical medicines too are sourced from China.

From this two conclusions can be drawn. First, the dependence of India’s pharmaceutical industry on China shows that the “pharmacy of the world” has fairly weak foundations that can be problematic for two reasons. While disruptions in supplies from China can cause serious bottlenecks, there is also no certainty that the Chinese suppliers of APIs have been maintaining the quality of their products in conformity with global standards. Second, since India imports more than 90% of the APIs for several antibiotics and vitamins from China, it is not possible for India in the short-term to successfully find alternate sources for meeting its API requirements.

The list of industries depending on China for their essential supplies is fairly long, but three other sectors are important (Annex Table III). The first is the motorcycle industry, which in 2018–19 sourced 85% of its imports of parts and components from China. While most motorcycle components are obtained locally, the Indian industry imports critical parts like wheel rims from China. Yet another disconcerting trend is that India is heavily dependent on China for solar photovoltaic cells. More than 90% of imports of silicon wafers and solar lanterns in 2019–20 were from China. This does not bode well for India as this renewable energy source is expected to be the lifeline of the energy sector as the country seeks greener options. The third sector is textiles in which synthetic and artificial woven yarn imports from China have risen.

The commodity composition India-China trade sums up the trade relations between the two countries as they have evolved over the past two decades. Charts 2 and 3 summarise the patterns of India’s imports from and exports to China as distributed between four broad product categories.

India’s imports from China have increasingly been skewed towards capital goods, a category here that include consumer durables. Imports of intermediates like APIs have also been sizeable. The share of imports of these products from China as a proportion of total imports increased to 57% in 2017 from 37% in 2003, after which it fell to 50% in 2019 (Chart 2). On the other hand, the share of intermediate goods imports from China, including APIs, fell to 27% in 2017 from 43% in 2003, but increased to nearly 34% in 2019. Consumer goods have had a relatively low share, increasing to 15% from nearly 12% between 2003 and 2019. These rising imports from China and their commodity composition reinforce the point that India is critically dependent on China in many areas and that this dependence cannot be overcome quickly.

India’s exports are a complete contrast to its imports: raw materials and intermediates dominate while capital and consumer are insignificant (Chart 3). India-China trade can be summarised as India supplying raw material and intermediates to China, while importing capital goods and critical intermediates for its pharmaceutical industry, the two-wheeler industry, and for synthetic yarn, among other goods.

The India-China trade pattern can be better understood through a few examples. In the earlier years, India’s exports included iron ore pellets and intermediates for plastics, including polyethylene and polypropylene, while imports included capital goods and synthetic yarn. Over the past two years, India’s exports have received a boost with Reliance Industries beginning to export paraxylene from its expanded petrochemicals production facilities (Dhar 2019). Paraxylene is the intermediate product for manmade fibres, which India has been importing from China. The implications of this pattern of trade for the respective economies is fairly obvious.

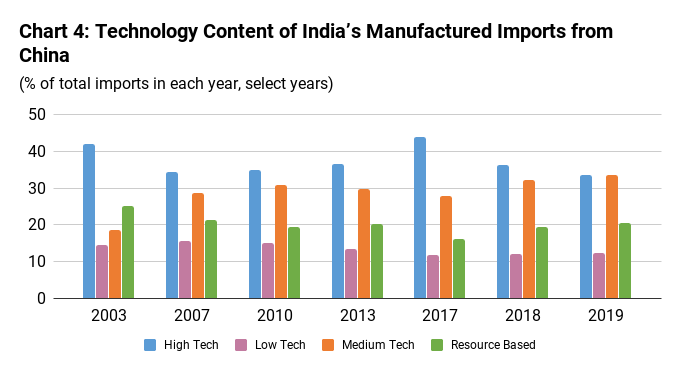

The current imbroglio between the two countries has brought into focus yet another issue: the technology content of the manufactured products traded between the two countries. Charts 4 and 5 provide the trends. The classification is based on Sanjaya Lall (2000), which provides a good basis for identifying the products by their technology content.

The pattern of India’s imports (classified by technology content) from China is quite in keeping with that for the broad product groups discussed earlier. Chart 4 shows that high and medium technology products dominated imports in 2019, accounting for more than 67% of the total. It may be mentioned here that the distinction between high and medium technology products can be somewhat contentious since several manufacturing sectors like machine tools and radio receivers, which have been classified as medium technology, can in fact be quite sophisticated in terms of their embedded technology. Only 12% of the manufactured products that India imported from China in 2019 were low technology.

[D]ependence on a single country for critical products in such a large measure can never be an appropriate strategy, especially when it has a huge demand for these products.

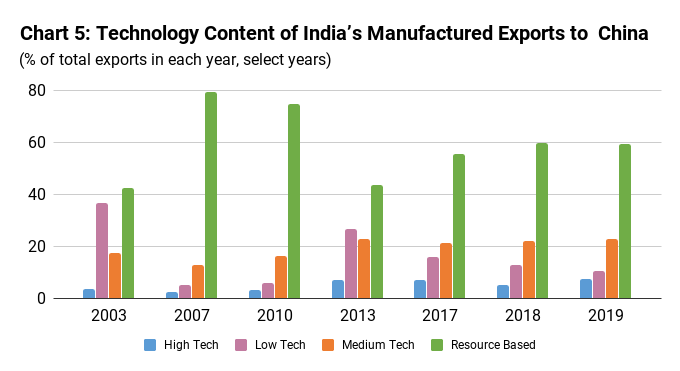

India’s exports were of a sharply divergent character (Chart 5). In 2019, more than 59% were resource based while the shares of high and medium technology products were 7% and 23%, respectively. The medium technology products were the petrochemical intermediates and processed iron ore products.

Two conclusions can be drawn from the above discussion. The first is that China is in a significantly superior position in the international division of labour vis-à-vis India. The relative economic performances of the two economies stands testimony to this fact. Second, from India’s perspective, dependence on a single country for critical products in such a large measure can never be an appropriate strategy, especially when it has a huge demand for these products. This situation needs to change, but this can happen only through the adoption of policies that can help change to a new normal. For doing so, India’s policymakers must reflect on what they should have done but did not do during the past 15 years. The fallout of this neglect is now causing much consternation within the country. If the lessons are not learnt, then, as the adage goes, the country would be left to repeat the same mistakes.

2. Explaining China’s Expansion in India

What explains the sustained expansion of imports from China since the early 2000s?

Two mutually reinforcing sets of developments explain the penetration of Chinese imports into the Indian economy. The first was India’s fast-tracked trade liberalisation that saw average import duties on industrial products decline to below 9% in 2008 from 33% in 2000. Import duties remained at that level until they were increased in 2018. 1 India’s average import duties for industrial products was between 9 and 11 per cent until 2018. A series of duty increases in 2018, raised the average import duties to 14 per cent (Dhar 2019, 60). India also had to remove (under WTO rulings) all the quantitative restrictions on imports, such as import licensing, in 2001. An expansionist China was thus provided an opportunity that it grabbed with both hands.

It was not as if advice on the urgent need to shore up the industrial sector had not been forthcoming.

The second development was the decision by successive governments to desist from taking any significant measure to prepare India’s manufacturing sector to face the challenges of an open economy. Policymakers had decided to repose complete faith in the policy of removing ‘market distortions’ through trade liberalisation and allowing the magic of the marketplace to put the economy on a ‘virtuous path’. Their target was to reduce import duties to the level of those in the East Asian region (Dhar 2020, 176–207). But what India’s policymakers refused to see was that these economies had adopted well-honed industrial policies before they opened up, which enabled their industries to not only face import competition in their increasingly open economies but also become globally competitive.

It was not as if advice on the urgent need to shore up the industrial sector was not available. In 2006, the National Manufacturing Competitiveness Council (Government of India 2006) advised the government to take prompt measures to raise the share of manufacturing in the country’s gross domestic product (GDP) to 23% within a decade. The United Progressive Alliance government unveiled the National Manufacturing Policy in 2011 in which the target set was to increase the share of manufacturing in GDP to 25% within a decade (Government of India 2011). And, finally, the Make in India initiative was launched in 2014 with the objective of strengthening the manufacturing sector and “raising the contribution of the manufacturing sector” to 25% of the GDP “in the coming years.” But the share of manufacturing in GDP has remained stuck between 15% and 17% for two reasons. One, the policy pronouncements for improving the share of the manufacturing sector in GDP were not backed by concrete measures. Two, in some of the key sectors, including electronics and pharmaceuticals, inappropriate instruments were adopted.

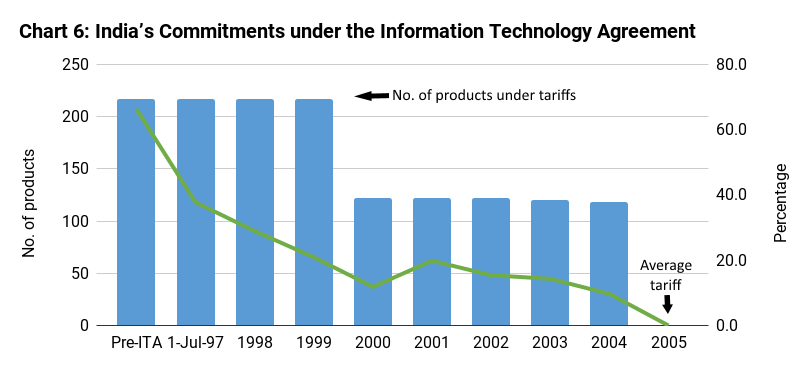

The production of electronics products in India goes back to the 1960s when public sector enterprises were tasked with the responsibility of producing computing devices (Dhar and Joseph 2019). Consumer electronics took root in the following decade and a fledgling industry was in place by the time economic liberalisation was set in motion in 1991 (Guhathakurta 1994). In the early phase of import liberalisation, the electronics sector was largely kept out of the process: the average import duties on these products was over 66% (Chart 6). The situation changed drastically after India joined the Information Technology Agreement (ITA), a plurilateral (optional) agreement under the World Trade Organization (WTO 1996) . When the ITA became effective on 1 July 1997, only 28 members of the 132 members of the WTO had acceded to the agreement. 2 European Union members are counted as a single customs territory.

According to the terms of the ITA (Chart 6), India agreed to eliminate import duties on 217 information technology (IT) products by 2005 in three phases: 95 products were rendered duty free on 1 January 2000, while duties were eliminated on the remaining products between 2003 and 2005 (WTO 1997). Accordingly, when the agreement became effective in 1997, India’s average import duties on IT products came down to 37.8%. By 2001, the average import duty on these products had declined to below 12%, before tariffs were completely eliminated on 1 January 2005.

The rationale for India’s accession to ITA seems difficult to understand as India was at the time a minor player in the global market for ITA products. India’s exports of IT products were the smallest among the 28 original signatories to the ITA between 1997 and 2003. 3 Based on authors’ estimates using UN Comtrade. In contrast, by 2003 China was already the third largest exporter of IT products and Hong Kong was not far behind. In fact, China and Hong Kong taken together have been the largest global exporters of IT products from 2003 onwards. It was hardly surprising that rapidly developing Chinese enterprises would take advantage of an open Indian market that was bereft of strong domestic competitors.

In the case of APIs, the dependence on China stems from the failure to ensure that domestic sources of supply were made available for the expanding drug formulations industry. This was in spite of the fact that the policymakers in the immediate post-independence phase had planned to build a strong API base. These policies were watered down and the public sector companies that were established to produce APIs were neglected from the 1980s onwards.

In 1954, the government had established Hindustan Antibiotics Limited with the objective of producing penicillin and its preparations, other antibiotics and vitamins (Committee on Public Undertakings 1976). Subsequently, the Indian Drugs and Pharmaceuticals Limited (IDPL) was established in 1961 for the manufacture of antibiotics, synthetic drugs and surgical instruments (Committee on Public Undertakings 1969). However, periodic reviews by several parliamentary committees showed that the two enterprises functioned significantly below their potential.

[E]very government, without exception, neglected the public sector enterprises that could have met the burgeoning requirement of APIs of the private formulations sector.

In 1974, the Committee on Drugs and Pharmaceutical Industry (better known as the Hathi committee after its chairman, Jaisukhlal Hathi) was constituted to recommend, among other things, the measures that would be “necessary for ensuring that the public sector attains a leadership role in the manufacture of basic drugs (APIs) and formulations, and in research and development” (Ministry of Petroleum and Chemicals 1975, 1). The committee noted that the “formulation activity represents the high pay-off sector of the pharmaceutical industry and bulk drugs manufacture gives comparatively low profits” (Ministry of Petroleum and Chemicals 1975, 55). Based on this finding, the Hathi committee recommended that strengthening of the public sector together with the private sector enterprises would be essential for a resilient pharmaceutical industry in India. In the subsequent decades, while the private sector firms expanded rapidly in production of formulations, every government, without exception, neglected the public sector enterprises that could have met the burgeoning requirement of APIs of the private formulations sector. This demand-supply gap in APIs was fully exploited by Chinese enterprises.

What is doubly inexplicable is that despite the body blow being suffered by the domestic manufacturing industry because of being thrust into import competition without the requisite preparation, successive governments have deepened import liberalisation through free trade agreements (FTAs). India’s three major FTAs, with the Association of South East Asian Nations (ASEAN), Korea, and Japan, respectively, have resulted in a widening trade deficit almost entirely because its exports have remained sluggish while imports from these trading partners have expanded because of the market opening (Dhar 2018). In recent years, there was a strong push from within the government to join another FTA, the Regional Comprehensive Economic Partnership (RCEP), which includes China. Academics and activists had cautioned about the adverse consequences of eliminating import duties on a large number of products, which would have enabled China to expand further in the Indian economy at the expense of the domestic manufacturing industry (Dhar 2019). When the Prime Minister was finally persuaded not to join the grouping in November 2019, the response of officials was that this was a “missed opportunity” for India.

As in imports, investments from China seem irreplaceable for India’s unicorns.

If India had joined RCEP, today the country would be ruing its decision. Besides offering lower tariffs to Chinese imports, RCEP would have not permitted India to scrutinise foreign investment from China, a policy that it introduced in April this year after the economic shock of the pandemic made many Indian firms vulnerable to a takeover. RCEP includes an investment agreement that limits the autonomous policy space of the participating governments to regulate investments.

India had unilaterally given up scrutinising foreign investment in 2017 by significantly deregulating the Foreign Direct Investment (FDI) regime by disbanding the Foreign Investment Promotion Board (FIPB). The liberalisation of FDI policies that began in the 1990s and gained momentum in the 2000s and 2010s was yet another nail in the coffin for the manufacturing sector. Companies already weakened by import competition became easy targets for foreign investors. This was evidenced by the increasing cases of takeovers of Indian entities (Rao and Dhar 2018).

The scale of Chinese investments in India is unclear, as official agencies from China and India give widely varying numbers. While India’s Department for Promotion of Industry and Internal Trade puts the figure at over $2 billion, China’s official agencies have put the figure at $8 billion. But as in trade, Chinese investors have a dominant position in India’s unicorns that are also an integral part of the gig economy (Rai 2020). The latter has often been lauded by the government as having the potential to address India’s unemployment problems. As in imports, investments from China seem irreplaceable for India’s unicorns. The political uncertainty could therefore put the future of these companies in some doubt.

With the government now emphasising ‘national self-sufficiency’, it could take lessons from an essay that John Maynard Keynes wrote at the height of the Great Depression, bearing the same title: “Ideas, knowledge, science, hospitality, travel these are the things which should of their nature be international. But let goods be homespun whenever it is reasonably and conveniently possible, and, above all, let finance be primarily national” (Keynes 1933, 181, emphasis added).

Annex Table: India’s dependence on Chinese imports: An illustrative list