Salil Tripathi was a hotel management graduate and worked as a manager at a Delhi restaurant before the pandemic, earning about Rs 40,000 a month. He lost his job during the first lockdown in 2020. To make ends meet, which included paying school fees for his 10-year-old son, he had to take up a delivery job at Zomato, making at the most Rs 10,000 a month, three-fourths less than what he had been earning earlier. He lost his father in the second wave.

His own life ended in a road accident while he was delivering for Zomato.

The rich and the elite of India have grown at the cost of others even as the overall economy was contracting.

This is the story of an upwardly mobile household whose journey was cut short by the pandemic, pushing them back to where they began from or perhaps even worse. This may well represent the conditions faced by a majority of the working people of this country during the Covid-19 pandemic. This though will not be the story told by the Government of India’s Economic Survey 2020-21.

‘Vulture Capitalism’

The gap between the rich and the poor is part and parcel of capitalism. It existed in India during the planning experiment of a 'mixed economy' and continues in the post-reform period. In the pre-reform period, incomes of both the rich and the poor grew, but at a slow pace. In the post-reform period, especially since the 2000s, the pace of growth picked up significantly, but diverged widely between the rich and the poor.

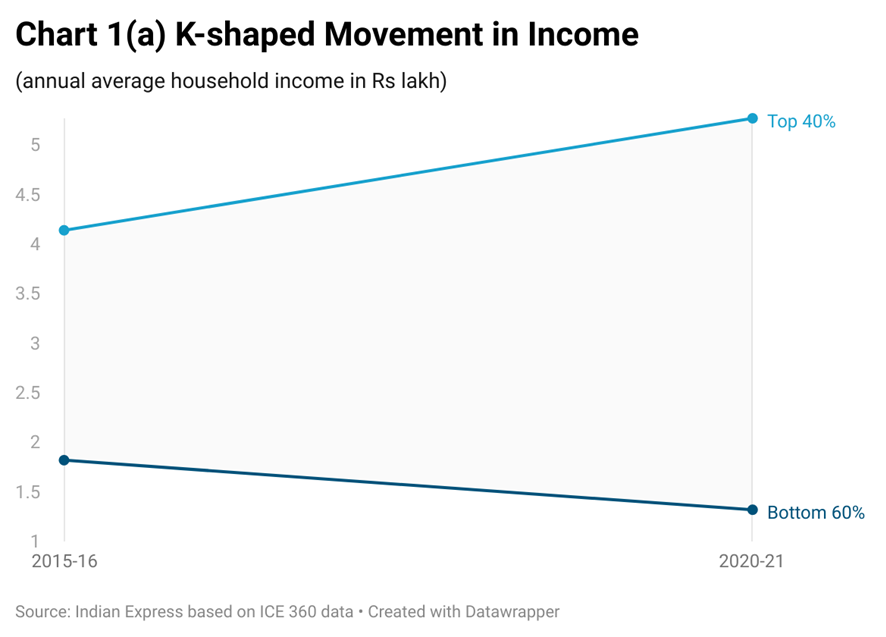

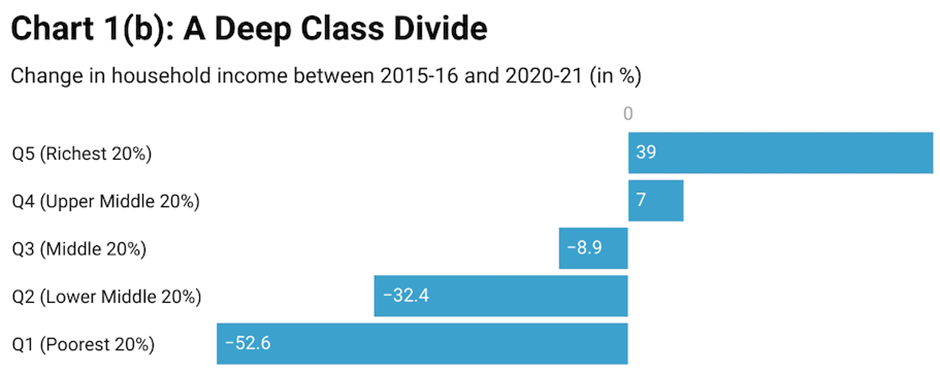

What we have witnessed during the pandemic though is something more alarming than widening inequality. The rich and the elite of India grew at the cost of others even as the overall economy contracted. Much like Dickens wrote, this pandemic has also been the best of times for some. Charts 1(a) and (1(b), based on recently released data from a survey, speak for themselves. That is a K-shaped movement in income.

This is disturbing because it is not the usual case of increasing inequality. Instead, it is a case of a few feeding off the absolute impoverishment of many. Most likely it started with demonetisation in 2016 but it has worsened during the pandemic (Chart 1 covers the period of demonetisation as well). One may quite aptly call it vulture capitalism.

As was shown by Santosh Mehrotra and Jajati Keshari Parada, poverty in India charted a V-shaped path between 2004-05 and 2019-20: falling between 2004-05 and 2011-12 and then rising between 2011-12 and 2019-20, when nearly 80 million more people were thrown into poverty. For the period specific to the pandemic, Mrinalini Jha used data from the CMIE's Consumer Pyramid Household Survey (CPHS) to show how the poor lost the most during the pandemic as compared with those in the highest quartile.

The poor lost their entire income during the first lockdown between March-April 2020, she points out. Even though there has been a near full recovery in the incomes of the poor after the lockdown, this needs to be set against the increased indebtedness (especially from informal sources) because of the loss of income during the first lockdown.

To be sure, the impact of the pandemic is not the same among the working people. As Rosa Abraham and Amit Basole demonstrated comprehensively, some groups, like salaried executives who held a regular position, did not suffer as much as the others during the pandemic in 2020-21.

Imagine now those for whom it was the best of times. Using the Forbes India Rich List, this report shows that between April and July 2020 (the first lockdown), the combined worth of the 100 wealthiest billionaires increased by a whopping 35%. While the wealthiest Indian, Mukesh Ambani, made Rs 90 crores every hour during the lockdown, 1.7 lakh people were losing their jobs every hour in April 2020.

We should remember this is not merely an economic crisis. We are globally in the midst of a triple crisis — health, economic and climate.

Another indicator of this vulture-like behaviour is the way the stock market has moved. The benchmark Sensex jumped to a high of over 62,000 in October 2021 from 29,468 in March 2020. So, while Zomato delivery ‘partners’ barely made Rs 10,000 in a city like Delhi, the company’s shares jumped up by as much as 82% when they made a debut in the stock market. It is perhaps for the first time in India that the stock market index was booming even as the economy was on a downward spiral.

One could argue that it is a reflection of what is to come with growth of the gig economy, rather than a reflection of what has already happened. But that may not be true, at least not entirely. The bull run in the stock market was not just restricted to the companies belonging to the gig economy, like Zomato, or restricted to large cap stocks. It was near universal with the mid- and small-cap companies across sectors doing well.

We should remember this is not merely an economic crisis. We are globally in the midst of a triple crisis — health, economic, and climate. While all sections of the society have been affected, the poor and the marginalised are the ones feeling the maximum brunt. A family that might have crossed the poverty barrier after years of effort would find itself back in poverty after a death in the family because of Covid-19 or even just one episode of hospitalisation.

Why this divergence?

Shouldn’t an economic crisis hit both workers and capitalists, even if the extent of impact differs between the two? If the pie becomes smaller, shouldn’t all the claimants lose at least a part of their pie? But here, not only did one section not lose anything, they increased the size of their pie by grabbing more from those who did not have much to begin with.

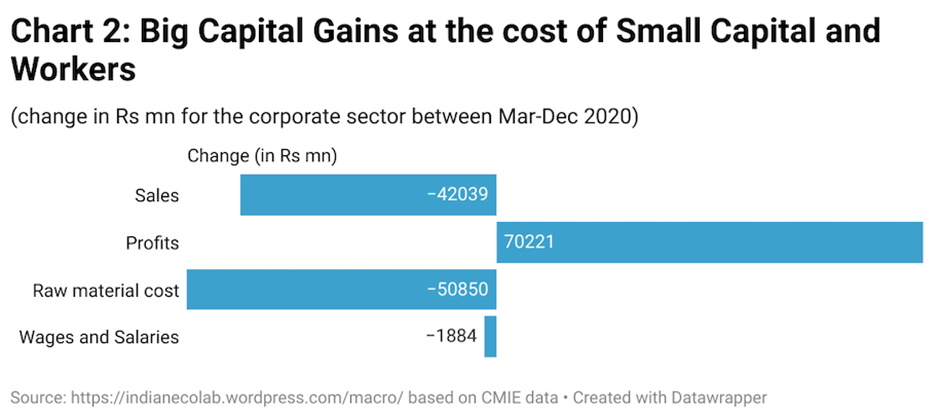

Chart 2, based on a sample size of 2,236 non-financial firms from the CMIE prowess database for the period March-September 2020, shows this perverse reality. While sales of corporates fell (the pie got smaller), profits rose. The rich and the wealthy gained even in the face of misery all around.

A short digression on income distribution may help put things in perspective.The two categories — poor/rich or workers/capitalists — are not homogenous. Instead of using class as a category, a simpler way for understanding income distribution might perhaps be to look at income (or wealth) inequality with people on an income (or wealth) scale, like Chart 1 does, without going into the source (from labour or capital) of that income. While this may measure inequality better, it does not necessarily tell us the why of it, which is where the lens of class comes to the rescue.

Income distribution is like the division of a pie, the size of which is the level of output (the real pie, not its nominal value) in any period. Here we are discussing only the distribution of this pie and not its size. Each class uses a bargaining chip to claim a share. Workers do it through wages, bankers through interest rates, primary commodity producers through food and mineral prices, and capitalists through prices of the commodity produced. It is obvious that only those who have the power to stake a claim, who the economists call price ‘makers’, can actively participate in this game of grabbing as large a share as possible.

In the absence of an active intervention of the government to influence this balance of forces, one could safely assume that capitalists, especially the big ones, are at the top of the ‘price chain’ because they are the final price makers. They normally set the prices over and above the various costs: wage, raw material, or interest. Who manages to get what share depends, in the end on the relative strength of these classes, and within these classes of different groups.

It would not be an exaggeration to say that one section fed off the misery of the other during one of the most stringent lockdowns in the world.

Those who are price makers (oligopolies, top end corporate executives, salaried workers up in the hierarchy) gain at the cost of price takers (petty raw material producers, small businesses like the Micro, Small and Medium Enterprises (MSMEs), unorganised sector workers, unskilled workers in the formal sector). Under normal circumstances, the latter set of people merely acts as spectators outside the boxing ring, so to speak, and settle with whatever remains after the game is over. In that sense they are the shock absorbers of the system.

Since there are multiple claimants with different striking capacities, this boxing match will have differential outcomes. Some from within the working class — top executives, and government employees — may not lose their share, or at least their jobs, despite an overall slowdown. Their brethren who are, however, lower in the pecking order of bargaining may lose everything they had. Similarly, even within the capitalist class, it would have a differentiated impact depending on where one is located on the price chain. Small and medium enterprises may lose since they cannot set their prices, especially during a recession, whereas big enterprises gain in the very process of suppressing the prices of intermediate goods bought from the smaller ones.

Against this backdrop, let us look at how the corporate sector fared during the pandemic. Based on the CMIE data, this report and opinion piece show that corporates managed higher profits even in the wake of falling sales by suppressing their wage and raw material costs by more than the fall in the revenue 1 One could argue that this perverse relation between sales and profits is a problem of aggregation since some sectors like the gig economy obviously gained from the lockdown. So, if the profits of the gig sector rose more than the fall of profits in the rest of the economy, it will show up as a rise in profits of the entire corporate sector. But one, if it is a problem of aggregation, it should show up in sales too and not just in profits. Two, if it shows up in profits and not in sales, it means even in sectors that grew during the pandemic, profits were rising much faster than wages and other costs. Three, as this piece argues, “(t)he sharp increase in profits during the September 2020 quarter is not concentrated in only a few large companies. It is quite widespread.” With lifting of the lockdown, sales have picked up in many sectors but our focus is on the lockdown in particular to show the vulgarity of this ‘vulture’ capitalism. .

It would not be an exaggeration to say that one section fed off the misery of the other during one of the most stringent lockdowns in the world. This is where the bargaining process came into play. While big corporations may not have managed to increase their prices, they were able to cut down on costs, which amounts to the same thing as far as the distribution of income is concerned. They did so by pruning their workforce or by suppressing prices paid to those lower down the price chain.

There is a similar story in the data on inflation in the post-lockdown phase of income distribution moving in favour of the big corporations and the elite. The recent episode of rising inflation, which seems temporary, has been partially led by increased crude prices as well as a mismatch between a temporary pent-up demand, especially by those in the upper arm of the K-shaped recovery, and supply chains that were broken by the lockdowns, both domestically and internationally. But a part of this inflation, as Roshan Kishore shows, based on CMIE data, is triggered by increased profit margins by firms in the non-financial sector.

This means that the firms chose to extract their pound of flesh by passing on higher prices to the consumers. The resulting inflation redistributes the income of the working people, particularly those whose wages are not indexed to inflation, in favour of firms in the non-financial sector. As for the financial sector, particularly banking, their profit margins have also increased as shown by the rising spread between their lending rates and the rate at which they borrow from the central bank.

The stock market is a very risky investment avenue and people with precarious sources of income would be wary of taking the plunge in such a big way.

What about the stock market boom? While the large cap stocks may have been driven by both domestic and foreign institutional investors, the mid and small were driven by retail investors. A report in the Financial Times shows that 40% of the current retail investors (almost 2 crore) have joined the National Stock Exchange in just the last two years. In total, they account for almost half the total trading market share in India. It is possible, as the report argues, that this increase in retail trading accounts could be distress-driven since people were losing their regular source of income and they needed to find an alternative. It is unlikely though that this was primarily distress driven.

The stock market is a very risky investment avenue and people with precarious sources of income would be wary of taking the plunge in such a big way. In all likelihood, the increase in trading came from the middle classes who could afford to take such risks. After all, there is the upper arm of the K-shaped recovery, driven by enterprises with the high-salaried regular employees and those in the gig-sectors that boomed during the pandemic.

While the majority of India was going hungry to bed and jobless for many months and dependent to a large extent on handouts from the government, there was another India that was merrily playing roulette with its money.

Is the misery temporary?

It is possible that this may just be a blip, since the 2020 lockdown was temporary? There are reasons to be worried that it is not so.

First, unlike countries that have robust social security systems or have pursued aggressive fiscal measures, a temporary supply ‘shock’ in India can lead to a longish depressed effect on jobs, incomes, and demand. Countries with such systems or policy responses would have, in effect, guarded against an aggregate demand and supply mismatch once the lockdowns were lifted.

A pandemic-induced lockdown disrupted the supply side of the economy. But once the supply gets stabilised, the overall demand needs to match up to it. Otherwise, potential supply in the form of idle factories and machinery will be ready to be utilised but will not have enough demand to start them up. In countries that have unemployment allowances as a policy for workers who may have lost their jobs or implemented a one-time aggressive fiscal response, demand would be forthcoming once the supply conditions eased.

The slightly well-off may have got their lost jobs back, but for a sizeable majority the lost jobs are lost for at least some time to come.

Countries like India neither have unemployment allowances for workers like Zomato's Salil Tripathi nor did they make a significant fiscal push during the first two years of the pandemic. The initial loss of jobs because of the lockdowns may have a prolonged effect on demand.

To take the case of Tripathi, even if this tragedy had not struck him, it would be hard to imagine that he would have easily got his job back. The restaurant in New Delhi where he was working would have to make a comeback post the pandemic with cash flows like before to be able to offer him a job. Some bigger ones may even make a comeback but not many smaller ones even in the capital.

The situation may be worse in innumerable other sectors where a restart may require the overall economic conditions of the country to improve significantly. The slightly well-off may have got their lost jobs back, but for a sizeable majority, the lost jobs are lost for at least some time to come. It will take a while for the whole cycle of economic activity to restart.

This is not the first time we are witnessing such a heavy and prolonged jolt to the job prospects of the working masses. We saw how long it could take to get the lost jobs back in the biggest, and perhaps the crudest, macroeconomic experiment in India of all times — the 2016 demonetisation disaster. Even five years later, those who lost jobs and incomes in the informal sector have not returned to their previous levels of livelihood.

We can only hope that the pain of the pandemic-induced crisis is not just as prolonged. But we cannot live on just a hope when livelihoods are at stake; we need an active policy intervention to ameliorate this pain at the earliest possible.

Is there a way forward?

Every crisis should also be seen as an opportunity to break free from the past. It gives policymakers an opportunity to think out of the box for the road ahead.

Unfortunately, most governments, so far, have gone down the same beaten path.

To begin with, in response to the severe triple crises, governments have primarily relied on 'below the line' financial measures. These are in the nature of loan guarantees and 'potential' liquidity injection, which are essentially supply-side measures and are, therefore, ineffective when the crisis is of a serious lack of aggregate demand in the economy. For example, the fiscal stimulus provided under India’s Atmanirbhar package, even by the most liberal estimates of the IMF, is a mere 2.5% of the GDP. The rest of the promised "10% of the GDP" promised (Rs 20 lakh crore) were practically loan guarantees and access to credit. Neither a household, which has lost jobs or income; nor a firm, which has significant idle capacity, would have taken a loan, how much ever the banks may persuade them with lucrative terms of lower interest rates and larger volumes of credit.

But if these did not work, what is all the discussion on a spectacular V-shaped recovery that India has witnessed?

A V-shaped recovery in growth rates is a statistical truism since that is just the effect taking place on top of the massive contraction of 2020-21. So, an economy with a GDP of 100, after having faced a 10% contraction due to the lockdown, may 'bounce back' with an arguably impressive 5-6% rate of growth. This means the output fell from a pre-pandemic level of 100 to 90 as a result of the lockdown and, after the lockdown was lifted, rose to 95. It shows that the economy has not even reached the pre-pandemic GDP level.

[I]t is not just a fiscal vs monetary debate: a more important question is what kind of fiscal policy do we need?

As compared with the ineffective monetary policy measures, fiscal measures are definitely far more effective as evident in many countries that took that path. But it is not just a fiscal vs monetary debate. A more important question is what kind of fiscal policy do we need?

Is there a path that can address the three crises simultaneously? A purely fiscal measure may address just one — economic — of the three crises. Instead, a green fiscal response, which focusses on spending on greening the infra sector while changing the energy mix of the economy as well as spending on the care economy, may take the triple crises head-on.

Such a response needs to forefront climate justice by incorporating redistributive elements, some of which are intrinsic to this path and some need to be designed as part of the programme. Our work shows that this green path is not only more labour-intensive compared to the business-as-usual scenario, it also favours the rural, unskilled and marginalised sections of the population. Additionally, some specifically built-in components — financing the programme through wealth and inheritance taxes; a right to access to energy to all — could help address the growing wedge between the two Indias.

An economic recovery of this kind — inclusive, sustainable, and equitable — is the only way forward.