A Finance Commission has four primary mandates prescribed in the Constitution. It decides on the share of the states in the divisible pool of Union taxes, the inter-se shares of states in that pool, grants-in-aid to states in need of assistance under Article 275(1) and measures to augment the finances of the states on the basis of the State Finance Commission reports for panchayats and municipalities. While most Finance Commissions in the past were given additional mandates by the president in the interest of sound finance, the Sixteenth Finance Commission (16th FC) had only the primary mandates prescribed in their Terms of Reference (ToRs), along with a reference on financing of disasters.

The 16th FC stuck to its mandate by confining itself to the framework of vertical devolution, horizontal devolution, grants for the third tier of local governments and disaster management. But, in a break from the past, it declined to recommend any grants-in-aid for states in need of assistance neither for meeting their post-devolution gaps in resources nor for any need-based intervention for merit goods or state-specific requirements. Not unexpectedly, this unusual recommendation has elicited both appreciation as well as opprobrium.

Does the departure from the earlier practice of giving grants-in-aid to cover the post-devolution revenue deficit to needy states conforms to the Constitutional mandate? Or has the 16th FC has not fulfilled its obligation to the Constitution?

Constitution on Grants-in-Aid

The Constitution does not define the terms “grants-in-aid” and “needs”. But the Constituent Assembly (CA) debates 1CA Debates dated August 8 and 9, 1949 on Clause 255 in Draft Constitution (later Article 275 in the Constitution of India) – Constituent Assembly Debates Volume IX reveal that the framers recognised wide disparities that existed amongst the provinces in terms of economic development and their dependence on resource transfers to carry out even basic administrative functions. Exploitation and neglect during colonial rule had left many provinces bereft of even basic services. The members of the CA also had before them the template of the grants made during colonial rule, including the Niemeyer award of 1936 preceding Independence.

In line with the intent of the CA debates, the Constitution provided for grants-in-aid as a mechanism to address the needs of the states that in the assessment of the Finance Commission remained unmet.

These were determined on the basis of certain broad principles for assessment of the final measure of need and took into account all other forms of assistance, including devolution of revenue and adjustment of debt. These were amounts which were estimated to be sufficient to place the finances of the provinces on an even keel and were unconditional grants. Thus, to meet the increased obligations that the Constitution would impose on provinces, the demand was for an impartial and transparent analysis of their requirements and needs without depending on the discretion of the Union government.

In line with the intent of the CA debates, the Constitution provided for grants-in-aid as a mechanism to address the needs of the states that in the assessment of the Finance Commission remained unmet from other sources of transfers and debt in Article 275 and Article 280. The terms of reference of the 16th FC called upon the commission to make recommendations on “the principles which should govern the grants-in-aid of the revenues of the States out of the Consolidated Fund of India and the sums to be paid to the States by way of grants-in-aid of their revenues under article 275 of the Constitution for the purposes other than those specified in the provisos to clause (1) of that article.”

The provisions contained in the two Articles are as follows:

● Article 275(1): "Such sums as Parliament may by law provide shall be charged on the Consolidated Fund of India in each year as grants-in-aid of the revenues of such States as Parliament may determine to be in need of assistance, and different sums may be fixed for different States."

● Article 280 (3) (b): "[It shall be the duty of the Commission to make recommendations to the President as to ...] the principles which should govern the grants-in-aid of the revenues of the States out of the Consolidated Fund of India."

Article 275 (2) further provides that no grants shall be made under this by the President except after considering the recommendations of the Finance Commission. With Parliament not having made a law yet on the subject, the Finance Commission’s recommendations become obligatory for the President to consider.

The provisions contained in Article 275 and 280(3)(b), are silent on the question of whether these grants can be made or not, and if they are made whether they should be conditional or unconditional. The reason for this question to arise is primarily due to use of the word “may” and not “shall” in Article 275. This is especially in contrast with the language used in Article 270(1) with respect to tax devolution where “shall” has been used. Does the Constitution therefore allow the Finance Commission to recommend principles for grants-in-aid at its discretion?

Supreme Court Ruling

A question similar to the use of “may” and not “shall” in the field of revenue law was answered by the Supreme Court. 2See Chief Controlling Revenue Authority and another vs the Maharashtra Sugar Mills Ltd ( AIR 1950 SC 218): page 221 para 7. The apex court had noted that “when a capacity or power is given to a public authority there may be circumstances which couple with the power a duty to exercise it.” It went on to quote from a judgement of the Privy Council that “there may be something in the nature of the thing empowered to be done, something in the object for which it is to be done, something in the conditions under which it is to be done, something in the title of the person or. persons for whose benefit the power is to be exercised, which may couple the power with a duty, and make it the duty of the person in whom the power is reposed to exercise that power when called upon to do so.”

The use of the word 'may' does not necessarily mean 'may not'. The word 'may' will transform to the word 'shall' depending on the circumstances and prevailing conditions as assessed by the Finance Commission in each case. No constitutional power can be exercised as a matter of grace; the grant-in-aid is not a grace. All actions of every authority have to be informed with reason and should not be unjust, unfair or unreasonable or arbitrary or whimsical.

No constitutional power can be exercised as a matter of grace; the grant-in-aid is not a grace.

Article 275(1) itself provides the guidelines. In this case, it is the need of the states which is sine qua non for such grants. The word 'may' as 'shall' is not arbitrary and has to be read according to the facts and situation of the need of each state based on objective criteria, and the Finance Commission is empowered to prescribe different sums for different states. It should not be vitiated by political considerations as different political parties may be in power in different states in a federal constitution like the Indian Constitution.

Revenue Deficit Grants

The Constitution in Article 280(3)(b) casts an obligation on the Finance Commission to make recommendations on the “principles” to govern grants-in-aid. Read together with Article 275, the principles set out are importantly akin to guidelines for internal work in the commission in the matter of re-assessment of revenue and expenditure forecasts of the states to evaluate the needs of each state. They provide the framework founded on comparable analysis, past data and behaviour. The analysis seeks to eliminate expenditure items that are excessive or do not meet the norms. The evaluation of the resource base of the states is done using comparable data on tax effort and tax efficiency. Historical factors and structural constraints are analysed to moderate the findings wherever necessary. A state-wise assessment done on a comparable basis will eliminate any abnormal, unusual and non-recurrent items of receipts and expenditure which may vitiate comparisons unless they are excluded. All these, and many other used by different Finance Commissions feed into the estimation of states’ fiscal position.

All Finance Commissions, including the 16th FC, have relied on devolution of taxes as the primary mode of transfers. Grants-in-aid, a very small share of the transfers recommended, have been used by all Finance Commissions in the past to address specific needs of the states. General purpose grants also called “gap grants”, or “revenue deficit grants” (RDGs) served the purpose of addressing the deficient resources of the states. These have always, with one exception, been unconditional. 3The 11 FC in its final report recommended that a certain portion of revenue deficit grants would be conditional and released on fulfillment of certain conditions prescribed for the States. Dr. Amaresh Bagchi, Member, gave a dissent note arguing, inter alia, conditionality attached to RDG was against the spirit of the Constitution. Conditional grants served the purpose of addressing the fiscal capacity of the states with the relative need for any specific services, especially merit goods like education or health. As regards the relative role of unconditional and conditional grants, each Finance Commission has attempted through a detailed assessment of each state the system or a combination of systems that best fits the facts of its current economic circumstances.

Grants-in-aid, a very small share of the transfers recommended, have been used by all Finance Commissions in the past to address specific needs of the states.

While conditional sector-specific or state-specific grants have varied across the past 15 Finance Commissions, RDGs have been a constant feature in each of them. What is the reason for this?

Revenue Deficit Grants reflect the gap that exists in a state’s normatively determined revenues and expenditure after the devolution of Union taxes as per the horizontal distribution formula. It signifies the existence of a vertical imbalance yet to be corrected. Unlike a gap-filling approach that assesses without making any corrections in the fiscal behaviour of the states, a normative or comparable assessment ensures that deficiency in fiscal capacity is corrected, but inadequate revenue effort or excessive expenditure is not encouraged. Thus, after the devolution, some states end up with a post-devolution revenue deficit as a result of a vertical imbalance that needs correction because the assessed need is yet to be met. Revenue Deficit Grants, therefore, ensure that as per the Finance Commission’s assessment, at the beginning of each year of the award period, all states start with at least a revenue balance.

This is the second article in a two part series on the 16th Finance Commission. Read the first article here.

Another Constitutional question often asked is whether conditions should be attached to the RDGs? Article 275 is silent on this. It does not specify any approach, leaving it to the Finance Commission to determine. With the exception of one instance (see note iii), the RDGs have been unconditional. Does this precedent, therefore, become a “constitutional convention”?

The legal effect of constitutional conventions has been considered by the Supreme Court 4In Supreme Court Advocates-on-Record Association Vs Union of India (1.993) 4 SCC 441 at page 650 at para 337 which has held that that there is no distinction between the "constitutional law" and an established "constitutional convention'' and both are binding in the field of their operation. Once it is established to the satisfaction of the Court that a particular convention exists and is operating, then the convention becomes a part of the "constitutional law" of the land and can be enforced in the like manner."

16th Finance Commission on RDGs

The 16th FC has not recommended any RDG or sate-specific or sector-specific grants. The Constitution does not make it mandatory for a Finance Commission to prescribe any RDG or any type of conditional grant. What it does is to ensure that in making its recommendations the Finance Commission has not been prejudiced, imbalanced or arbitrary or whimsical.

The 16th FC in reaching its conclusion has not carried out any normative assessment for comparability of tax effort or expenditure rationalisation, and projections of the state-wise needs in its report. While being critical of the previous Finance Commissions for their poor marksmanship in making assessments and projections, the 16th FC too has carried out a similar subjective exercise on projections as the previous FCs. The analysis fails to recognise that projections can become under-estimations or over-estimations depending, amongst other things, of the macro-economic scenario, performance of the national economy, the Union’s conduct of macro policies, monetary conditions and the Union’s own budgetary numbers. For instance, the 16th FC’s own projections for the Union finances have proved to be an over-estimation over the 2025-26 (Revised Estimates) and 2026-27 (Budget Estimates) for transfer of taxes to the states.

The 16th FC recommendation overlooks the fundamental principle of fiscal federal structure in India where the surplus of the states in the aggregate is not shareable amongst deficit states.

Second, the report is silent on state-wise data of the assessed pre-and post-devolution tax resources and expenditure needs. It has instead done an aggregated view of all the states combined and reached its conclusion. As noted in a recent review of the recommendations, “even if the assessment is that no state is in any need of assistance, such a recommendation should have been based on a detailed examination and assessment of state finances”. 5D.K Srivastava, 16th Finance Commission: A shift in approach to grants and tax devolution, Moneycontrol, February 2, 2026, https://www.moneycontrol.com/news/opinion/16th-finance-commission-a-shift-in-approach-that-will-not-help-states-with-lower-fiscal-capacity-13804134.html/amp

Third, the 16th FC recommendation overlooks the fundamental principle of fiscal federal structure in India where the surplus of the states in the aggregate is not shareable amongst deficit states. The long history of Finance Commission devolutions has established that the horizontal distribution made on certain broad principles to ensure a certain degree of equity, equalisation and efficiency leaves many states with a post-devolution revenue surplus, but certain states are still left with assessed deficits. The states with post-devolution surplus are placed on a superior footing vis-a-vis access to resources compared to stressed states with a deficit. All Finance Commissions in the past were cognisant of this requirement to bridge the residual post-devolution revenue gaps through RDGs.

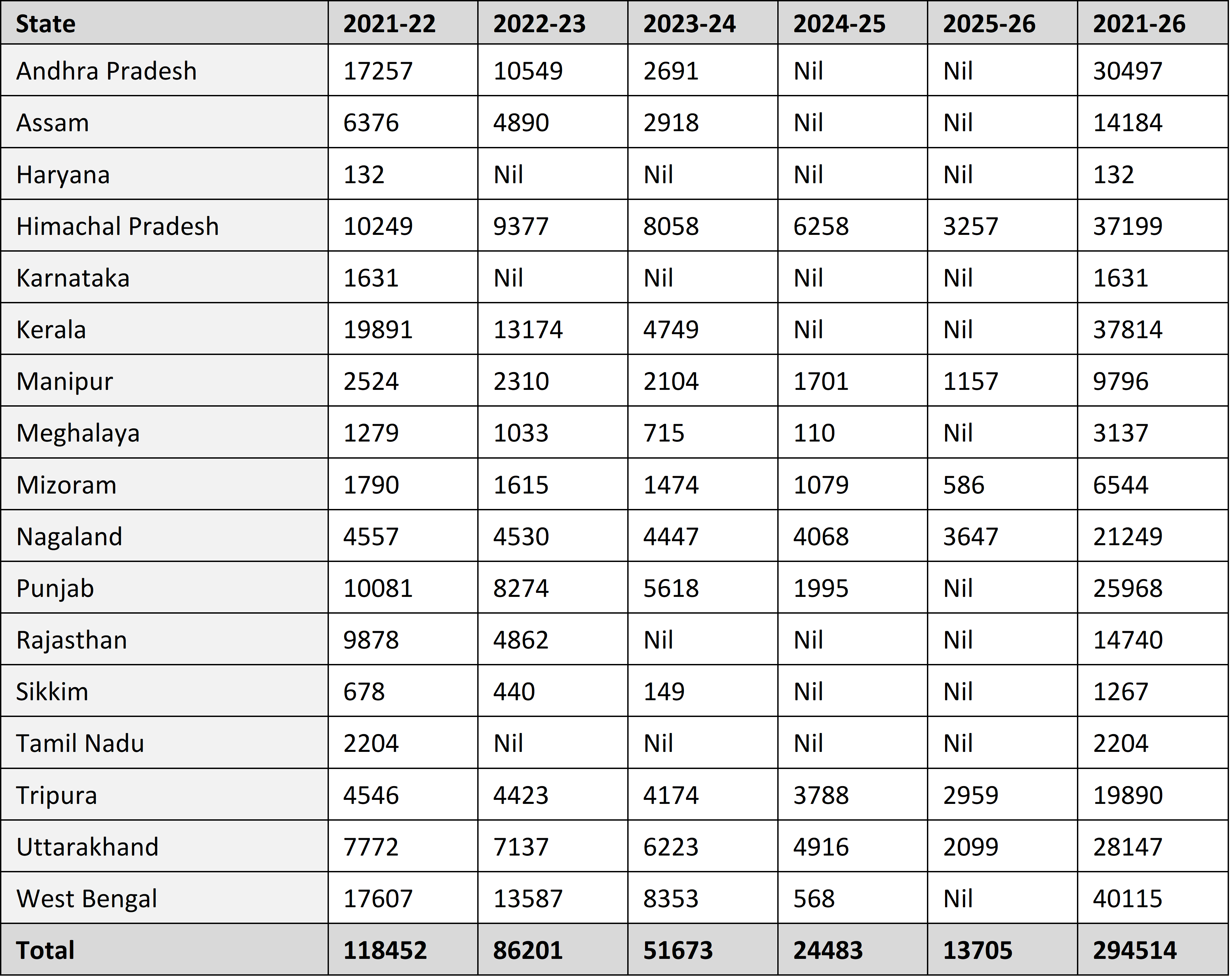

The RDGs, on the minimum, ensured deficit states came to a normatively assessed revenue balance. The 15th FC gave RDGs to 17 states in 2021-22, the first year of the award. By the final year, 2025-26, the number of states receiving RDGs were the six north-eastern and hill states. Table I gives the amounts and spread of the grant over the five years of the 15th FC period. As no specific assessment of the fiscal gap in each state has been done by the 16th FC, the impact can only be evident as the fiscal year 2026-27 unfolds. Can this be the reason that the Union government in its Action Taken Note 6Explanatory Memorandum as to the Action Taken on the Recommendations Made by the Sixteenth Finance Commission, February 2026, Ministry of Finance, Budget Division, Government of India. placed in Parliament kept its options open for assisting the states in fiscal distress by stating that “the Government takes note of the assessment of the Commission” instead of the usual “the Government accepts the recommendations”?

Table 1: Grants-in-aid for Revenue Deficit (2021-26)

Finance Commissions as an institution have been widely respected for their impartial and non-partisan approach to address inter-governmental transfers. Dr. Ambedkar had said in the CA debates that “the Finance Commission will act as bumper between the States and the Centre” 7CA Debates dated August 10, 1949 on Clause 260 in Draft Constitution (later Article 280 in the Constitution of India) – Constituent Assembly Debates Volume IX TT Krishnamachari in his intervention in the same debate added that the Finance Commission will assure the states that they will have a fair deal.

By missing a Constitutional mandate of assessment and projections for each of the states, the 16th FC has left many states with uncovered deficits that may adversely impact their fiscal balance over the award period.

This article was first published in The Forum for State Studies.

Ajay Jha, a former finance secretary to the union government, was a member of the 15th Finance Commission.