For many, the advent of digital money was logically inevitable. In the long history of the evolution of money, as a commodity, as coins, and as paper, the form of money has become progressively more symbolic and abstract. The digital form is merely its latest manifestation. From this perspective, the discussion around a digital currency would be essentially technical in nature and would focus on its benefits, costs, and risks, and which particular form of digital money would most suit the needs of an economy.

Central banks around the world are actively engaged with the question of having a central bank digital currency (CBDC). In more than 100 central banks, the question has moved beyond academic enquiry — some are researching its feasibility, others are in the design stage or pilot testing variants of CBDCs, and some have already launched a digital currency.

Emerging markets have taken the lead with the Bahamas being among the first to launch a CBDC in 2020, the Bahamian Sand Dollar. Nigeria launched its eNaira in 2021. China was the first among the major economies to pilot a CBDC, the e-Yuan, and is conducting large-scale trials with some 100 million users. There were earlier versions of digital cash such as the Bank of Finland’s Avant, or Tunisia’s e-Dinar but these were more in the nature of debit cards. South Korea and Sweden are the other major economies conducting trials on variants of CBDC. Many of the advanced economies are undecided as yet, but they are carrying out detailed studies on the pros and cons of having a digital currency.

The principal raison d'être for a CBDC is that the pace of technological change has created new challenges to the central bank monopoly of issuing currency with several versions of privately issued digital 'money'. The proponents of a CBDC see many advantages to it, beginning with it being an efficient and technologically advanced replacement for paper currency.

[A] CBDC as a fiat currency represents a fundamental transformation of the nature of money as we know it, and not enough is known on how this will affect the monetary and the financial system or, indeed, society as a whole.

The House of Lords Committee in the United Kingdom has called the CBDC a solution in search of a problem (House of Lords Committee 2022). Its scepticism stems mainly from that central banks have not yet made a convincing case for a digital currency. Our reasons for arguing against a CBDC go further. We make the case that a CBDC as a fiat currency represents a fundamental transformation of the nature of money as we know it, and not enough is known on how this will affect the monetary and the financial system or, indeed, society as a whole.

Design of a digital currency

The design of a digital currency assumes critical importance in enhancing its effectiveness while mitigating potential risks. A universal digital currency, which is often described as a retail CBDC, could be based on a centralised ledger technology (CLT) or a distributed ledger technology (DLT). A CLT would enable greater control of the central bank while a DLT would be based on a blockchain of decentralised transactions. (Saha and Ray (2021) have a detailed explanation of the use of CLT and DLT technologies as well as other technical design elements of digital currencies.) A CBDC may be account based in the central bank, or mediated through commercial bank accounts, or issued as anonymised tokens (as digital cash), or some combination of these. In the hands of a retail user, a CBDC would be available in a digital wallet similar to the many types of electronic payment instruments now available.

Wholesale digital currency: Some central banks are looking at wholesale digital tokens (wCBDC) for the settlement of transactions between financial institutions. A wCBDC would essentially be a pre-paid digital token that offers definitive finality of payment between financial intermediaries, and under certain conditions improve the liquidity management of the financial institutions participating in the system. However, a wCBDC in a purely domestic setting might not add much value over a real time gross settlement (RTGS) system.

A CBDC combining the features of direct cash payments and the efficiency of electronic transfers enables a faster, cheaper, and more reliable system of payments and settlements than is currently available.

Payment transactions in an RTGS system have near instant settlement finality in the books of the central bank. RTGS provides for a number of ways to manage liquidity—by balancing incoming payments against outgoing payments and through effective queue management. Secondary liquidity is also available via access to central bank credit (See Mägerle and Oleschak 2019). However, since RTGS systems everywhere are generally restricted to major participant banks and significant financial entities, settlement in wCBDC could potentially include a wider range of participants, including non-resident institutions and other non-bank entities, as pre-paid wCBDC tokens could be used to settle payments even without having an account or access to central bank credit.

Cross-border payments: The use of CBDCs for cross-border payments could potentially have many benefits. A retail CBDC could be made available to foreign residents either conditionally, for limited purposes, or without restriction. This would be similar to non-residents holding a country’s currency in cash or as bank credit for travel, remittance, or payments within the currency area. However, there are concerns and risks for the issuing central bank.

Cross-border settlement systems using wCBDC would have significant advantages. They could potentially simplify intermediation chains of correspondent banks, and operate a peer-to-peer settlement in bilateral or multilateral central bank currencies. Cross-border payments would be faster, cheaper, and considerably reduce credit and liquidity risks as counterparty central banks would provide the implicit guarantee of settlement. For emerging market central banks this would significantly enhance their ability to manage international payments in multiple currencies and reduce their need for maintaining substantial reserves in dominant currencies.

However, this requires a lot of groundwork for developing interoperability and security standards as well as cross-border governance frameworks. Incidentally, the Financial Stability Board (FSB) in its roadmap on behalf of the Group of Twenty (G20) assigns only one out of 19 building blocks to a CBDC in enhancing cross-border payment. Other building blocks focus on enhancing the existing infrastructure and technology (FSB 2020).

Case for a CBDC

The motivations for issuing a CBDC vary among central banks. The most commonly cited reasons are cash substitution, competition from private issuers of digital money, enhanced payment services, reducing the cost of financial services, improving financial inclusion, preventing money laundering, tax evasion, or counterfeiting, and a more effective monetary policy (BIS 2022). The case for a CBDC is based on the following key points.

Increasing efficiency of payments: A CBDC combining the features of direct cash payments and the efficiency of electronic transfers enables a faster, cheaper, and more reliable system of payments and settlements than is currently available.

Enhancing cross-border payments: The use of a CBDC in cross-border payments, as well as in domestic payments, would be faster, cheaper, reliable, and transparent.

Broadening financial inclusion: While it would not directly promote access to a range of financial services for underserved households and businesses, a CBDC would help mitigate some of the constraints by enabling low-cost payment services and direct fiscal transfers of benefits.

More effective monetary policy: By monitoring, controlling, and directing the supply of central bank money, a CBDC could support faster and more effective transmission of a monetary policy. Central banks could lever the tools of monetary policy far more granularly and target specific sectors of the economy than is now possible.

Reforming the international financial system: Some would see the issuing of CBDCs by many countries as a shift from the dominance of the dollar. A multi-currency cross-border settlement system could potentially correct reserve imbalances and suit the needs of an increasingly multipolar global economy.

Risks: Central banks also see potential risks. The dominant concerns are privacy, disintermediation, operational risks, disruption of financial systems, cyber threats, cross-border currency substitution, volatility, currency dominance, and, ironically, the potential loss of currency sovereignty.

Electronic money versus digital currency

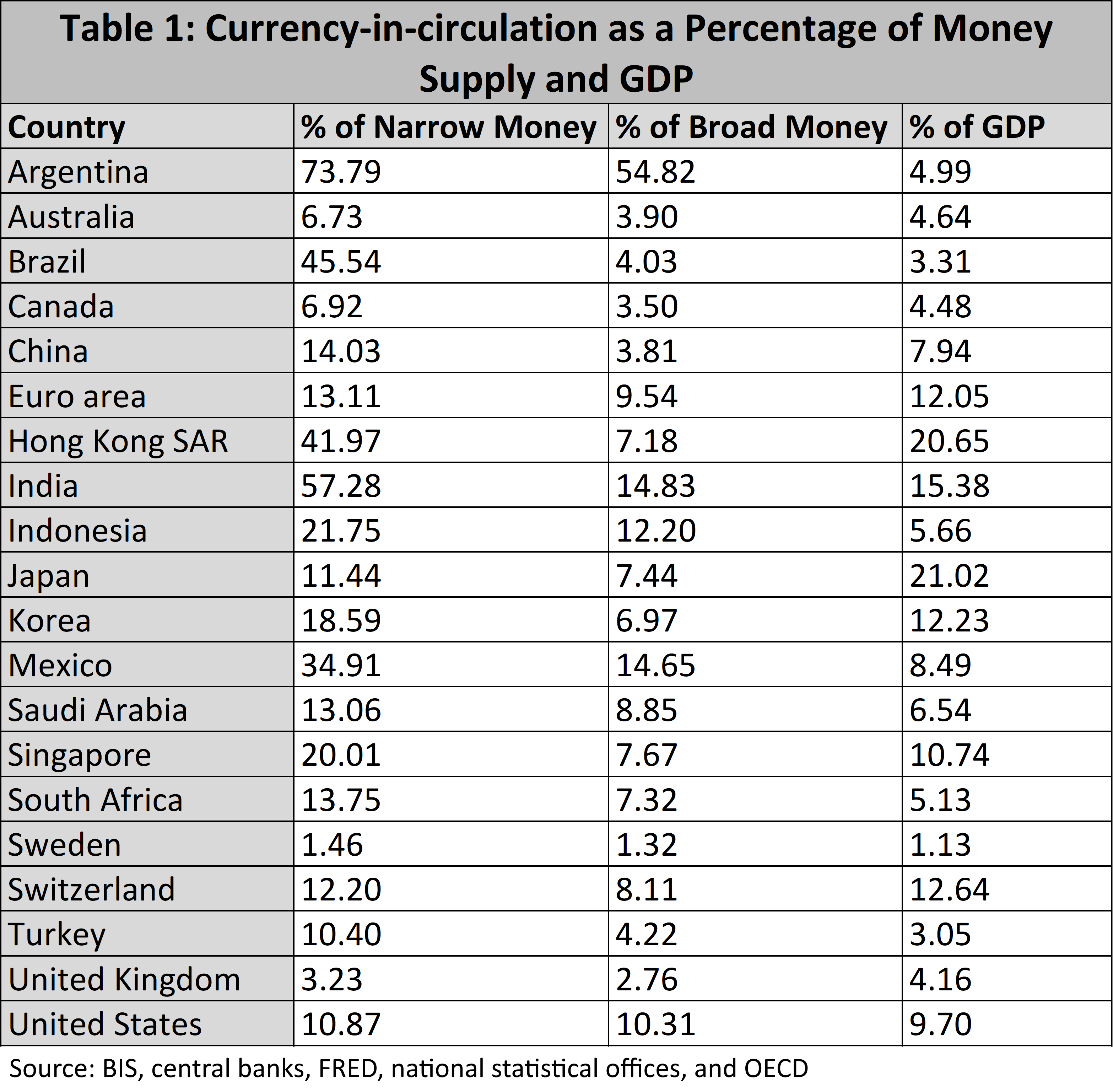

The use of cash among the systemically important economies (G20 economies) shows a mixed picture in both advanced and emerging market economies (Table 1). In countries such as Sweden, the UK, Brazil, or South Africa, cash in circulation is below 5% of the gross domestic product (GDP). In others, notably Hong Kong, India, Switzerland, and Japan, the share of cash is well above 10% of the GDP.

A better gauge of the use of cash is comparing the currency in circulation to broader monetary aggregates, as a share of broad money (M3) and narrow money (M1) respectively. The definitions and components of money supply aggregates such as broad money (M2, M3 or M4) and narrow money (M1) vary among central banks. However, narrow money (M1) in most central banks consists of currency-in-circulation, reserves held with the central bank, and demand and short-term time liabilities of commercial banks. The share of currency in M1 provides a clearer view of the use of digital or electronic money—the lower the share of cash, the greater the use of commercial bank liabilities as a means of payments.

Recent trends suggest that the Covid-19 pandemic may have accelerated the shift to digital (credit) transfers in both advanced and emerging markets (CPMI 2021a). In more than 60 countries, fast payments systems (FPS) allow instant and final payments on a 24/7 basis for person-to-person and person-to-business transactions. The retail payments landscape, mostly privately intermediated, is rich in a variety of payment instruments from debit and credit cards to payment apps and digital wallets that ensure instant online and offline transfers. Simultaneously, RTGS operations are getting synchronised on a near continuous basis for inter-bank settlements (CPMI 2021 b).

[E]lectronic money in the form of bank deposits has substantially replaced cash or even card transactions in several countries. Digitalisation and online platforms are becoming faster, cheaper, and more reliable than before.

Improvements in cross-border payments are equally impressive. New data from the Society for Worldwide Interbank Financial Telecommunications (SWIFT) on its global payment improvements suggests that the average time for processing international payments is around eight hours while the median time between high-income countries could be as low as one and half hours. A vast majority of payments among major economies (both advanced and emerging) are settled on the same day. Delays in reaching the beneficiary account are mainly due to the levels of controls required at the beneficiary bank. Capital controls and processing technology could be contributory factors (CPMI 2022).

The main takeaway is that electronic money in the form of bank deposits has substantially replaced cash or even card transactions in several countries. Digitalisation and online platforms are becoming faster, cheaper, and more reliable than before. A CBDC as a means of retail payments may be cheaper than private electronic payments only to the extent that the public payments systems (central bank) absorbs or subsidises costs. There are no compelling technological reasons to suggest that a CBDC would have a greatly superior outcome.

CBDC and the monetary system

Any discussion on a CBDC must begin with the essential elements of a monetary system, with central bank money (fiat money) at its centre, as a unit of value, and a means of payment (the settlement medium), and a mechanism to transfer payments and settle transactions. A well-functioning monetary system depends on trust, the absence of uncertainty about the value of money (as a unit of account), and stability of that value (price stability). Moreover, it would also depend on an elastic supply of the means of payment (central bank money) and commercial bank money (credit) to ensure the smooth functioning of the economy, a two-tiered monetary system with central bank credit (and interest rates), interbank markets, and bank credit to settle payments between persons and businesses (Borio 2018). Cash is an essential part of the mix whose holding preference is largely demand determined.

In theory, the substitution of cash by digital money should be neutral in its impact if the digital currency (token) is a mere change of form. However, as will be argued, a CBDC is a new form of money unlike any of its previous manifestations. The ability of individuals and businesses to hold and directly make electronic payments using a CBDC has far reaching consequences for the monetary system, not all of them salutary. It would also profoundly affect the way a central bank would manage its monetary operations.

First, some level of disintermediation is inevitable. The shift from deposits to a CBDC would reduce the level of credit in the economy. The larger the shift, the larger the associated reduction in the supply of bank reserves. This would have important consequences for the aggregate demand and supply of money in the economy (Bank of England 2020).

A two-tiered settlement system depends on a fine balance between the supply elasticities of central bank money and bank credit, where the two trade “at par” in all states of the world. Countervailing measures to limit the quantity of a CBDC to the public would alter this balance and could impact the liquidity of the system, particularly if the payment systems shift towards settling in a CBDC. In times of financial stress, a CBDC would trade at a premium over bank deposits in the absence of an elastic supply of CBDC.

[T]he programmable nature of a CBDC makes it impossible to maintain the privacy of payment transactions.

Second, the probability of adverse selection (currency substitution) among competing CBDCs would increase if there are no capital controls or if a CBDC is freely available to non-residents. The effect would likely be exacerbated if the value of the currency is not stable. Once again, the option would be to restrict access to non-residents or impose other forms of control.

In neither of these scenarios are the conditions for a well-functioning monetary system fully met through the ordinary mechanism of demand and supply of central bank and commercial bank money? Instead, the monetary system would have to depend on a variety of controls to ensure the smooth supply of means of payments. While such scenarios are plausible even under current monetary systems, a digital currency could amplify these effects to a degree inconceivable in a cash-based system.

Third, a CBDC differs from the fiat currency, as we understand it, in two important ways. Its programmable nature makes it impossible to maintain the privacy of payment transactions. The entire chain of transactions involving each individual unit of a CBDC is traceable and accessible. Beyond the privacy question, a digital currency can be programmed in ways such that it is no longer a universal exchange of value. A CBDC can be of limited tender for a specific basket of goods or services, or limited by quantities or even for a specific time period.

The normal response to these critical questions is to suggest legal or governance frameworks that would provide the required workarounds. However, once the genie is out of the bottle, it is anyone’s guess how different countries and regimes would use the power of this technology.

Do we need a CBDC?

At the outset, it should be clarified that a wholesale CBDC is a misnomer. It is not a digital version of money, either as a unit of account or as a medium of exchange or, indeed, as a store of value, although it might have some of its characteristics. It is essentially a means of payment or a settlement medium. Therefore, the discussion on the utility of a wholesale digital currency (token) ought to be separated from the concept of a CBDC.

Indeed, there are many advantages and benefits to the use of a wholesale digital asset as a settlement medium among financial intermediaries in the first-tier interbank payments system. Wholesale digital assets could bring substantial progress in cross-border payments both in a bilateral and multi-currency framework. Central bank cooperative initiatives in this area are particularly welcome and desirable.

Attempts to implement a universal CBDC in large economies are, at best, premature, and, at worst, an irreversible transformation of monetary systems as we know them, with far-reaching consequences for the economy and society.

That said, the so-called retail CBDC is a true replacement of fiat money in any jurisdiction. It is what is described as a “universal CBDC” (Cecchetti and Shoenholtz 2021). We argue that attempts to implement a universal CBDC in large economies are, at best, premature, and, at worst, an irreversible transformation of monetary systems as we know them, with far-reaching consequences for the economy and society. A step not to be taken lightly, but with a full understanding of its consequences.

We have already touched upon the potential asymmetrical effects of a CBDC on the functioning of a monetary system. Even if this turns out to be not insurmountable, there are other substantive reasons to consider. These are set out in the reverse order of importance.

CBDC and payments: The ability to make faster, cheaper, and reliable payments is seen as a major advantage of a CBDC. However, the benefits are not so substantial if one considers the rapid digitalisation of the payments landscape and developments such as retail fast payments systems, 24/7 RTGS systems, and numerous non-bank payment service providers and payment mechanisms. A CBDC does not add much value but could, instead, stifle innovation and competition.

Conflict of interest: Central banks have a core mandate to ensure a well-functioning monetary system as a supplier of the means of payment (fiat money), as a supplier of inter-bank credit (liquidity), and as a lender of last resort. This mandate is best served by overseeing payment and settlement systems instead of administering them. Platforms such as PIX in Brazil or UPI in India are shared by all payments providers, banks and non-banks alike. These and numerous other mobile payment services have also boosted financial inclusion. Central bank issuance of a CBDC could potentially make it a monopoly operator to the detriment of these already well-functioning platforms.

Privacy and anonymity are the two key attributes of paper currency that would be eroded by a digital currency. Irrespective of the design or form, a CBDC would be fully traceable.

Currency substitution and currency dominance: A CBDC will have to contend with non-residents holding digital currency. While this can be controlled through technology, it would limit its usability. Cross-border currency could potentially dominate domestic currencies, leading to a loss of currency sovereignty.

Privacy and anonymity: Privacy and anonymity are the two key attributes of paper currency that would be eroded by a digital currency. Irrespective of the design or form, a CBDC would be fully traceable. While this is useful in preventing money laundering and criminal activity, there is the greater danger that an individual’s economic autonomy will be compromised. Institutional safeguards are not wholly adequate as they can be breached, depending on the political system and the regime.

Smart money (Programmable currency): Perhaps the most powerful aspect of a CBDC or digital currency of any kind is its programmable features. A CBDC is not a digital substitute for paper money—it can be modified, withdrawn, restricted, or limited in its usage. Limits can be imposed on how much of and for what purpose the currency may be used. The consumer behaviour could be controlled and nudged in directions according to state policy.

Digital ID and CBDC: Independent of CBDCs, the push towards expanding the use of digital IDs across the world raises concerns about the erosion of privacy and autonomy of the individual. A digital ID is an important element in the design of payments services in many countries, whether at the central bank level or by private banks and other payment providers. Paired with a CBDC, a digital ID can be a valuable resource in the hands of big tech or the state.

Surveillance and state control: A CBDC would be a powerful tool in an authoritarian state. Even in democratic countries, the ability to control and observe makes it a potent means to control the way money may be spent. Coupled with a digital ID, every individual and her money are fully accessible—to be observed, to be monitored, and, if necessary, to be controlled in the way it is used.

Conclusions

Powerful technological forces and a sense of inevitable progress are largely pushing the movement towards introducing a CBDC. The concerns raised here are not new and are generally recognised. However, multilateral agencies and national authorities assume that international standards and principles that enshrine a good governance framework will suffice to manage concerns (BIS AER 2022, Ch III).

Grand projects of the state based on some notion of high modernistic ideology see technology as an infallible means of social progress (Scott 1998). The outcomes are often extreme. States, even democratic ones, quickly adopt technologies that are intended for surveillance to track their citizens. In the hands of an authoritarian state, this becomes lethal.

A CBDC has this power. At its most basic level, the technology behind digital currency could be used to track and trace every transaction along a long chain of transactions. The data obtained from these transactions can be exploited by big tech, private entities, or the state. More advanced levels can nudge, push, and control the use of money in the hands of the public, for benign or malign reasons. Central banks and others need to pause and re-evaluate its use.

Kaushik Jayaram is a former central banker who worked for many years in an international financial organisation. Herbert Poenisch is a member of the International Committee, International Monetary Institute, Renmin University, Beijing, a senior fellow of the Academy for Internet Finance, Zhejiang University, Hangzhou, and a former senior economist at the Bank for International Settlements, Basel.

Acknowledgement: The views are those of the authors and do not reflect the views of institutions to which they are currently, or were previously, associated. The authors acknowledge the research support provided by Pawan Thorat, Pune.