Listen to the podcast by Sudha Narayanan here.

On 5 June 2020, amidst growing concern over the seismic collapse of the economy and the spread of the Covid-19 pandemic, the Government of India promulgated three ordinances relating to agricultural marketing that represented a fundamental reorientation of the existing regulatory framework. In doing so, the central government demonstrated its willingness to use the Covid-19 crisis and the ordinance route to unilaterally push through reforms, without the explicit involvement of the state governments.

By September 14, 2020, these ordinances had been brought to Parliament as legislative bills for “discussion”, approval and have since been passed. The proceedings in Parliament have regrettably been vastly inadequate in highlighting the potential ramifications of the bills and in redressing their many lacunae. Nor did the government use the parliamentary discussion as an opportunity to reveal and clarify its larger vision for Indian agriculture that these bills foregrounded. On 27 September, the bills received presidential assent and were notified in the gazette.

One bill relaxes restrictions governing purchase and sale of farm produce, the second relaxes restrictions on stocking under the Essential Commodities Act (ECA), 1955, and the third introduces a dedicated legislation to enable contract farming based on written agreements.

The three bills need to be read together. They share a premise that they will enable private players to invest in agri-food supply chains more easily, lead to gains in efficiency downstream along the supply chain (and upstream in the input supply chain) and that these gains will be passed on to farmers in the form of higher output prices or lower input prices as the case may be.

To both the uninitiated and those who familiar with agricultural marketing reform, these three bills represent complex issues.

On the one hand, many have hailed the bills as a watershed, while others have critiqued them as sounding the death knell for farmers. Many, such as the former Prime Minister H.D. Deve Gowda, are rightly distressed by the manner in which the bills were pushed through Parliament in a hurry. Some fear that this is the thin edge of the wedge, a dramatic start to an irreversible withdrawal of the state from a critical sector in the economy, paving an easy path for big business. The government has maintained that those who object are being obstructionist and themselves once supported reform; there are widespread accusations that farmers are being misled and confused, instigated by political parties.

To both the uninitiated and those who familiar with agricultural marketing reform, these three bills represent complex issues. This article attempts to provide context to and clarity on these bills, focusing on specific aspects and then analyzes the wide-ranging but uncertain implications for Indian agriculture.

I first outline the context of these momentous reforms—for they are indeed momentous—and describe the key features of these bills. I then discuss why they invoke great anxiety even amongst those who support agricultural marketing reforms. I argue that this discomfort has as much to do with what the bills say as it does with what is left unsaid. Marketing reforms, especially those that involve deregulation and the retreat of the state, necessarily need to be situated in the larger context of state intervention and as such it is essential to have a clearer articulation of the intended trajectory of policy, especially with regard to existing state support. This is especially important because at a time when much of the developed world is re-evaluating the sustainability of their agri-food supply chains, India, as a nation of smallholders, has an opportunity to create a model of agriculture that at its core strengthens collective farmer organizations and small and medium-scale local enterprises, as opposed to behemoths that control entire supply chains.

Agricultural marketing in India

Agricultural market reform in India has historically been a vexatious issue. “Agriculture”, “markets and fairs” and “trade and commerce within the state” are all state subjects in the Constitution (Entry 14, 26, 28, List II, Seventh Schedule). Agricultural markets have therefore been the responsibility of the states. At the same time, the centre has an overarching responsibility via Article 301 to ensure that there is free trade within the country: of ensuring “freedom of trade, commerce and intercourse”.

State-specific laws under the Agricultural Produce Marketing Committee (APMC) Acts thus regulate agricultural trade within states. These typically mandate that purchase of certain 'notified' agricultural commodities be through government-regulated markets (mandis) with the payment of designated commissions and marketing fees. Traders and intermediaries (commission agents) typically require a licence to operate in these mandis. In many states these are mandi-specific licenses issued by the APMC. Many of these acts were introduced in the 1960s to ensure that farmers had access to organized markets. The markets had the benefit of oversight by the government to minimize the risks of exploitation by traders and middlemen.

Though the APMC Act was designed to protect farmers’ interests, it perversely rendered farmers dependent on middlemen, who were financiers, information brokers and traders, all rolled into one. Middlemen perform a critical role that formal institutions have found hard to replace or dislodge. Agents and traders are not all mercenary and trade in the APMC markets is in fact auctioned or tendered in closed bids to the highest bidder. But the nexus between traders and commission agents tends to keep out competition and often leaves the farmer with little bargaining power.

[C]ommodities change hands as many as five-six times from the farmer to the end-consumer. One estimate suggests that removing inter-state barriers to trade can increase farmer prices by 11%.

Agents are known to charge “more than just a commission” for the services they render. Many studies document non-transparent price discovery processes, often through collusive trader behaviour or hoarding as in the case of onions (Banerji and Meenakshi, 2004, 2008; Madaan et al, 2019). Consequently, farmers are reported to receive but a fraction of the price paid by the final consumer with middlemen cornering a large part of the rest (Mitra et al., 2013). More critically, the prices farmers get, coupled with low yields, are often inadequate to cover their costs or for servicing debts and meeting their consumption needs. Research on agricultural markets in India has typically concluded that they are inefficient, characterised by a high level of wastage (Mattoo et al., 2007; Umali-Deininger and Deininger, 2001 are examples).

Further, the large variation across states in the scope and stringency of these APMC Acts has led to fragmented markets that have impeded the emergence of a single national market. Consequently, commodities change hands as many as five-six times from the farmer to the end-consumer. One estimate suggests that removing inter-state barriers to trade can increase farmer prices by 11% (Chatterjee, 2018).

While states have jurisdiction over the APMC, the Essential Commodities Act (1955) bestows the centre with wide-ranging powers to impose restrictions on storage and movement of certain ‘essential’ commodities by private parties, mainly to protect consumer interests. State governments are free to set stocking limits based on the centre’s notifications. The ECA, often described as “draconian”, is seen as thwarting private investment in post-harvest storage, warehousing and processing, especially because these controls are implemented somewhat arbitrarily. Historically, ECA-related restrictions have been neither predictable nor infrequent. And since restrictions are imposed temporarily, typically, for six months or a year at a time, the attendant uncertainty hinders operations of agribusinesses, logistics firms and traders alike.

As for contract farming—the third area of reform—since the APMC Acts at the state level govern all forms of marketing transactions, the decision on whether to permit contract farming too was left to the state governments. Whereas some states have allowed contract farming for years, others continue to implicitly disallow it. Except for rare attempts by states like Punjab, which proposed a dedicated act for contract farming, contract farming has thus far not been governed by a special legislative framework.

Bumpy road to reform

Ever since India embarked on liberalizing its economy in 1991, there has been an attempt to reform the APMC Act and the ECA. Critics felt that the two laws had perhaps overextended their reach, compromising farmers in favour of trader-middlemen and consumers. Further, with the growth of private sector participation and export-orientation in processing industries following delicensing, access to and control over the source of feedstock to ensure quality and traceability became desirable.

In 2000, as part of what was termed a ‘Rainbow Revolution’, the National Agricultural Policy stated: “private sector participation will be promoted through contract farming and land leasing arrangements to allow accelerated technology transfer, capital inflow, and assured market for crop production ...” The vision for agriculture, then as it is now, involves private players spearheading a transformation of Indian agriculture, providing capital, inputs, technology and market access, with investments in storage and handling that would lead to less wastage and greater efficiency.

It would be fair to say that agricultural economists in India, despite differences, have been more united on the need for marketing reform than on any other issue. Indeed, over the past two decades, many committees have consistently made remarkably similar recommendations, so that one well known economist declined to be on yet another committee that would say the same thing. Farmers and farmer-activists likewise have consistently recognized the need for farmers to get fair and remunerative prices and the failure of the current APMC-centric system to secure them.

After a brief attempt to incentivize state reform in agriculture via Finance Commission allocations, the central government appears to have opted for a less federalist approach.

Yet, since agricultural market reform was the domain of the states and powerful lobbies of traders and their nexus with politicians in many states blocked reform, successive governments at the centre have historically faced huge challenges in pushing through any reform that would take all states forward at the same pace. Hitherto, efforts at harmonizing state-level laws have taken the form of appeals and entreaties by the centre urging them to reform the APMC along prescribed lines, the most recent recommendation being the Agricultural Produce and Livestock Marketing (Promotion and Facilitation) Act, 2017.

As part of these attempts, a longstanding proposal to integrate markets across states took the form of the electronic National Agricultural Market (e-NAM)—an effort to enable inter-state trade by establishing an online trading platform that would integrate markets across states. However, this too was predicated on states aligning their laws to enable the e-NAM. Many states have indeed embarked on reforms but to varying degrees and at varying, often glacial, pace. Given this record, the Economic Survey 2014-15 noted that “if persuasion fails (and it has been tried for a long time since 2003), it may be necessary to see what the center can do, taking account of the allocation of subjects under the Constitution of India.” This bolsters the view that it would be well within the central government’s remit to pass laws unilaterally for a unified national market (Entry 33 and 42 within the List III, Seventh Schedule). After a brief attempt to incentivize state reform in agriculture via the Finance Commission allocations, the central government appears to have opted for a less federalist approach.

The passing of the three bills thus represents a culmination of a prolonged effort to change the regulatory environment of agricultural markets to allow more room for private players, while allowing farmers to connect with non-traditional private players in agricultural markets.

What are these three bills?

Each of the three bills deals with one aspect of agricultural marketing. Collectively, they are designed to reduce barriers that diverse agri-food supply chain actors face in connecting to farmers. They aim to do so by reducing reliance on traditional APMC-based intermediaries (‘disintermediation’) and by creating a unified national market ( “one nation-one market”). Despite the titles of the bills highlighting ‘farmers’, rather than focusing directly on farmer welfare all three bills rely overwhelmingly on supply chain actors to take advantage of the new rules and share their gains with the farmers.

The first, and perhaps the most far-reaching and controversial, is called the Farmers’ Produce Trade and Commerce (Promotion and Facilitation) Bill, 2020. This bill attempts to bypass the state-level APMC Acts and can hence be referred to as the ‘APMC Bypass bill’. 1 These abridged names were proposed by Kiran Kumar Vissa; I will use this for convenience. This bill limits APMC’s oversight and jurisdiction to the APMC ‘market yard’. Outside of the market yard, entities are free to transact in agricultural produce in what would be referred to as the ‘trade area’. Thus, a trade area is where trade happens that is not already under APMC (Section I.2.m). Transactions in the trade area are free of an obligation to pay a fee to the APMC and no licences are required by buyers. These trade areas across the country therefore constitute an alternate marketing space that purports to operate seamlessly across the country.

At first glance, it would seem that given all the structural problems with the functioning of agricultural markets in India, these three bills are cause for unbridled joy.

The preamble promises that the bill focuses on “creating of an ecosystem where farmers and traders enjoy freedom of choice”, there are “competitive alternative trading channels” that “promote efficient, transparent and barrier-free inter-State and intra-State outside APMC” (Section II.4.1). This bill also aims at a “facilitative framework for electronic trading”. The APMC Bypass bill thus also permits electronic trading platforms. Permitting trade areas and electronic platforms thus wrest control from state governments since the states no longer have jurisdiction over either of them.

The second is the Essential Commodities (Amendment) Bill, 2020 that attempts to remove the arbitrariness and unpredictability in notifying stocking limits, by linking it to transparent rule-based price triggers. Accordingly, a form of restriction will be deployed only in “exceptional circumstances”. The bill suggests that for horticultural produce, stocking limits can only be invoked if there is a 100% increase in retail price and 50% increase in retail price of non-perishable agricultural foodstuff, using a base price. The base price would be the retail price in the preceding 12 months or the average retail price of the last five years, whichever is lower. There are currently debates on whether these are too high to be relevant or too low so as to the render the amendment meaningless, but this bill has generated comparatively less controversy. There is a view too that removing the threat of stocking limits would be especially welcomed by large businesses that hitherto found this to be a constraint.

The third ordinance, the Farmers (Empowerment and Protection) Agreement on Price Assurance and Farm Services Bill, 2020 is more easily referred to as the ‘Contract Farming bill’ and aims to provide a framework for written agreements between farmers and sponsors without mandating them. It allows ‘Sponsors’ to engage with farmers via written contracts, if they choose to use such contracts. Unlike the APMC Bypass bill, the contract farming legislation has a longer history of extensive consultations with stakeholders. Yet, bewilderingly, the 2020 bill seems to have broken with the past by abandoning the 2018 proposed model contract farming act in favour of a national legislation.

The new effort is a lighter framework that permits contract farming with minimal obligations. A second significant departure is the expansion of the scope of the bill to include farm services, i.e., “supply of seed, feed, fodder, agro-chemicals, machinery and technology, advice, non-chemical agro-inputs and such other inputs”. The Contract Farming bill explicitly excludes land leasing and forbids the Sponsor from erecting built structures on farm land. The bill also provides for timely payments by the Sponsor to the farmer. As with the APMC Bypass bill, this bill frees downstream players in the supply chain from state APMC regulations, enabling them to undertake written contracts freely across the country, outside the purview of any ‘State Act’ or ECA (II.7.1 & 2)

Commentators have predictably hailed the passing of these three bills as a game changer, the 1991 moment for Indian agriculture. These would “unshackle” the Indian farmer, fulfil the dream of a “one-nation, one-market” and bring farmers up to speed on “futuristic technology”. At first glance, it would seem that given all the structural problems with the functioning of agricultural markets in India, these three bills are cause for unbridled joy.

[T]he three bills indeed change the rules of the game dramatically. However, in their current form, will the perceived benefits materialize? The outcomes are unfortunately highly uncertain.

After all, the bills mark a significant departure from the anachronistic APMC Acts that did not keep pace with the rapidly evolving agricultural supply chains in the country. In recent years, agri-tech start-ups have proliferated in India and estimates suggest that one in nine agri-tech start-ups worldwide is established in India, relying on venture capital to rapidly scale up their businesses and impact. A 2019 NASSCOM report asserts that India’s agri-tech start-ups had a delightful year: by June 2019 they had raised funding to the tune of $248 million, compared with $73 million in all of 2018. More than 60% of the funding was directed to those working on market linkages. Crop advisory services and inputs are other key areas.

Social enterprises centred on producer well-being too have emerged in a big way (Kanitkar and Chebrolu, 2019). Farmer Producer Organizations (FPOs) are the `new age cooperatives’, despite the challenging issues they face in becoming viable enterprises. Organized retail and food-tech companies are growing rapidly as well, with even traditional grocery stores modernizing their backend, demanding strong backward linkages with producers. Many of these start-ups have also become vehicles for delivering financial and extension services, strengthening smallholder access to modern technology. The Covid-19 lockdown too has accelerated many of these trends with new players.

All the three bills lower entry barriers for these new players and reduce the costs of transactions in the new trade areas. Although in many states these players are already thriving, these bills could potentially expand the number of players, from the stream it is today into a gushing river. There are clear opportunities for such enterprises to explicitly serve the interests of the farmer in multiple ways, especially those driven by social goals or farmer-based organizations.

Yet even those who have been strong advocates of reform along these lines have been left with deep misgivings about the three bills, asking if this is in fact the reform we need. In other words, the three bills indeed change the rules of the game dramatically. However, in their current form, will the perceived benefits materialize? The outcomes are unfortunately highly uncertain. Some of this uncertainty is on account of some glaring lacunae in these bills; some of it also relates to the fundamental premise of this approach and the future of state intervention in Indian agriculture.

In the next sections, I focus on the many lacunae in the three bills and then offer a perspective on why the anticipated gains of this reform package might not materialize or be modest at best, with potentially perverse consequences if the shortcomings remain unaddressed.

Missing pieces

In principle, the designation of trade areas across the country that are free from APMC regulation is designed to create a seamless national market. Yet, in the current APMC Bypass bill, there is no obvious mechanism by which a single national market will emerge. First, facilitating the emergence of many electronic platforms that are disconnected from each other would imply fragmentation rather than unification. The APMC Bypass bill does suggest that these platforms may be interoperable, but without ensuring interoperability it is unclear how these markets will function as parts of a whole. Second, under the new trade areas we face another bewildering prospect. As of today, private players, where they operate, tend to look to the APMC markets to guide their own transaction prices outside the mandi. If players in the trade areas continue to use APMC markets to guide the prices they pay, then the APMC continues to influence prices in new trade areas,. In this case, although savings in mandi fees may be passed on to the farmer, private players might not provide a meaningful alternative to the APMC mandis. Considering that the non-transparent price discovery mechanism in APMC is supposedly the evil that the new bills sought to redress, this is not a significant break from current practice.

All three bills collectively invisibilize trade area transactions, contract farming and stocking in a way that makes them unregulatable.

If on the other hand, the APMCs decline in importance and influence, and cease to offer a reference price, then what replaces the APMC as the source of price signals? In the absence of a thick market with many players and high traded volumes, transactions in the new trade areas could splinter into bargaining islands, leaving price setting to the relative bargaining power of the farmer vis-à-vis the buyer. The outcome of such a system looks disturbingly like that of the structure it seeks to replace.

Perhaps a greater problem with the three bills is not what they attempt to do, but what they do not do. In general, they lack a transparent recording of transactions and a credible regulatory architecture. All three bills collectively invisibilize trade area transactions, contract farming and stocking in a way that makes them unregulatable.

Perhaps the most problematic aspect of the bills is that there is a complete absence of regulation and regulatory oversight for both the new trade areas and for the new electronic platforms that might emerge. Agricultural transactions especially at the point of first sale are notoriously challenging to regulate and there is often agreement that practically speaking it is impossible to do so. At the same time to not regulate any of the transactions that bypass the APMC is bewildering, to say the least. India’s experience with dairy deregulation in 1991 is instructive. Delicensing of dairy firms resulted in chaos with the emergence of a large number of dairies purveying contaminated and adulterated milk. The government then brought in the Milk and Milk Products Order in 1992, recognizing that deregulation without safeguards has its own perils.

Even if a rudimentary regulatory framework were established going forward, it is unclear how multiple regulatory systems would coexist and function. As per the current APMC Bypass bill, all existing trading places, both private market yards and warehouses, that have been declared as market places under the APMC Act would fall under the jurisdiction of the APMCs, but not those that are new. Rajasthan, for example, notified several warehouses under the APMC Act after the ordinances came into force, presumably to be able to retain control over more market areas within the state. A fragmented regulatory structure can be a huge disincentive for most private players, though larger businesses may be better placed to navigate regulatory complexity.

[I]t is eminently possible that the cartels within the mandi will now efficiently reorganize outside the mandi to escape regulation and detection.

Price information and market intelligence find mention in Section II7(1) and (2) of the APMC Bypass bill, but only as something that the government “may” do. Thus, although the bill uses the word “transparency” several times, the failure of a clear mechanism to record, collect and collate data renders all transactions in the new trade areas invisible and the entire marketing system opaque. There is no obligation for anyone in the trade area to record or report details of the transaction. The sole proof of transaction itself lies in a receipt that farmers are supposed to get upon delivery, which is left entirely to the buyer and the ability of the farmers to demand and insist on one (even on electronic platforms). Likewise, it also invisibilizes stock holdings, given that registration and reporting are not mandated, unlike those registered warehouses under the Warehouse Development and Regulatory Authority. Indeed, some commentators have called for mandatory registration of warehouses to overcome this lapse.

This complete absence of data and market intelligence is cause for concern. It is worth recalling that the Competition Commission of India’s extensive inquiry into collusion of onion traders in Lasalgaon involved, among other things, a detailed analysis of prices and arrivals relying on data recorded in the APMC mandis. Differently, data scientists have relied on anomaly detection techniques based on publicly available data to identify periods when prices in retail horticultural markets departed from what would be expected given the prevailing conditions. The absence of data is a serious obstacle towards efforts to ensure contestability and competition among buyers, which are the purported goals of the APMC Bypass bill. Indeed, it is eminently possible that the cartels within the mandi will now efficiently reorganize outside the mandi to escape regulation and detection. The absence of recorded data also hampers clear identification of needs for crucial decisions, especially on issues such as trade policy and food security.

Another notable weakness is the dispute resolution mechanism. It is developed at length both in the bills and in the rules, but it is weak at best putting the onus virtually entirely on the farmers. Indeed, the basis of the dispute resolution mechanism relies on a receipt the farmer receives as proof of the transaction and on the sub-district magistrate, rather than the civil courts. It is unclear how this will resolve interstate disputes and disputes over complex issues (such as quality, weighment, etc.) on the basis of a receipt, or of more complex issues relating to electronic platforms.. The dispute resolution process for the Contract Farming bill too is not a credible recourse for a farmer, for reasons discussed later.

[T]hese bills represent the right kind of reform done the wrong way and to correct course would require a mammoth effort going forward.

There are also gaps in the specification of rights over data. The entry of private agri-tech players and as the Prime Minister noted of “futuristic technologies” that develop data stacks of farmers requires careful thinking. The current version makes no references to any of these issues and data rights seem to poorly defined if not altogether ignored.

These lacunae are worrying because they might very well not translate into the benefits that the government hopes for or worse put farmers at a deep disadvantage. In that sense, these bills represent the right kind of reform done the wrong way and to correct course would require a mammoth effort going forward.

Uncertain outcomes

Beyond the flaws in these bills, we need to re-examine the central premise that private players will pass on the benefits of lower costs and efficiency gains to the farmer while competing with each other.

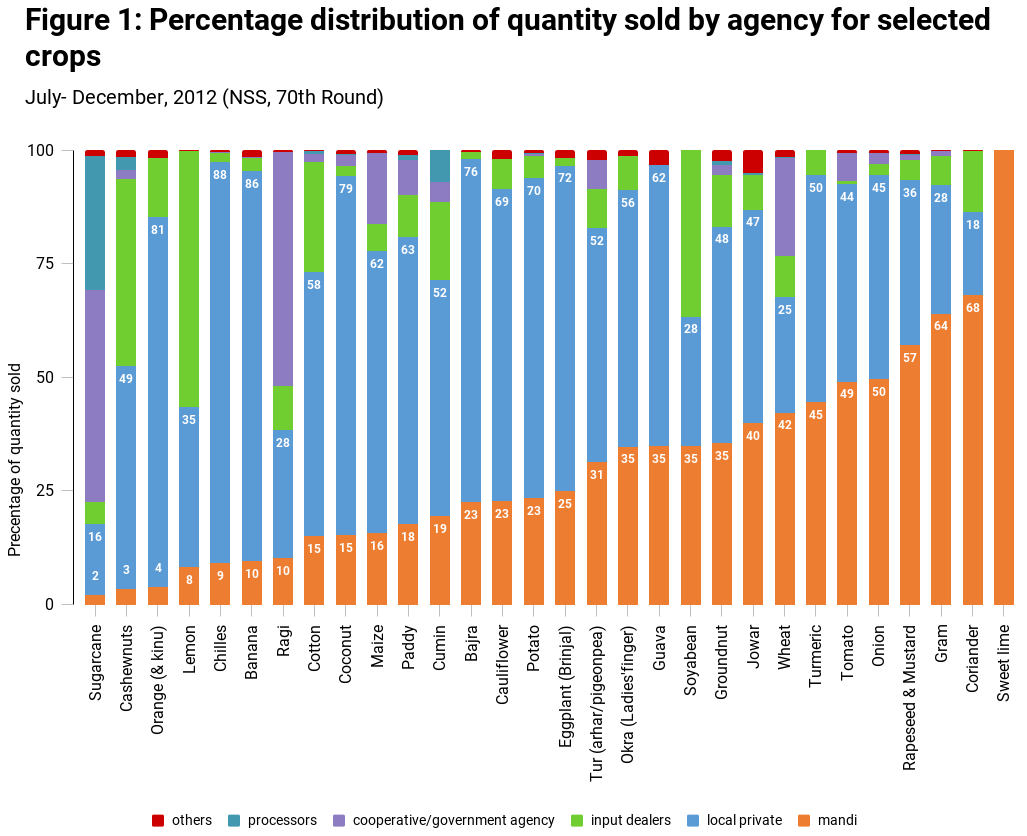

First, we examine the incremental contribution of these bills. Many commentaries erroneously suggest that so far farmers had no choice but to sell their produce to rapacious middlemen operating in the mandis. This is far from the truth (Figure 1). Nationally representative data of agricultural households suggests that only 25% of all transactions in India during 2012-13 passed through these mandis, whereas 55.9% were sold to private traders. Even before these ordinances were passed, a number of states had already reformed their APMC Acts allowing for private players to set up market yards, undertake contract farming, purchase produce directly from the farmers and so on (Purohit, 2016). A series of measures spanning 2012-15 denotified several horticultural commodities, freeing them from the requirement that the first sale be at the APMC yard. Cotton ginners and spinners, solvent extractors, sugar, oil and dal mills have historically been procuring directly from farmers in several states. Karnataka, for example, pioneered deep market reforms early this decade, unifying markets via an electronic trading platform and simplifying licensing procedures throughout the state.

Six states already deem warehouses to be marketplaces, permitting warehouse-based sales. A few states enabled this during the Covid-19 lockdown. States such as Kerala, Bihar and Mizoram have had no APMC Act to speak of, implying unrestricted private trade. Uneven and ineffective implementation notwithstanding, it is not the case that the APMC is the monopoly purchaser of commodities. Indeed, with the growing diversification of crops and the diversity of market players, non-APMC channels have consistently accounted for an increasing share of the purchase. Thus, commentaries that suggest that the APMC had shackled the farmers are disconnected from reality. Indeed, the NASSCOM report of agri-tech enterprises cited earlier reports that whereas 39% of the agri-tech start-ups interviewed indicated finance was a constraint, fewer (29%) indicated policy as a constraint. FPOs too face constraints of human capital and finance rather than regulatory barriers.

Many argue … that the need of the hour is not to privilege greater private participation at the expense of the APMC…but to strengthen existing public marketing infrastructure and systems.

If anything, there has been a longstanding demand from farmers to have more markets that farmers can easily access. In Mizoram, for example, where market access is a big constraint and one of three states that has not notified the APMC Act passed in 2008, farmer groups have been demanding implementation of the act. As per the State of Indian Agriculture, 2015-16, while the all-India average area served by a regulated market is 449 sq. km, the density varies widely across the country — from one per 119 sq. km in Punjab to one per 11,215 sq. .km in Meghalaya. The National Farmers Commission (2004) had recommended that a regulated market should be available to farmers within a radius of 5 km (corresponding to a market area of about 80 sq. km).

Here, the bills certainly incentivize private players to directly transact with the farmers. At the same time, the history of agribusiness engagement suggests that there are strong placement effects. Businesses are highly selective in which geographies they work in, often choosing areas with less competition, better infrastructure, skilled farmers and higher productivity. Many agribusinesses also select larger farmers rather than smallholders to reduce the transactions costs of operation. Small and marginal farmers often sell to input dealers, itinerant traders and other supply chain actors, at far lower than market prices because the transport costs of visiting a mandi simply does not make economic sense. For this group, it is unlikely that these bills lead to an expansion in potential buyers. The benefits of competition among buyers, if at all, would therefore not be widespread, instead benefitting those farmers who have strong locational and competitive advantages. In many cases, therefore, the absence of private players might be on account of systematic disadvantages of operating in certain geographies, rather than regulatory barriers. The limited presence of organized private players in Bihar, where the APMC was abandoned, is likely reflective of this. These suggest the continued need for a strong state-supported marketing infrastructure, especially in marginal areas. Many argue therefore that the need of the hour is not to privilege greater private participation at the expense of the APMC, especially when private business are already important participants, but to strengthen existing public marketing infrastructure and systems.

As for contract farming, the Indian experience is unenviable, working only for a few niche commodities where competing domestic markets do not exist and in specific geographies. In reality, the legal framework for contracting has been largely immaterial to agribusiness decisions on whether or not to contract and whether it takes the form of a written contract. In that context, the Contract Farming bill is unlikely to encourage a growth of contracting. On account of the small size of farms and small transaction volumes, it is immensely expensive for firms to contract with a large number of smallholders. Many therefore prefer to contract with intermediaries, who aggregate produce from farmers, or to procure from the APMC mandis themselves. Further, widespread breach of contracts by both farmers and firms have meant few contract farming schemes survive beyond a few years. Most contracting firms tend to use the mandi price to benchmark the contract price, rather than offer a guaranteed price for contracted produce (which the bill mandates), in part to prevent breach in the event of price spikes in the local market.

[T]here is also a fear that big businesses might embrace contract farming not so much to guarantee markets or prices but to exercise indirect control over farm land in the guise of securing farmer services.

In general, neither farmers nor agribusinesses in India are keen on written agreements, preferring to rely on trust and mutual understanding to sustain the relationship, albeit for different reasons. Farmers often fear written contracts and even when they don’t, they are unlikely to be able to seek formal dispute resolution. Firms, on the other hand, only use written contracts to demonstrate seriousness of intent and, even in this case, they are unlikely to ever enforce the contract, except to sound out a warning to all contract farmers. Typically, though, as one business said: “we would never take a farmer to court; it would jeopardize relations with all the farmers and not just the one who defaulted”. The current Contract Farming bill thus appears to overestimate the enthusiasm of agribusinesses to enter into contracts. That said, there is also a fear that big businesses might embrace contract farming not so much to guarantee markets or prices but to exercise indirect control over farm land in the guise of securing farmer services.

A second well-entrenched myth is that traditional supply chains in India are associated with intolerably high wastage and this is provided as a justification for large-scale private investment along the supply chain. These claims have thus far relied largely on ghost statistics. A careful recent work on this by the Indian Council for Agricultural Research shows that the post-harvest losses of various commodities range from 3.9-6% for cereals, 4.3- 6.1% for pulses, 5.8-18.0 % for fruits and 6.8-12.4% for vegetables. These suggest much scope for improvement but are not compelling evidence of the failure of existing supply chains. The evidence of impacts upstream on technology adoption is equivocal as well. On the one hand, we have examples that suggest that businesses can transform the way farmers do things. Pepsi is widely credited with teaching farmers to grow tomatoes on raised beds, increasing yields. Yet, the evidence is mixed. Existing work on dairy supply chains for example suggests that technology adoption and the adoption of safe practices does not improve significantly when linked to modern supply chains. This is not to dismiss the potentially large benefits that private firms can deliver to the farmer, especially in the context of weak public extension systems, but it is important that these claims are not overstated.

Third, the three bills are designed to foster contested markets where multiple buyers will bid up prices that therefore benefit farmers. This is certainly true, especially when buyers are not all local, making it hard to collude. My own research on contract farming suggests that where multiple firms contract for produce in the same village, it is hard for agribusinesses to short-change the farmers. That said, it is not clear that non-traditional buyers won’t themselves collude or in their own words, “coordinate” on pricing. Contracting firms that operate in clusters often agree on prices before the season and commit to not outpricing each other. Further, it is not uncommon for buyers to carve up territories so as not to step on each other’s toes.

Globally, many also note that initially cost savings by agribusinesses are passed on to farmers who are then subsequently and gradually squeezed over time, a phenomenon referred to popularly as `agribusiness normalization’. It is also common enough that businesses end up consolidating, so that whereas farmers enjoy the advantages of multiple buyers initially, they end up facing a single buyer eventually. In each of these cases, there is a high likelihood that new players will offer better access to markets for farmers, but it is eminently possible that this happens without leaving them significantly better off monetarily. If anything, the power imbalance between large business and farmers is often far greater than those between local traders and farmers.

The presence of large agribusinesses can also thwart farmer collectives. Verghese Kurien reflected on his failure to nurture dairy cooperatives in Sri Lanka, where the then minister is quoted as saying that he was a “Nestlé man” (Kurien 2005, 165) and dairy cooperatives were therefore a non-starter in Sri Lanka. At other times, cooperatives and small players end up growing so large that they behave like multinationals themselves.

[T]he view that a transformation of the agricultural marketing ecosystem will deliver benefits to the farmer rests on fairly thin evidence.

It is instructive too to look at farmer wellbeing in models where agribusiness has been consolidating over the past decades. In the US, in 2018, the farm share was 14.6 cents of each food dollar expenditure. The European Commission noted in response to a 2015 question in its parliament that the “value added for agriculture in the food chain dropped from 31% in 1995 to 24% in 2005, mainly in favour of other food chain actors”. By 2011 it was 21%, versus a value added of around 28% for the food industry and 51% for food retail and food services, suggesting that the highest value addition occurred at points in the supply chain farthest from the farmer, accruing to non-farm actors in the chain! In contrast, the Indian numbers compare surprisingly favourably. A 2012 study estimates that farmers obtain 37 and 48 per cent of the retail price of fruits and vegetables in Gujarat. A recent study by the RBI in 2018-19 notes that the farmer’s share in consumer’s rupee ranged between 32% and 68% for horticulture, 40-89% for foodgrains and oilseeds (RBI, 2019).

Interestingly in farmer’s markets like the Uzhavar Sandhai in Tamil Nadu and Rythu Bazaar in Andhra Pradesh, farmers get 15-40% more than the prevailing mandi/wholesale prices and consumers pay 15-30 % less than retail prices (GoI, 2007). This is not to suggest that farmers are doing well under the current system—in many existing commodity chains, they do not—but the view that a transformation of the agricultural marketing ecosystem will deliver benefits to the farmer rests on fairly thin evidence.

Fourth, the three bills also imagine that disintermediated trade without traditional middlemen will shorten supply chains and the benefits would accrue to farmers and consumers alike. There are a number of models where this is indeed the case, the farmers’ markets above being a good example. At the same time, as discussed earlier, given the small size of farm holdings, it is extremely challenging and expensive for private enterprises, especially small enterprises, to directly engage with farmers, especially across states with payments within the time period stipulated in the bills. For example, in the early days of its entry into food processing, a company official of a firm that focussed on exports noted “I can manage ten or twenty farmers, but not thousands” (Witsoe, 2006).

The emergence of Business-to-Business models among agri-tech firms… suggests that these firms end up as intermediaries connecting large retail with farmers, implying reintermediation rather than disintermediation of the supply chain.

In reality, most large firms are able to contract with around 5,000 farmers, but typically to do with fewer than a thousand. Disintermediated trade is unlikely to grow for inter-state trade where existing private players would rather rely on intermediaries to procure the volumes they need, inspect for quality and organize the logistics, rather than engage directly with a large number of small players. Indeed, it is eminently possible that rather than serve as alternatives, FPOs and agri-tech platforms are co-opted by the large businesses who control logistics and retail as participants in their supply chains. For example, in the 1990s, the Central Arecanut and Cocoa Marketing and Processing Co-operative Limited (CAMPCO), was using its chocolate factory to produce for Nestlé, until the agreement soured because Nestlé wanted to take over the factory rather than contract with the cooperative. The emergence of Business-to-Business (B2B) models among agri-tech firms, less challenging to agribusiness than Business-to-Consumer (B2C) models, for instance, suggests that these firms end up as intermediaries connecting large retail with farmers, implying reintermediation rather than disintermediation of the supply chain. While substantial gains may exist for these players, it is a moot question on what the farmers’ position in these chains will be.

Thin edge of the wedge

The bills, the benefits and flaws notwithstanding, raises fundamental and discomforting questions on the larger vision that the current government has for Indian agriculture. Indian agriculture is led by smallholders. Here was an opportunity to chart out a creative growth trajectory for this sector that avoids the pitfalls of models followed elsewhere in the developed world, that result in consolidation not just of agribusinesses but also of farms. It is not an accident that across the world there has been a call to break up big business and efforts to rethink agri-food supply chains. Nor is it an anomaly that even as large efficiency gains are made along the supply chain with increasingly sophisticated technologies and large-scale enterprises, the extent of state support to farmers in these countries has been increasing.

A model that would work for India needs to focus on strengthening collective enterprises and small- and medium-scale local enterprises that can flourish and operate without the often-self-destructive pressure of serving investors or without having to consolidate to survive. Where private players drive the sector, it is crucial to have a regulatory framework to safeguard farmer interests with appropriate checks and balances. It is also imperative to strengthen state support to complement private participation. The role of the state is in fact more important than ever before.

The three bills on reforming agricultural markets mean little to the farmers without a coherent vision and blueprint for Indian agriculture that places them in context.

The bills therefore need to be discussed in the context of the larger question of state intervention in agricultural marketing, including price-based intervention, procurement and foodgrain distribution, on the one hand, and public investments in infrastructure and institutions, including the existing APMC system, on the other. Here, the government’s efforts have been disappointing at best. Decisions to ban the export of onions and effect a measly 2.6% increase in the Minimum Support Price for rabi wheat in 2020-21 hardly reassures a sceptical farmer that the government has farmer interests in mind or that public support systems would not be weakened, especially when big businesses have been roped in to handle foodgrain storage for an assured guaranteed return for the next 30 years.

Bypassing the states in passing these laws has already triggered a race to the bottom, where some states have begun reducing mandi charges to assuage the traders and middlemen, leaving less revenue for investments in strengthening public infrastructure. Budgetary allocations so far to strengthen the existing mandi system, whether for e-NAM, the APMCs or rural village markets (GrAM) have been woefully small. The commitment to creating 10,000 FPOs by 2024, though in the right direction, ironically seems to lack understanding of the challenges of setting up viable collective enterprises. Current decisions of the government therefore barely inspire confidence.

The three bills on reforming agricultural markets mean little to the farmers without a coherent vision and blueprint for Indian agriculture that provides the right context. To suggest that protesting farmers are misled or confused is to evade these crucial issues. The way forward for the government is to revisit and rethink the newly enacted legislation and provide clarity on the vision it has for Indian agriculture. It must do so not by bypassing the states and its farmers but by including them.