Amid the government’s consistent claim that the Indian economy was performing better than most other major economies came Prime Minister Modi’s unexpected call to citizens to exercise austerity while spending in foreign currency. He urged citizens to defer purchase of gold and unnecessary foreign travel, reduce consumption of essential items, including edible oil, petrol and diesel, and increase purchases of products produced domestically. The prime minister’s alarm bell was not merely a reality check on the “Achhe Din” narrative that the government had built since it came to power in 2014, but it also triggered questions about the state of India’s macroeconomy, even by those who had assiduously supported the government.

Ample justifications exist for the questions being asked of the government about the country’s economic performance.

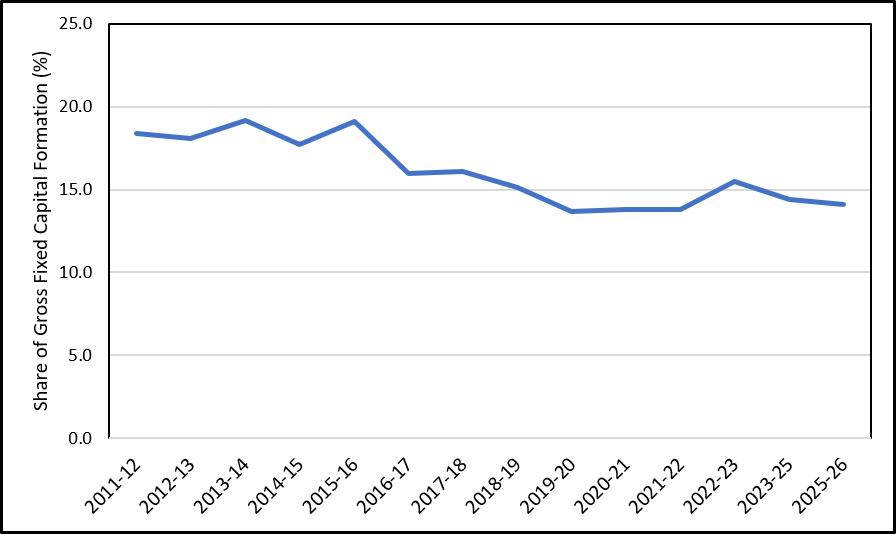

One major factor has been the continued lack of enthusiasm of the private sector to invest in capacity creation in the country, which is an important indication that all’s not well with the economy. The share of private investment in machinery and equipment fell almost consistently after peaking in 2015-16. (Chart 1) The post-Covid government stimulus briefly broke this trend before the downward trend resumed.

Chart 1: Share of Private Investment* in Machinery and Equipment in Gross Fixed Capital Formation

The lack of enthusiasm among private investors forced the central government to step up its capital expenditure. While in the four years prior to the onset of the pandemic, central government capital expenditure was, on an average 1.7% of the GDP, in the four years after the Covid-reset, i.e. from 2022-23, this has increased to 3.1%. In fact, in her budget proposals for the current fiscal year, the finance minister had increased budget support for capital expenditure by almost 12%, and as a result, central government’s capital expenditure is expected to be at a record level of almost 3.31% of GDP.

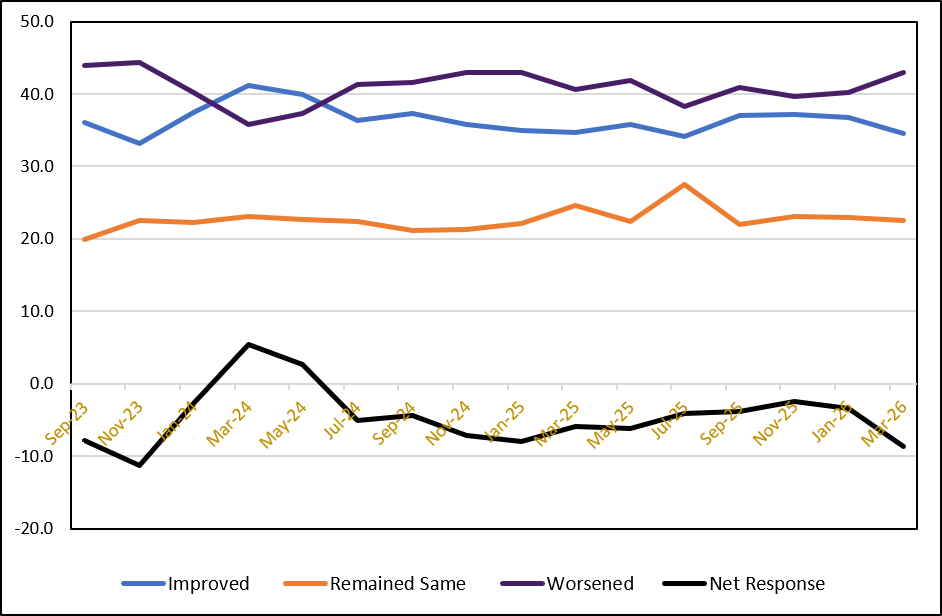

The sustained weakness of private investment can be attributed to the downbeat consumer confidence that has become a constant feature of the post-Covid years. Though the government has been crediting an uptick in private final consumption expenditure for the 7+ percent annual growth, the RBI’s bi-monthly consumer confidence survey showed that consumer confidence has been at a low ebb even after the Indian economy came out of the depths of the pandemic-induced downturn (Chart 2). This seems to explain the weakness on the demand side of the economy, as also the lack of incentives for the private investors to invest. That private investors would refrain from creating additional production capacities in the face of depressed demand, is almost axiomatic.

Chart 2: Perceptions and Expectations: Consumer Confidence

Besides these factors that are critical for maintaining the growth trajectory of the Indian economy, the long drawn-out conflict in West Asia, could affect the Indian economy significantly. The government seems to have identified the rising expenditure in foreign exchange as an immediate area of concern, which was evident from Prime Minister Modi’s urgings to the citizens to reduce spending on several products having a high import content.

It is not only that increasing foreign exchange outgo on the merchandise trade account is an area of concern. India’s capital account has also witnessed relatively high levels of outgo at least for the past three years. In this article we elaborate on the nature of the problems that India’s external sector faces and will try to identify the key contributory factors. Our view is that the government must prepare a medium-term strategy without which the external sector may not be able to recover from its weaknesses. We would begin by discussing the vexed situation on the current account, largely due to the steep increase in merchandise trade deficit. In the second section, we would analyse the weaknesses on the capital account.

1. India’s Merchandise Trade Account Problems

The prime minister’s announcement is directly related to the delicate situation India is facing on its merchandise trade account. The previous financial year, 2025-26, ended with India’s merchandise trade deficit at a historically record level of $333 billion, an increase of over 17% as compared to the preceding year. The increase in trade deficit was caused by imports expanding by 7% to scale the highest ever level of $775 billion, while exports increased by less than a percentage point to reach $441 billion.

The US-Iran war and the disruption caused to the oil supplies due to the subsequent closure of the Strait of Hormuz has adversely affected India’s crude oil imports. In March 2026, imports fell by over 41% in quantity terms, on a year-on-year basis, and by 35% in terms of value. Thus, the crude oil import bill did not reflect its higher prices in the international market, which, according to IMF’s crude oil price index, rose by 53% since the war began. This was largely because India’s imports from its second and the third largest suppliers, Saudi Arabia, and Iraq, respectively, fell by 63% and 61% in that order. Quantities of natural gas imported were also affected, though not as adversely as crude oil, which also meant that the 40-50% increase in natural gas prices since the beginning of the conflict in West Asia are also not reflected in the import figures. Most commentators have warned that crude oil and natural gas prices tend to be sticky, in other words, they are not likely to come down, even if peace returns to West Asia. This indicates that India could be saddled with a higher crude oil/natural gas import bill and an inflated merchandise trade deficit at least until the end of the 2026-27 fiscal year.

The probability of gold imports declining seems low as sustained stock market volatility has pushed retail investors towards diversifying their portfolios, opting for both physical and Exchange Traded Fund gold.

India’s imports in 2025-26 were driven by four product groups having sizeable shares, namely, gold (and silver), edible oils, fertilisers, and electronic components. Imports of precious metals, valued at over $90 billion, accounted for about 12% of the import bill, and were the third largest product group in the import basket after crude oil and electronics items. Gold imports increased by 24%, and silver, by a staggering 150%. Exports of gems and jewellery, on the other hand, declined by over 5%, indicating that increased imports of the precious metals were mostly absorbed domestically.

The unprecedented increase in gold imports has continued unabated in the financial year 2026-27, increasing by 82% in April 2026 as compared to a year before. Given this surge, the government followed up the prime minister’s urging to the citizens to postpone non-essential gold purchases, by increasing customs duty on gold and silver imports to 15%. The question is, would higher import duties reduce imports of precious metals? The probability of gold imports declining seems low as sustained stock market volatility has pushed retail investors towards diversifying their portfolios, opting for both physical and ETF (Exchange Traded Fund) gold. In fact, there are expectations that higher import duty on physical gold will increase the shift towards ETF gold.

India’s dependence on imported edible oils because of inadequate oil seed production has been the outcome of a worrisome aspect of the country’s agricultural performance. The increase in edible oil imports exceeded 12% in 2025-26, which followed a 17% increase in imports in 2024-25. April 2026 saw an even higher year-on-year rise in imports, by 40%. Almost 56% of India’s edible oil demand was met through imports in 2023-24, the most recent year for which official data are available. The recent surge in imports is a pointer that import dependence in this critical commodity has worsened. Since the government has failed to find a way of increasing domestic production of oil seeds, it needs the citizens to decrease their consumption of edible oil to reduce imports, and to thus save foreign currency.

Spiralling prices of fertilisers in the international market are not only causing the country to lose foreign currency due to its high import dependence, but the fertiliser subsidy bill could also significantly increase. In global markets, fertiliser prices increased by 46% between December 2025 and April 2026, while the price of the most popular fertiliser in India, urea, more than doubled in this period. Over the past five years, imports have met between 31% and 37% of the country’s fertiliser needs but this was expected to have been over 50% in 2025-26, as imports of urea increased by over 60%. The disruption due to the war in West Asia has increased India’s fertiliser import bill by nearly 80%. In 2023, the Prime Minister's Programme for Restoration, Awareness Building, Nourishment, and Amelioration of Mother Earth (PM-PRANAM) was introduced to promote adoption of biofertilizers and natural alternatives in addition to chemical fertilizers. Current assessments show that the market for biofertilizers in India is approximately $150 million, which is dwarfed by the $40-50 billion market for chemical fertilisers. A coherent strategy is, thus, needed to insulate the domestic market for fertilisers from supply shocks and to reduce uncertainties for the farmers, through rapid expansion of domestic production of all forms of nutrients.

In global markets, fertiliser prices increased by 46% between December 2025 and April 2026, while the price of the most popular fertiliser in India, urea, more than doubled in this period.

Though the prime minister advised the citizens to “prioritise Made in India products,” the Atmanirbhar Bharat Abhiyan launched in 2020 to reduce the country’s import dependence on China has not made much headway in several key industries. Therefore, six years after the launch of the Production Linked Incentive (PLI) Scheme and huge budgetary outlays to increase domestic production, several target industries remain significantly dependent on imports. This includes electronic components, imports of which grew by over 20% in the previous fiscal year. Domestic production of accumulators and batteries were also to be stepped up to reduce the import content of electric vehicles, but in 2025-26, imports of these products increased by 50%. India’s transition towards greater technological sophistication is thus burdened with the cost of considerable foreign currency outgo.

1.1 The FTAs Conundrum

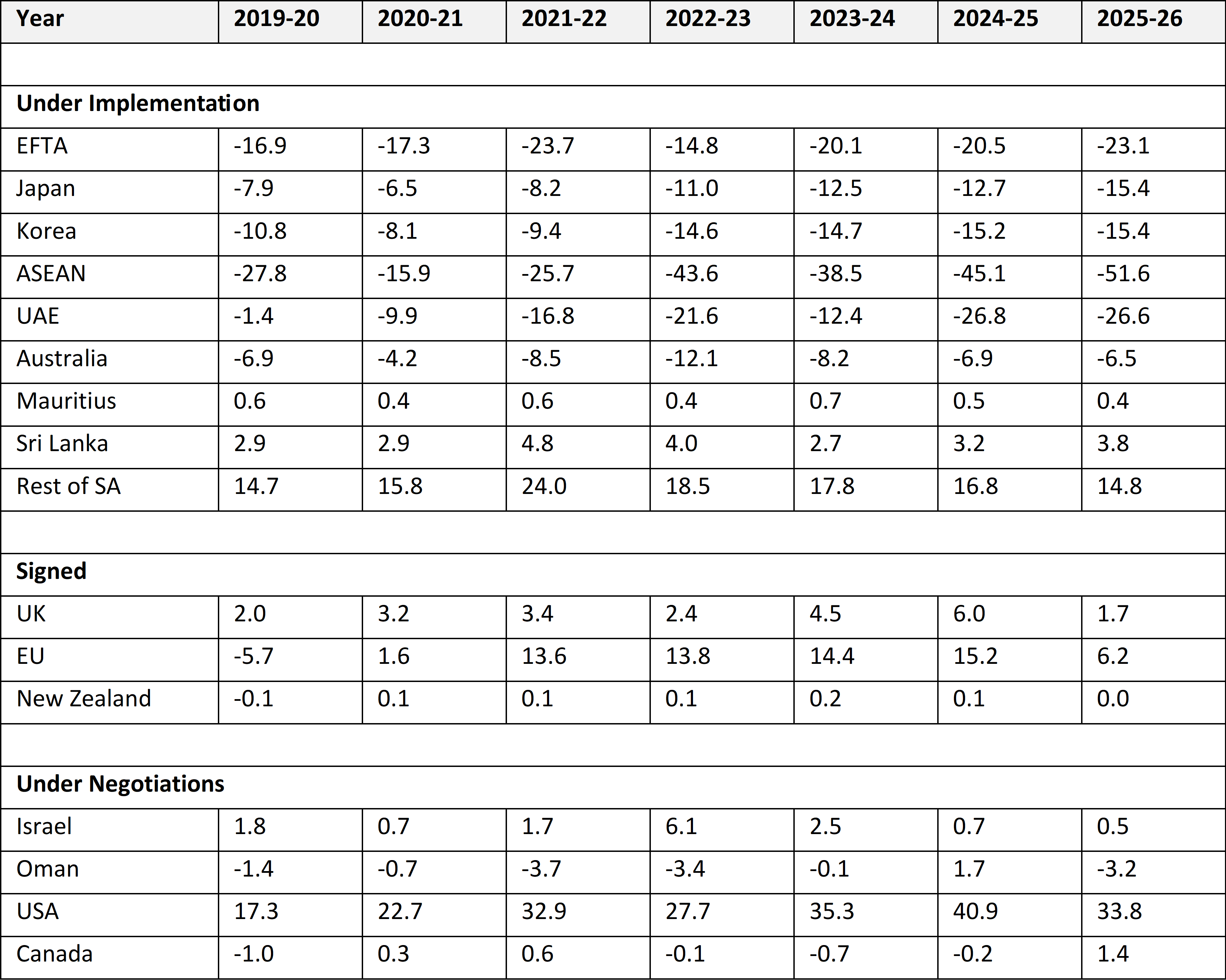

When the prime minister is urging that the foreign exchange outgo on the merchandise trade account should be reduced, the government needs to take a serious look at the problems associated with the implementation of free trade agreements (FTAs) with major trade partners. These FTAs have one common feature: all of them have seen mounting trade deficits (Annex Table 1), including those signed earlier in the decade.

Another noteworthy feature is that until 2024-25, India enjoyed substantial trade surpluses with two of its largest trade partners, the US, and the EU. But as the two-decade old India-EU FTA negotiations were finally concluded in January 2026, and progress was being made in the US-India FTA negotiations, India’s trade surpluses with both partners reduced significantly. With India offering significant market access to the EU and Donald Trump intent on extracting the maximum benefits from India in the on-going FTA negotiations, the trade surpluses with these partners could quickly shrink.

Widening trade deficits with FTA partners has been entirely on account of sluggish export growth. FTAs have increased imports, as expected, following India’s steep reduction or removal of tariffs. Though India signed these FTAs with the expectation that its businesses would be able to substantially increase their exports to partners’ markets, this expectation has remained largely unmet. Export growth has been low due to inadequate preparedness of Indian businesses, and this is also a reason why Indian products have remained uncompetitive in the international market. India’s policy makers have failed to recognise that gains from FTAs cannot be ensured merely through market opening. A simultaneous implementation of robust domestic policies, including industrial and agricultural policies, designed to enhance the competitiveness of domestic enterprises, is imperative for securing benefits from these agreements and to reduce the drain on foreign currency resources. It is imperative for the government to review the failings of the past FTAs before committing to further expand its FTA-engagement.

2. Uncertainties Gripping the Capital Account

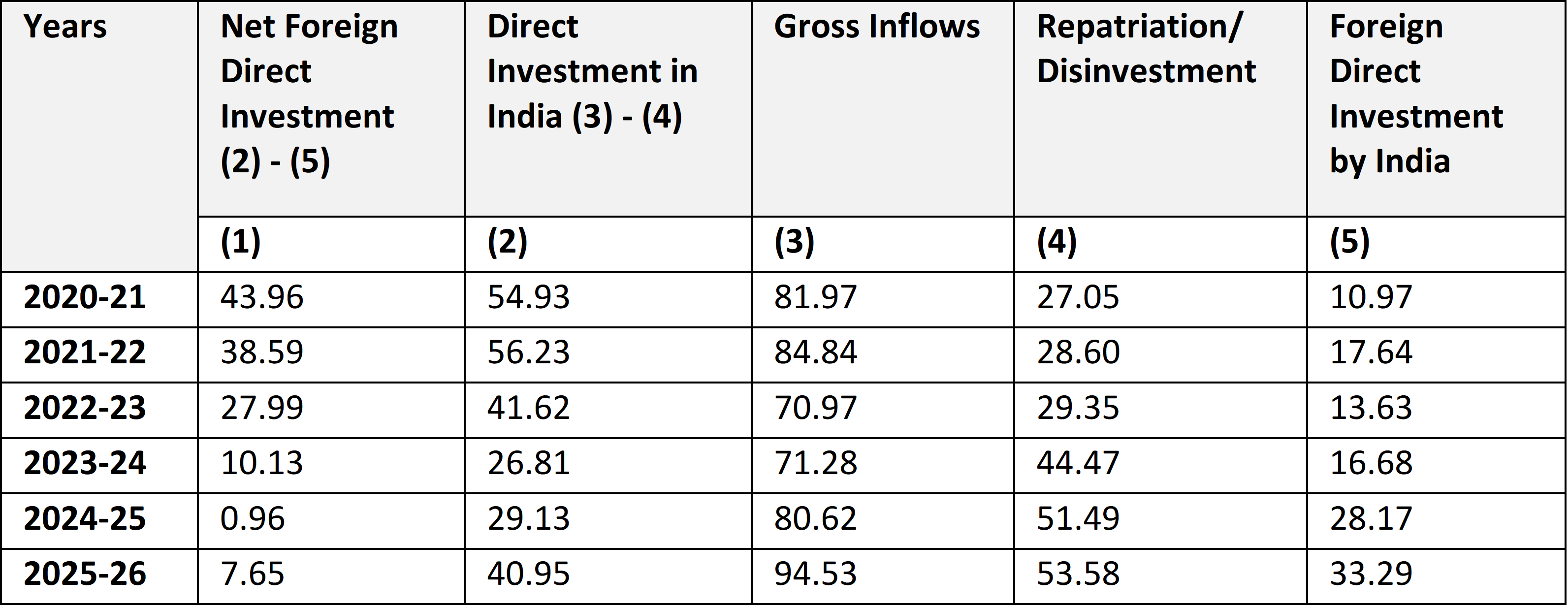

The headline in this regard is that India’s net FDI inflow 1Net FDI inflows is the difference between direct investment in India, or gross inflows less divestment, and foreign direct investment from India. dipped to an alarming level of less than a billion US dollars in 2024-25. Though this figure was $7.7 billion in the previous fiscal year, it was still well below the peak of $44 billion in 2020-21. In fact, the decline in net FDI inflows has been a feature of the post-pandemic years (Annex Table 1).

The government tacitly accepted that this squeeze on FDI inflows was a source of concern by announcing a major shift in its FDI policy in March. The nodal ministry, the Department for Promotion of Industry and Internal Trade (DPIIT), made a key amendment to Press Note 3 (PN3) issued on 17th April 2020, which increased regulations on foreign direct investors from countries with which India shares land borders 2Before PN3 was issued, a citizen of Pakistan or Bangladesh, or an entity incorporated in these countries, could invest in India only under the Government route, in other words, automatic approvals were denied. In addition, a citizen of Pakistan or an entity incorporated in Pakistan could invest in sectors other than defence, space, atomic energy, and in sectors generally prohibited for foreign investors. PN3 extended this restriction to countries with which India shared land borders or where a “beneficial owner” of an investment in India was located in or was a citizen of these countries (emphasis added). This new condition was clearly targeted at investors from China, which followed worsening of bilateral relations after the border clashes in Ladakh. .

The latest amendments to FDI policy improved the conditions for potential investors from countries with which India shares its land border, in two ways. One, investors from these countries with non-controlling “Beneficial Ownership” of up to 10% are allowed to invest under the automatic route, subject to the applicable sectoral caps, entry routes, and attendant conditions. And, two, processing of proposals for investments in specified sectors/activities of manufacturing in capital goods, electronic capital goods, electronic components, polysilicon and ingot-wafer, would be completed expeditiously, within 60 days. The indicative sectors are a subtle hint that the government is extending an olive branch to the Chinese investors, which is in keeping with the improvements in bilateral relations over the past several months. The government’s expectation is possibly that the new guidelines would provide clarity to the investors from the country’s northern neighbour and facilitate an inflow of investments, thus contributing towards greater, access to new technologies, domestic value addition, expansion of domestic firms and integration with global supply chains. Our view is that the new guidelines are in response to the weakening of net FDI inflows into India.

…[D]uring the past decade, disinvestments by foreign direct investors increased nearly five-fold, while the gross inflows grew less than two-fold.

As mentioned earlier, net FDI inflows dropped to a precipitous level of less than a billion US dollars in 2024-25. Net inflows slumped despite annual gross inflows of $81 billion in 2024-25, followed by $94 billion in 2025-26, due to significant outflows on two fronts. First, disinvestments by foreign investors reached record levels of disinvestments, and, secondly, India’s overseas FDI also touched an all-time high. (FDI inflows were $21 billion in the first three months of 2026, or Q4 of 2025-26. Compared to the three previous quarters of FY26, this was the lowest.)

Disinvestments by foreign direct investors reached a record level of $51.5 billion in 2024-25, increasing from $18 billion in 2019-20. In fact, during the past decade, disinvestments by foreign direct investors increased nearly five-fold, while the gross inflows grew less than two-fold. Disinvestments were between 64% and 57% of gross FDI inflows in 2024-25 and 2025-26 respectively, well above the 25% levels seen in the previous decade. FDI is considered as stable and long-term investments and for it to become foot-loose is something that policy makers should be concerned about. However, Chief Economic Adviser (CEA), V Anantha Nageswaran, while admitting that “net FDI has been weaker”, “driven substantially by higher repatriation of profits”. It is quite baffling to see the chief economist of the government blaming higher profit repatriation, a current account transaction on the balance of payments account, for the weakness in net FDI inflow, a capital account transaction. However, we must compliment the CEA for highlighting the substantial foreign currency drain that FDI is inflicting on the current account through two channels, profit repatriation and outflow on account on payments for intellectual property.

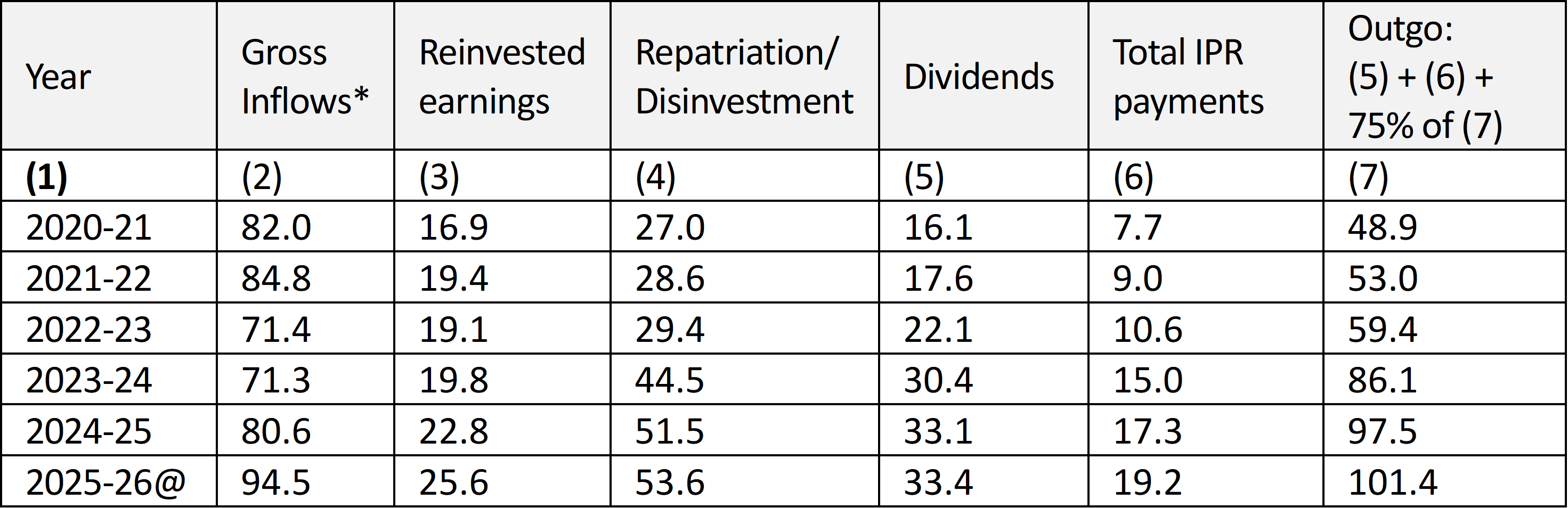

Annex Table 3 provides details on the foreign currency outgo on account due of FDI. The total outgo, which includes net repatriation of profits (after reinvestment in India), disinvestment, and charges for the use of intellectual property, was more than twice as large in 2025-26 as in 2020-21. The net outgo has been higher than the gross FDI inflows since 2023-24, peaking at over $17 billion in 2024-25, and reducing subsequently to $7 billion, on account of higher gross inflows. Thus, foreign direct investors’ financial participation in India mirrored the colonial pattern: outgo of financial resources from the host countries was larger than the inflows.

As in the case of disinvestment by foreign investors, India’s outward foreign direct investments (OFDI) increased dramatically from the beginning of the 2020s. From about $11 billion in 2020-21, OFDI grew to over $33 billion in 2024-25. This sudden spurt in OFDI from India is not only surprising, but it is also counter intuitive. When the Indian economy is the fastest growing among the major economies, we would expect domestic investors to have been looking at investment opportunities at home, instead they are investing in other countries.

What is more, India’s private sector has been generating record profits since the pandemic. Between 2020 and 2025, profits of India Inc. grew three times faster than the country’s GDP. The comfortable balance sheet position of India Inc should also have given them the advantage of raising funds. A paradoxical situation has thus emerged wherein Indian investors are moving capital out of the country while the government is wooing investors from its FTA partners by offering significant concessions in bilateral trade agreements, including larger market access, which fules the import bill. For instance, in the FTA with the four-member European Free Trade Area (EFTA), the government justified its decision to reduce/remove tariffs on 95.3% of industrial goods arguing that EFTA members would invest $100 billion in India within a decade. More recently, while endorsing the FTA with New Zealand, the Indian government spoke of the latter’s commitment to invest $20 billion in India over the next 15 years.

When the Indian economy is the fastest growing among the major economies, we would expect domestic investors to have been looking at investment opportunities at home, instead they are investing in other countries.

These expectations of FDI inflows seem too optimistic for a number of reasons. In the past quarter of a century, the EFTA members, Switzerland, Norway, Lichenstein, and Iceland, had invested just a little more than $12 billion in India. Given this, an investment of $100 billion by these countries during the next decade seems improbable. In comparison, the pharmaceutical giant Novartis AG, sold its entire 70.68% controlling stake in Novartis India Limited, Switzerland’s the most recognisable commercial face in India, to a consortium of three investment firms for approximately $345 million. Expectations of $20 billion investments from New Zealand over 15 years also seem overstated. New Zealand’s outward investments to all countries during 2000-24 was less than $7 billion, and in the post Covid years, it had divested its foreign stakes by $1.6 billion.

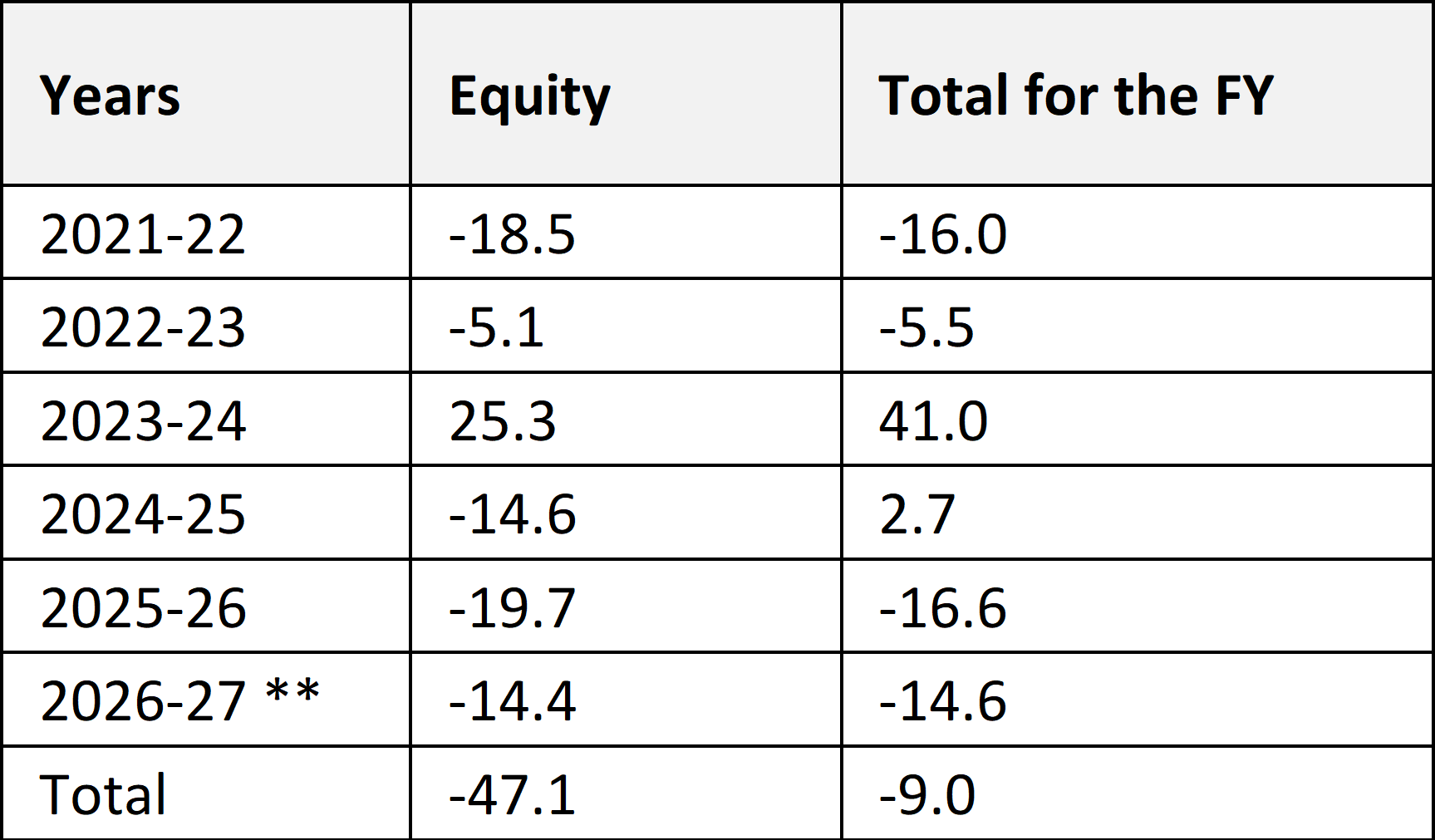

Any discussion on the developments in India’s capital account would be incomplete without referring to the behaviour of foreign portfolio investors (Annex Table 4). In the immediate post-pandemic phase, behaviour of portfolio investors was inconsistent, as they remained invested in India only in 2023-24. However, since the previous fiscal year, they turned sharply bearish, withdrawing a record high of $16.6 billion. In the first two months of the current fiscal year, portfolio investors’ behaviour has been worse, they withdrew $14.6 billion (up to 5 June). This volatility has added significantly to the uncertainties that the Indian economy faces at this juncture.

3. Warnings for the Macroeconomy

The Indian economy faces vulnerabilities caused by foreign exchange outgo both on the current and the capital accounts of the balance of payments. The government has already acknowledged the strain on the economy faces caused by the import surge, which prompted the prime minister to urge the citizens to reduce spending on several products that entail substantial foreign exchange outgo. The capital account also faces an exceptional situation as outflows on account of both direct and portfolio investments have caused considerable consternation among policy circles. In the first week of June, the government announced several measures including expanding the Fully Accessible Route (FAR) for government securities, removing limits pertaining to short-term investment, and increasing the limits for investment by NRIs and OCIs in equity instruments traded on the stock market without SEBI registration. Further, the RBI decided to provide facility of a concessional forex swap until 30 September 30 to incentivize ECBs by PSUs and Authorized Dealer Category 1 banks.

These measures, besides encouraging foreign investment inflows, are also aimed at stemming from the depreciation of the to unacceptably low levels, and to reduce the vulnerability of the economy. Over the past several months, the RBI has been selectively intervening to prevent a free-fall of the currency using the foreign exchange reserves. Between end-February and end-May 2026, India’s foreign exchange reserves fell $46.2 billion and foreign currency reserves fell by over $27 billion. Even if the rupee continues to slide, RBI will need to carefully calibrate its market interventions since further decline may not be prudent.

Keeping the value of the rupee relatively stable is imperative for several reasons. The first is to prevent the import bill from rising, which would, in turn, increase the current account deficit. Secondly, rupee depreciation would escalate inflationary pressures already being felt due to rising fuel and fertiliser prices. According to the RBI, CPI inflation for 2026-27 is expected to be at 5.1%, up from 3.6% in April 2026. And finally, stability of the rupee is vital for realising the government’s target of increased use of the domestic currency for trade transactions and reducing the reliance on US dollar. Alongside these short-term measures, the government needs to work towards medium-term solutions aimed at increasing the ability of domestic businesses to increase their exports, while at the same time reducing import dependence by making agricultural and industrial policies deliver concrete results.