The coronavirus outbreak, its spread to India and the sweeping shutdown the Government of India has put in place will have—indeed have already had—a serious impact on the Indian economy. The ripples of the global impact will make this worse. With the global impact of the coronavirus, it is now certain that the global economy will be pushed into a recessionary phase.

In such a context Union Budget 2020-21, which was presented as recently as on 1 February, has already lost much of its value. Moreover, the impact of the outbreak may call for a major fiscal stimulus of the kind many advanced country governments have implemented. Unfortunately, even in early February, well before the coronavirus impact had been felt, the budget numbers had little validity and the macroeconomic approach was one of fiscal fundamentalism.

In this context, this article argues that a budget prepared on the basis of a doctrine of fiscal fundamentalism will not able to bring the economy out of a downswing. Therefore, our argument for a fiscal stimulus, as outlined below, is going to be stronger in the future.

1. Introduction

The Union Budget is a routine annual income and expenditure statement of the government. In India, however, it turns out to be like a big fat Indian wedding, full of pomp and grandeur. The printing of the budget is preceded by the Union Finance Minister giving finishing touches to the customary halwa preparation for staffers. The subsequent lockdown of the ministry during the printing, to prevent any leaks, adds to the mystery. The media attention boosts the popularity of the budget presentation. This year was no exception.

Given the lacklustre growth of the India economy, one had expected a big-bang budget which would give some push to the economy, taking it out of the current slow growth path. This became all the more relevant after a monetary stimulus of a cumulative 135 basis points cut in the policy repo rate in recent months. The Reserve Bank of India Governor emphasised the need to have greater clarity on the kind and nature of countercyclical fiscal measures that could be pursued. 1 Edited Transcript of Reserve Bank of India’s Fifth Bi-Monthly Monetary Policy Press Conference on December 5, 2020.

There was widespread expectation that the government would use fiscal policy in the budget to boost demand in the economy. But the government has not recognised demand contraction as the reason behind the slowdown. Instead the Union Budget 2020-21 tried to focus on supply-side issues and attempted to fix the financial markets with some tinkering. 2 “Financial Sector in the Budget: Skating on Thin Ice?”, Partha Ray and Parthapratim Pal, Economic and Political Weekly, February 29, 2020, Vol LV, no 9. The government has missed a chance of pursuing an expansionary fiscal policy at this crucial juncture. The thinking behind the Union Budget 2020-21 has not been Keynesian in spirit.

Moreover, a more careful look at the resource mobilisation numbers indicates that the government may not be able to mobilise the resources it expects for 2020-21.

In the following, we choose to go beyond an analysis of the usual allocation decisions of the budget. We seek macroeconomic clarity on whether there is a counter-cyclical fiscal policy in the budget for a slowing economy. We also look at the credibility of the fiscal numbers. We argue that the budget lacks a long-term vision for reviving the economy.

Overoptimistic projections and unforeseen economic shocks like the spread of the coronavirus will show eventually in revenue and capital receipts in 2020-21 that are way off the mark. It is almost certain that there will be a major reduction in government expenditures, further dampening demand. The government should realise that demand generation through fiscal policies should be the main bulwark against a slowdown, and a dependence on interest rate cuts alone to revive the economy is unlikely to work.

2. Macroeconomic Context of the Budget

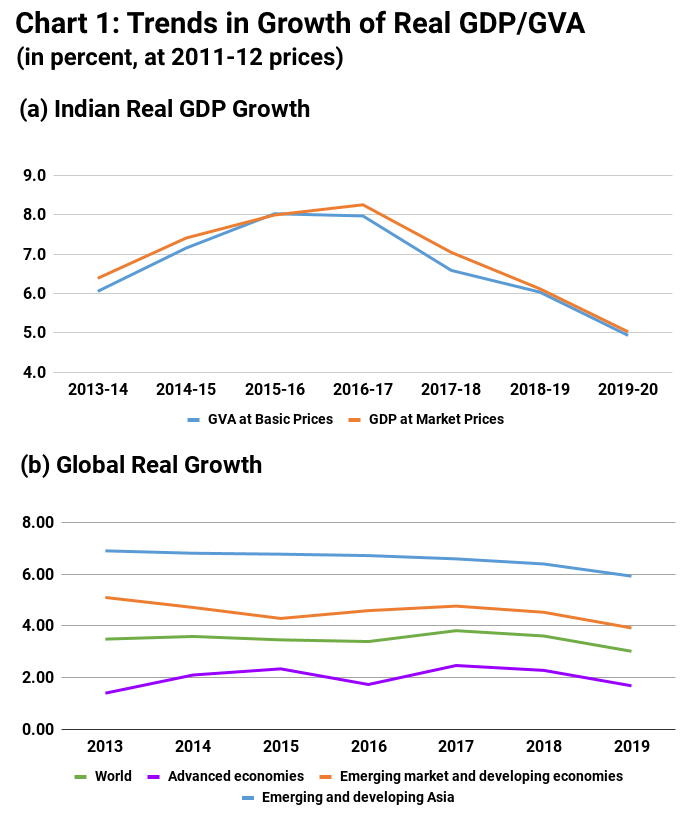

There has been a sharp deceleration in India’s GDP growth since 2016-17. The high growth rate of 8 % in 2016-17 has steadily come down to 5 % in 2019-20 (Chart 1, Panel (a)). While there has been a downward trend in global growth in advanced as well as emerging and developing economies, the trend has been very sharp in India (Chart 1, Panel (b)). Thus, to ascribe the whole slowdown to a global trend is misleading.

(b) World Economic Outlook Database, IMF, October 2019

The slowdown has been quite widespread. All major components of aggregate demand registered lower growth during 2019-20. The situation is particularly gloomy with respect to gross domestic capital formation, a key measure of investment, whose growth has contracted 0.6 % in 2019-20 compared with a growth of 9.8 % in 2018-19. Exports and imports have shrunk as well.

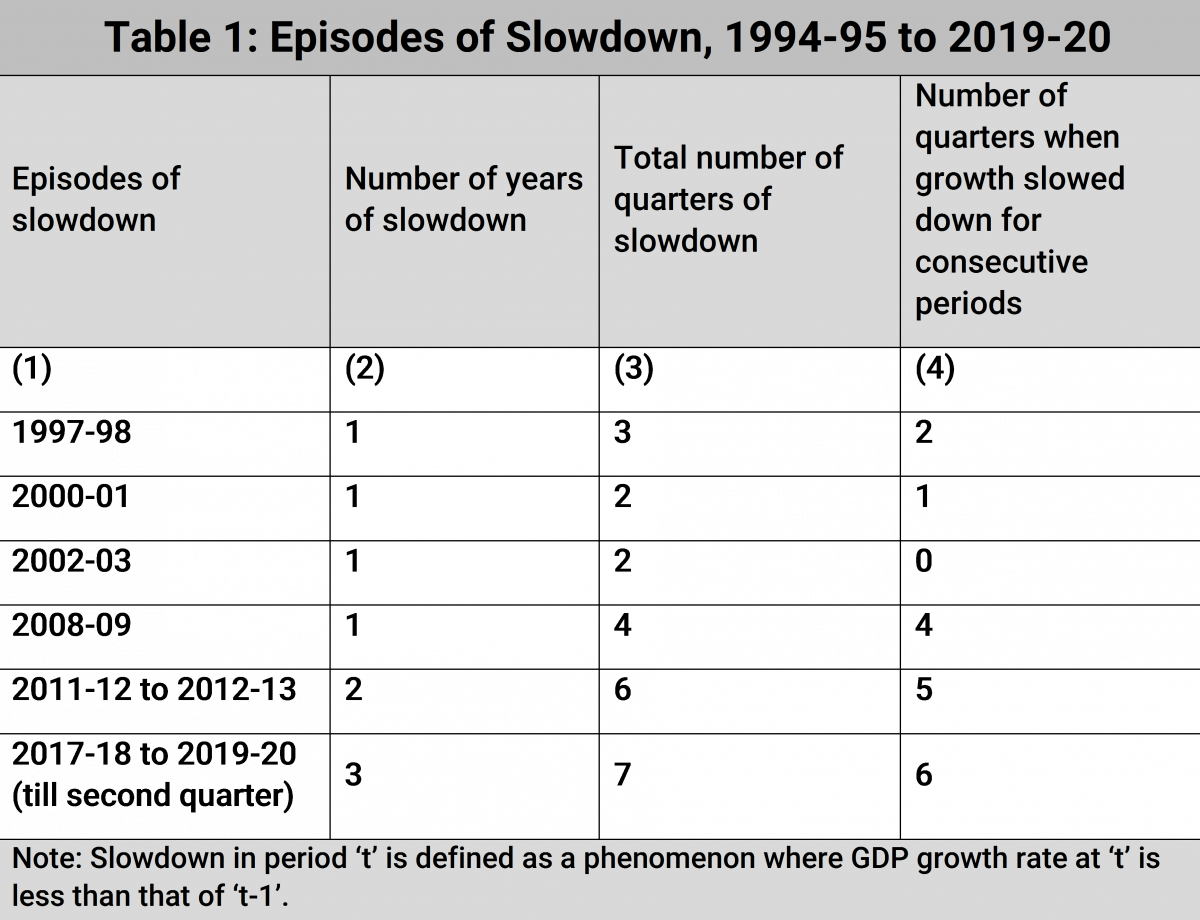

More importantly, the slowdown has been quite severe and prolonged. Examining the period 1994-95 through 2019-20, Dasgupta (2020) arrives at a startling conclusion: “Both in terms of annual and quarterly GDP growth rates, the present slowdown has been more prolonged than any other previous episodes of slowdown during the liberalization period” (Table 1).

Economic and Political Weekly. (forthcoming)

Thus, by all accounts the current slowdown has been prolonged, widespread and continuous. But what has been the diagnosis of this slowdown? Reading the Government of India’s Economic Survey 2019-20, released a day before the presentation of the budget, gives one an insight into the Government’s version of the root cause of the slowdown. If the Economic Survey’s diagnosis is to be believed, the root cause of the slowdown is fundamentally financial in nature. The principal villains are the slow offtake in credit disbursement following the accumulation of non-performing loans of the banking sector, and the lull in liquidity in the non-banking financial companies since the IL&FS crisis of September 2018. If this diagnosis were true, the responsibility for tackling the slowdown would lie primarily with monetary policy. Fiscal policy then should follow a minimalist path. Its sole objective would be to follow a path of fiscal rectitude so as to control the fiscal deficit indicators.

3. Some Unpleasant Fiscal Arithmetic

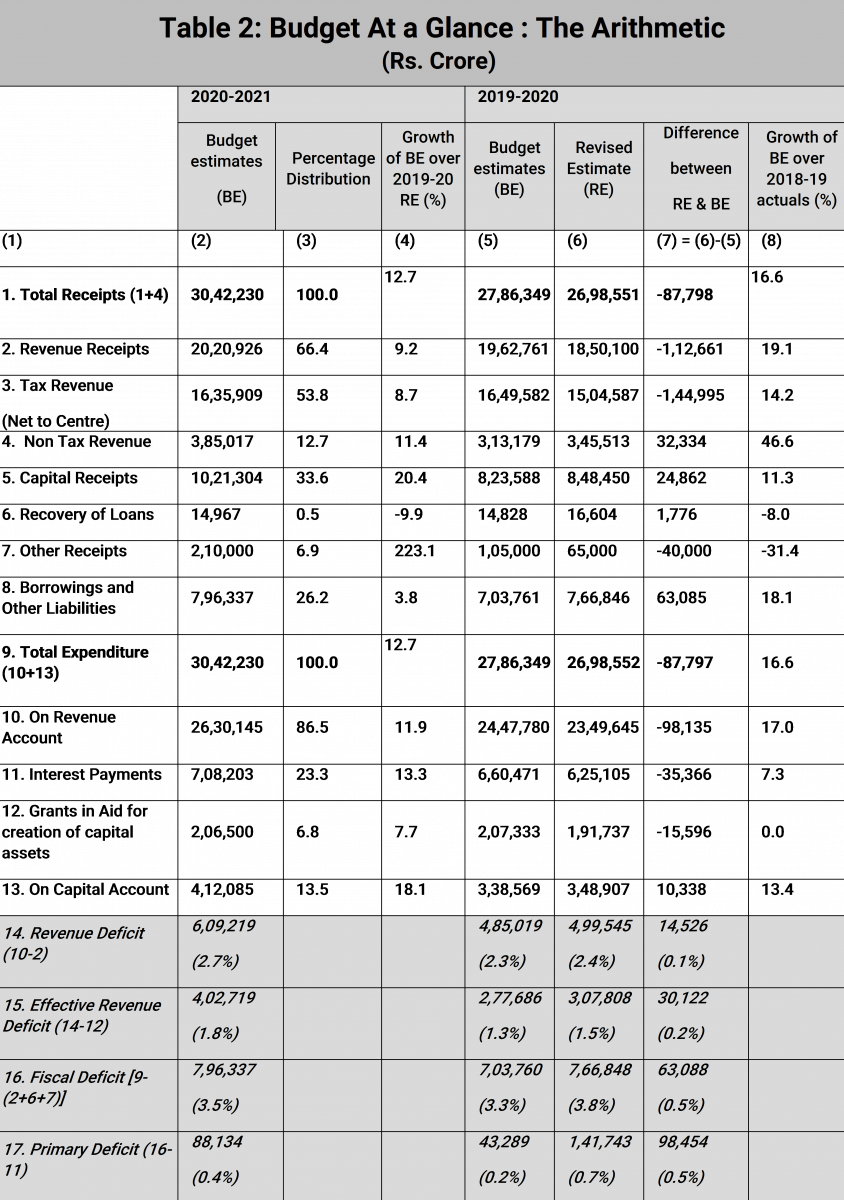

Stripped of all the hype and hoopla, the budget is an income-expenditure statement of the Central Government. In order to understand this aspect of the budget, Table 2 presents the numbers reported in the Budget at a Glance statement of the Finance Minister, in which column (3) and (6) are derived by us.

A few broad features of the budgetary arithmetic may be highlighted.

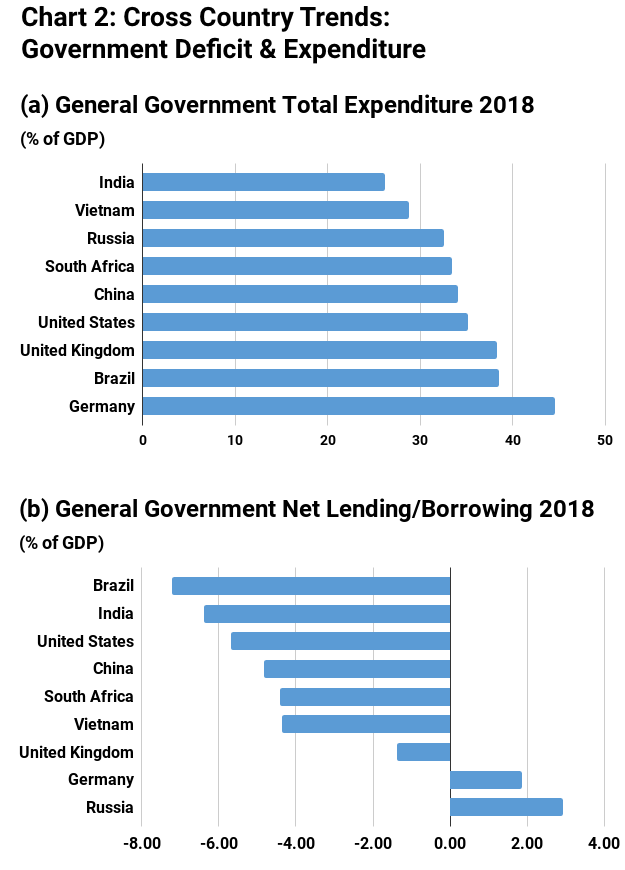

First, despite the huge media attention, the size of the budget at Rs. 27 trillion in 2019-20 is only around 13 % of India’s GDP. In other words, the size of the government in India is not very large. Even if we add the expenditure of all the state governments, as the IMF does, the total government expenditure as a percentage of GDP in India is lower than all the BRICS countries as well as the leading G7 economies (Chart 2a). However, in terms of general government (i.e., centre plus states) net borrowing, India is next to Brazil (Chart 2b). Taken together, it is not that the Indian government spends a lot, but its revenue is paltry. It is no wonder then that India has only 7 tax payers for every 1000 voters, one of the lowest in the world (Economic Survey, 2016-17). Thus, an ultra-conservatism in the form of fiscal minimalism is perhaps misplaced.

Second, despite such a meagre size of government expenditure, why are there then such expectations from the budget? The answer to this question can be sought in basic Keynesian macroeconomics. Any increase in government expenditure has a multiplier effect on the economy. Thus, depending on the value of the multiplier, even a small increase in government expenditure may have a large effect on the final effective demand, which can do wonders in a slowing economy.

What is the value of the multiplier in India then? While official values of multipliers are unavailable, there is near unanimity among researchers that the multiplier for capital expenditure is far higher than for transfer of income. 3 A working paper from NIPFP found the following values of multiplier: 2.45 for capital expenditure; 0.98 for transfer payments; and 0.99 for other revenue expenditure. See Sukanya Bose & N R Bhanumurthy (2013): 'Fiscal Multipliers for India', NIPFP Working Paper 2013-125, for details. Thus, despite the small size, the key to the effectiveness of the Union Budget will lie in the extent of capital expenditure. It is here that Budget 2020-21 fails to do justice in a slowing economy. Out of total expenditure only 13.5 % has been allocated towards capital expenditure. Even if one adds the revenue expenditure on account of Grants-in-Aid for creation of capital assets, it just touches 20 %.

It is perhaps in this spirit that Shankar Acharya, a former Chief Economic Adviser, commented that the government’s investment-based strategy to boost growth is more like what you expect in a normal year rather than as a response to a crisis. 4 'Budget 2020 Not What Economy Needs, Centre Seems in Denial’: Shankar Acharya, interview in The Wire However, it needs to be noted that while the multiplier in capital expenditure is high because of the long gestation times, the effect will be stretched out. But in the case of revenue expenditure its impact could be immediate.

4. How Credible are the Budget Numbers?

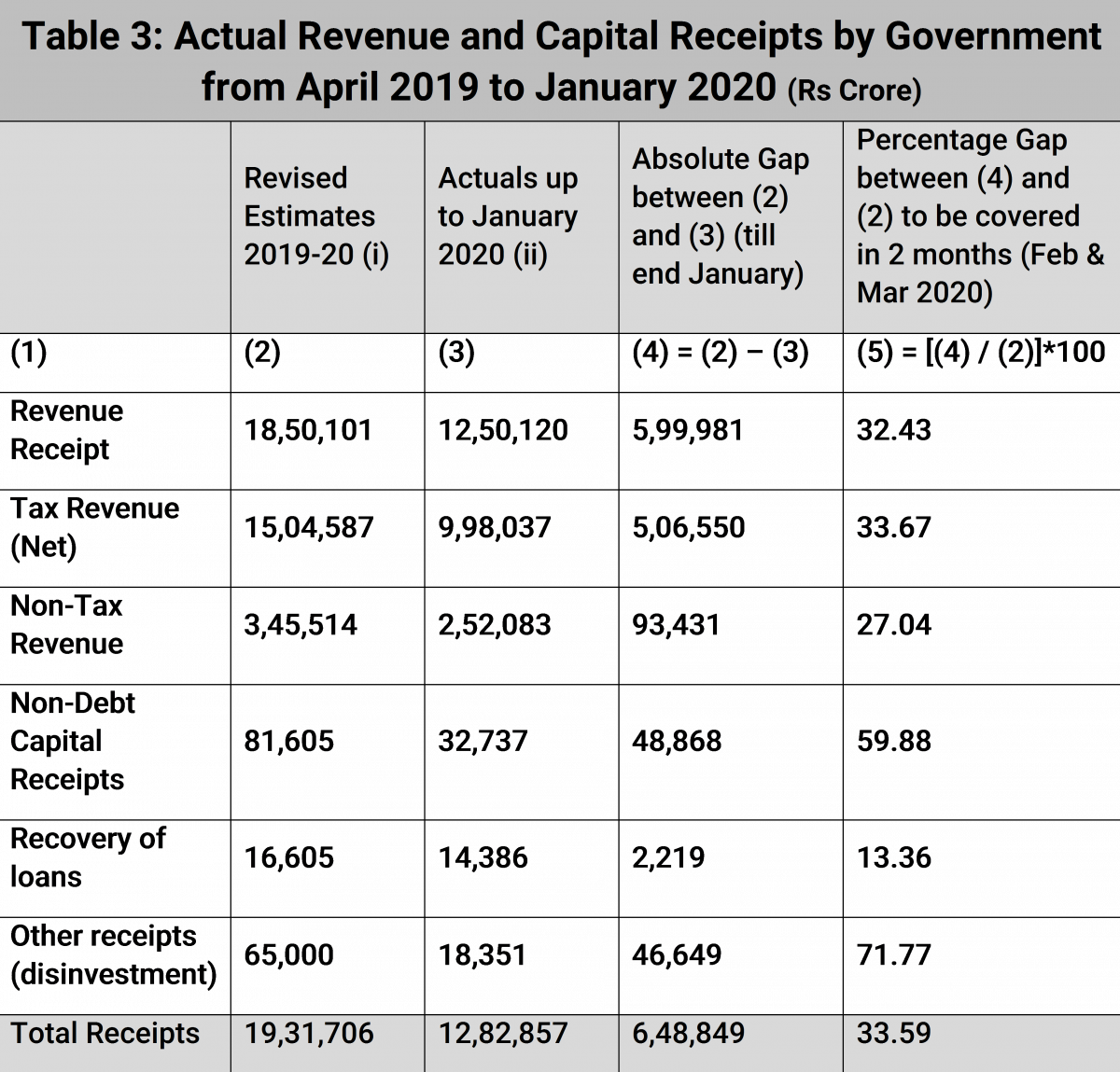

In terms of fiscal marksmanship, Budget 2020-21 has done a poor job. It is surprising that in 2019-20, a year of a slowdown, the budget showed that India’s Revised Estimates (RE) of revenue expenditure was nearly Rs one lakh crore less than the Budget Estimates (BE). This has hardly been compensated by an additional capital expenditure of around Rs 10, 000 crore. The phenomenon of reduced spending during a substantial slowdown is surprising. On the revenue side, the difference between the RE and the BE is more glaring. The Centre’s net tax revenue in 2019-20 undershot the revised estimates by Rs one lakh crore rupees, reflecting low GST collection. In fact, despite a huge windfall from additional RBI dividends, total revenue in 2019-20 RE is less than the BE for the year by nearly Rs. 88, 000 crore. Among capital receipts, other receipts—primarily reflecting disinvestment proceeds of the government—are likely to fetch Rs. 40,000 crore less than in the BE. 5 But as we will discuss below, the actual resource mobilization through disinvestment is even less.

The spread of the coronavirus and its economic fallout across the world will change some of the projections quite drastically. This will affect both inflation and real GDP growth. The economic shock arising out of the spread of the coronavirus has led to a decline in oil prices. On 9 March 2020, the Brent Crude futures were trading at US $35–37 per barrel down more than 20 % over a few days. If low oil prices persist then it will have a dampening impact on inflation rates in India. On the other hand, there will be a negative impact on the real growth rate. If both inflation and the real growth rate come down, then the 10 % nominal rate of growth assumed in Budget 2020-21 will not be achieved.

We now take a more careful look at the figures presented in the budget and compare them with the actual resource mobilisation achieved by the government in 2019-20. We start with the numbers published in the Budget at a Glance. 6 Monthly trend of the actual revenue/expenditure numbers are available from the website of Controller General of Accounts. We use these in conjunction with the budget numbers available from the www.indiabudget.gov.in website.

Receipt Accounts

In the budget calculations for 2020-21, the government has assumed a growth of 11.43 % in gross tax revenue and 12 % in non-tax revenue. The underlying assumption here is a 10 % nominal growth rate of GDP. Given the continuing slowdown of the economy, achieving these revenue targets will not be easy. It is to be noted that the increase in gross tax revenue in the 2019-20 RE over the actual figures of 2018-19 is only 3.99 %. For non-tax revenue, the estimates are mostly coming from a staggering 64 % projected growth rate in the ‘other non-tax revenue’ head. 7 According to the estimates for 2020-21 it is projected that ‘Other non-tax revenue’ will increase from Rs 131,525 crores in revised estimates for 2019-20 to Rs 215, 465 crores in 2020-21. (Source: Budget at a Glance Table 5) It is to be noted here that the government has clarified that it has not taken into account the dues of Rs 1.47 lakh crore cumulatively owed by several telecom firms. Even if some fraction of these dues is recovered, it can boost the revenue figures significantly. 8 'Govt not included AGR dues payment in Budget 2020-21: DEA Secy', The Economic Times, February 4, 2020

However, the biggest jump in Budget 2020-21 is assumed in capital receipts. The budget projected a 175 % increase in non-debt capital receipts in 2020-21 over the 2019-20 RE. An even bigger increase is estimated in disinvestment receipts. The government expects to raise Rs 2.1 lakh crore from disinvestments, more than twice the money it had expected to raise in 2019-20. 9 In the past few years, the amount of disinvestment the government has achieved is not always pure disinvestment. In certain instances, the government has sold stakes in one PSU to another PSU to shore up the disinvestment numbers. For example, ONGC acquired stake in HPCL and this is shown as disinvestment. This is much more than what the government has ever managed to achieve through disinvestment in a single year since 2010-11. Most of this depends on the proposed dilution of holdings in the Life Insurance Corporation (LIC) of India and IDBI Bank.

To assess how realistic these revenue and capital receipt projections are, it is important to look at the actual figures the government has achieved for 2019-20, data for which is available until January 2020. 10 This point has been raised by some critics. See ‘Smokescreen of Numbers’ by Jayati Ghosh and ‘You cannot take the numbers seriously’: TN Ninan on Nirmala Sitharaman’s Budget 2020. It is important to point out here that as the budget was tabled on 1 February 2020, the budget estimates of 2019-20 are based on actual data which, at the time of the tabling the budget, were available only till December 2019. Now actual data till January 2020 are available from the Controller General of Accounts. A look at this data shows some interesting trends, reported in Table 3.

There is a considerable gap between the actual receipts and the 2019-20 RE for both revenue and capital receipts. For example, the government had collected Rs 998, 037 crore in tax revenue till January 2020, one-third short of its full-year target. It will have to collect an additional Rs. 506, 550 crore in the two months of February and March, a sum more than half of what was collected during the 10-month period of April 2019 to January 2020.

Similarly, the last column of Table 3 shows the percentage shortfalls in other categories.

It can be argued that revenue collections possibly increase during the end of the fiscal year and, therefore, it may be possible that the government will be able to achieve the target for the entire year. Looking at the monthly tax revenue data, we find there is a cyclical pattern. Tax collections do go up sharply during the last month of the fiscal year.

Given this monthly pattern of tax collection, we probed a bit deeper to understand how the resource mobilisation of the government has fared in 2019-20 as compared with other years. We looked at the data of the past 5 fiscal years: 2015-16 to 2019-20. For this period, we looked at the ratio of actual receipts to revised estimates up to the month of January for each of the years.

We find that revenue receipts till January as a percentage of revised estimates were the lowest for 2019-20 as compared with any of the other years. The same is true for total receipts. In the other parameters also, 2019-20 turns out to be one of the worst performers in resource mobilisation. These numbers indicate that it will be difficult for the government to meet the 2019-20 revenue targets even if there are sharp increases in revenue collections in the last two months.

Even more difficult will be to meet the lofty disinvestment targets. Given the economic impact of Covid-19, the present economic scenario, and the current state of the stock market in India with prices on a volatile and downard slide, it will be very difficult for the government to reach anywhere close to the target.

From the actual revenue collection numbers and trends, it is very doubtful that the revised estimates will be achieved in 2019-20. This, therefore, raises more doubts about the revenue and capital receipt targets for 2020-21. The resource mobilisation suggested in Union Budget 2020-21 is over-ambitious and does not look achievable. Even the 2019-20 RE numbers will be difficult to achieve.

Expenditure Accounts

On the expenditure side, the numbers seem to be more in line with the 2019-20 RE. CGA data shows that revenue expenditure till January had reached 85 % of the revised estimates for the year. Capital expenditure had reached around 77 % of the revised estimates by January 2020 (Table 3).

A look at the expenditure numbers published in the budget show that the government has reduced total expenditure by about 3 % in 2019-20 RE from the 2019-20 BE. However, while the revenue expenditure has been reduced by about 4 %, there is an increase in capital expenditure of about 3.15 % in the revised estimates (Table 3). As stated before, it is difficult to understand the logic of a contraction in government spending in a demand-deficient economy.

For 2020-21, the government has projected a nominal increase of around 12% in revenue expenditure and 18 % in capital expenditure over the 2019-20 RE. The increase in capital expenditure per se is welcome, though, as discussed earlier, as a share of GDP this is very low. The nominal increase in total expenditure is projected to be around 12.74 % for 2020-21. Assuming an inflation rate of around 5–6 %, this implies a real rate of growth in government expenditure of 6–7 %. 11 Minutes of the Monetary Policy Committee Meeting February 4 to 6, 2020 show that RBI revised CPI-based inflation upwards to 6.5 % for Q4:2019-20; 5.4-5.0 % for H1:2020-21; and 3.2 % for Q3:2020-21. However, this increase will be contingent on the government’s resource mobilisation.

Given that the targets are too ambitious the inevitable revenue shortfall is likely to be adjusted through a reduction in capital expenditure. Generally, nominal revenue expenditure is politically more difficult to reduce, and it is easier to adjust capital expenditures. Given the possibility that the government may not be able to meet its revenue collection targets, it will be interesting to see how it will tackle the revenue and capital expenditures for 2020-21.

5. Fiscal Stimulus: Then and Now

The last major episode of a slowdown of the Indian economy occurred at the end of the UPA-1 government, coinciding with the global financial crisis, when the GDP growth rate came down to 6.7 % in 2008-09 from 9.3 % in the prior year. It will be useful to compare the fiscal policy adopted at that time with the present situation.

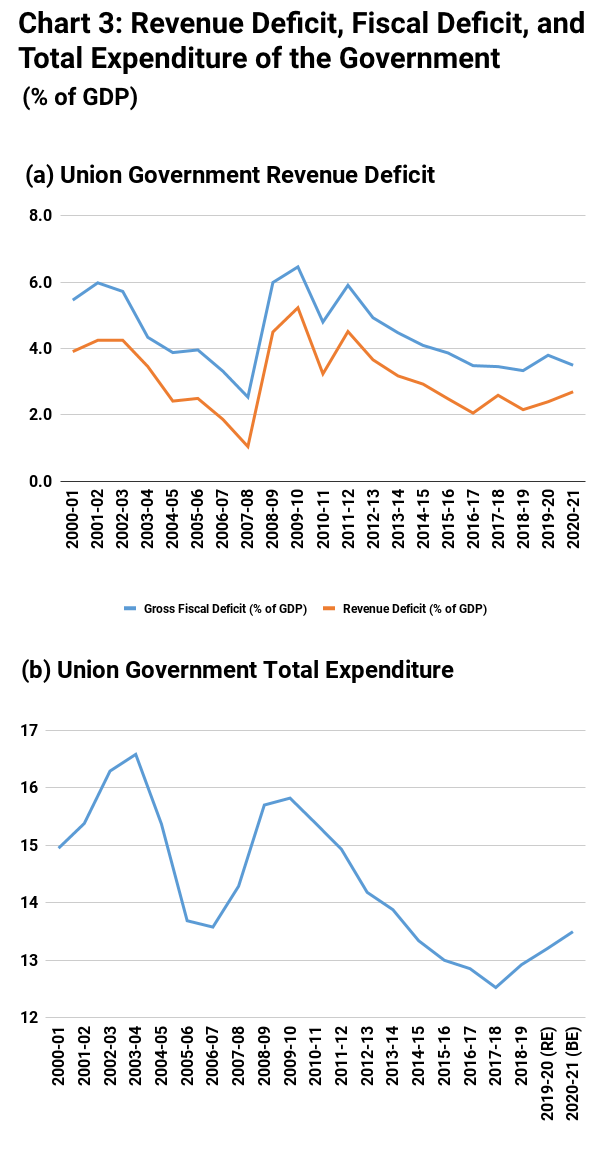

In 2008-09 the fiscal deficit went up within a year to 6.5 % from 2.5 % (Chart 3). India’s quick recovery from the crisis can be attributed to three quick successive fiscal stimuli—one each in December 2008, January 2009, and February 2009—when total government expenditure went up to around 15.5 % of GDP in 2008-09. These packages had been primarily in the form of tax relief and increased expenditure on public projects to create employment and public assets. Central VAT was cut by 4 percentage points, several import duties were reinstated, and there was a substantial increase in spending on projects including housing, infrastructure, irrigation, textiles, rural employment, and social assistance. These apart, the Indian Infrastructure Finance Company Limited (IIFCL) was allowed to raise Rs. 4,000 crore.

Of course, the ensuing increase of the gross fiscal deficit (GFD) by 4 percentage points within a year was overkill, if not a case of fiscal irresponsibility. This expansion of the GFD took place on the eve of an election, and some of the election year sops were camouflaged as part of countercyclical fiscal policies. However, while the UPA-1’s fiscal stimulus measures could have been an over-kill, the increase of expenditure by just 1 percentage point to 13.5 % of GDP over the four years to 2020-21 is meagre.

Was it the diagnosis of the slowdown as on account of financial fragility that prompted the BJP-led government to refrain from adopting any further stimulus? Has the Narendra Modi government lost faith in the power of Keynesian macro policies in handling the slowdown? Was the government too concerned with the fiscal obsession of the international financial organisations and foreign portfolio investors? In the absence of any clear-cut vision, one can only speculate on the reasons.

6. Some Concluding Observations

The budget speech by the finance minister this year was replete with verses from famous poets. Our analysis in a way reminds us of a poem by the celebrated Bengali poet Sukumar Ray, who immortalised children’s literature. He writes of a device for running fast. The contraption, invented by the fictional character Chandidash’s uncle, ties some alluring food on his shoulder. The desire to reach that food induces him to run faster. In fact, the greater the lure of that constantly moving food, the greater will be the acceleration. Union Budget 2020-21 reminds us of that contraption used as a means for self-deception by Chandidash’s uncle.

7. Postscript

The coronavirus attack came at a time when India was already in a major slowdown. The unprecedented country-wide lockdown that has been imposed is expected to have a devastating impact on the economy. There is going to be severe impact on both growth and the stability.

Therefore, the fiscal year 2020-21 will be a time for hard decisions and a strong fiscal stimulus. But the numbers in Union Budget 2020-21 indicate that the government’s ability to do so is limited. To start with, the budget was overly optimistic and did not include any major stimulus to boost domestic demand. On the other hand, revenue projections were based on unrealistic expectations. As the coronavirus attack has basically pushed the economy over the edge, there is simply no way that the budget numbers can be met. Given the present scenario, it is also doubtful how much of resource the government will be able to mobilise for any relief package. From our analysis it appears that the government needs to think out of the box and shed some of its fiscal fundamentalism to tackle this extraordinary economic crisis that is now on us. This, unfortunately, it is not willing to do. Thus, the fiscal package announced on 26 March is inadequate to deal with the deep disruption that will be caused by the three-week lockdown. The relief package will add up to less than 1% of India’s GDP. In comparison, in the United States, the Covid-19 related relief package approved by the US Congress the same week would account for nearly 10% of that country’s GDP.