The Indian economy has had the distinction of being one of the fastest growing economies in the world over the last three decades. Yet, today there is a sense of economic malaise in the air. The young are feeling frustrated as there are too few good jobs on the horizon for them. Rural areas are in distress as farm incomes have stagnated. Corporate investment has declined. Banks burdened with bad loans are finding it difficult to lend. Exports have declined. There are telltale signs of the onset of a further slowdown.

The Government is also showing signs of panic. Soon after witnessing the unease in the corporate sector after her budget speech in July 2019, the Finance Minister started holding consultations with business leaders to assuage their displeasure. The tax surcharge on income of over Rs 2 crore on capital gains of individual and institution investors (domestic and foreign) has been removed; only that on salaries and rent received by individuals remains. Several other measures have been announced: the merger of some public sector banks, recapitalisation, loan melas and moratorium on repayment of micro, small and medium enterprise (MSME) loans. All of these, except the last one, are supply side measures and are unlikely to have much of an impact anytime soon on stimulating demand.

Will the corrective measures recently taken by the government arrest the slowdown? If they do not, what would?

The measure that has received the most media attention is the corporate tax cut. In the third week of September came the announcement that the corporate tax rate would be cut from 30% to 22% for firms that do not seek any exemptions and from 35% to 25% for those who do. For manufacturing firms the tax rate would be as low as 15% for those making investments after October 2019. The news was welcomed by the corporate sector and boosted the Sensex index on the day of the announcement by as much as 4.5%.

How did such a state of affairs come to pass in this fast growing country? Will the corrective measures recently taken by the government arrest the slowdown? If they do not, what would? This essay is an attempt to answer these questions by examining the genesis of the present problems and then asks what should be the way forward. The goal is to put together a plausible and coherent story.

1. Development in a Dual Economy

Before we start putting together an explanation for the present state of affairs, we should understand the structure of the Indian economy.

Let us start by defining the terms ‘formal’ and ‘informal’. The ‘formal’ sector consists of all the registered firms (i.e., firms employing 10 or more employees) plus the government sector. The ‘informal’ sector consists of the rest. Typically, formal sector jobs are better jobs in which the workers get some basic benefits like provident fund, pensions, etc. Informal sector workers do not. Agriculture -- the sector that employees the largest part of Indian labour force (over 40%) -- is informal. Much of the rural economy is informal and so is a part of the urban economy. Eighty percent of India’s population makes their living in the informal sector and produces half of India’s GDP. Almost all the poor toil in the informal sector.

Consider India as a dual economy made up of two free trading regions – “Urban” and “Rural”. Urban is more developed and hence the average incomes are higher there. This is so because typically Urban growth is based on productivity growth in the formal sector while Rural growth is based much more on productivity growth in the informal sector (agriculture).

Typically, labour productivity and also the potential for productivity growth tends to be higher in the formal sectors like industry than in an informal sector like small-scale agriculture. Faster industrial growth would allow agricultural labour to move to higher productivity jobs in industry, and this can be a significant contributor to the overall growth propelled by productivity growth in each sector.

When there are fewer farmers left tilling the same amount of land, they too see an increase in their incomes. There can be a further increase in agricultural incomes through productivity gains in agriculture. When rural incomes rise, they also result in an increased demand for industrial goods, thus producing a virtuous cycle of growth. This is what happened in successful Asian countries. Not only did they grow fast, but they also managed to drastically reduce poverty in a generation.

All developed countries have gone through this process. Even large agricultural exporting countries like the United States (US), Canada and Australia have a miniscule percentage of their labour living off agriculture now.

The two oft repeated questions: ‘Why is the economy not creating enough good jobs?’ and ‘Why is there such rural distress?’ have a common answer. India has not succeeded in producing enough high productivity jobs to draw labour away from agriculture. Of course, there are further reasons for the present distress in rural areas, demonetisation being an important one. We will discuss these later.

If developed countries underwent this process and so did many other Asian countries, why is India taking so long to do this? To understand this let us first understand the strategy employed by the successful Asian countries.

2. A Successful Developmental Strategy

Except for the city-states like Hong Kong and Singapore, all the successful Asian countries were primarily agrarian before they industrialised. What they accomplished within 20 years was a total transformation of their economies.

Initially, the policymakers concentrated on increasing productivity in agriculture. This directly increased the incomes of the rural population, and, in addition, allowed a higher level of agricultural exports that would, in turn, enable imports of machinery and technology.

When a country industrialises in a transformative way, it needs to undertake some major structural reforms.

Late-developing countries have the advantage that they can rapidly improve their productivity by transferring technology from developed countries rather than having to invent it themselves. Some of the technology transfer is done through foreign investment and the rest through direct purchase or copying. However, in order to absorb the transferred technology they need a well-trained labour force and supporting infrastructure. Moreover, in order to sustain a high rate of capital formation, they needed to have a high rate of domestic savings. All the Asian success stories paid due diligence to these essential aspects of development.

When a country industrialises in a transformative way, it needs to undertake some major structural reforms. In order to facilitate a movement of land and labour to their more productive use, laws pertaining to land and labour may have to be reformed. In order to facilitate savings by households, the financial system needs to be modernised. The financial system should be easily accessible for people no matter where they live and also it should be able to inspire trust. Foreign investors should be assured of legal protection of their intellectual property rights. The success of these Asian countries was based on these basic preliminaries.

Another crucial aspect of their development strategy was to start by focusing on producing labour-intensive goods (textiles, footwear, toys, etc.) for the markets in developed countries. They could thus take advantage of their cheap labour and then produce these goods in quantities far in excess of what they could have sold domestically. Thus, domestic demand was never a constraint for them in expanding their industries producing goods in which they had a comparative advantage.

There is a certain logic behind this export-led strategy for fast growth. First, when firms can see that there is a potential market for their products they are inclined to make investments. Second, to be able to accumulate capital, a country needs to have a high savings rate; but high savings imply low domestic consumption and hence low domestic demand. However, when a country produces for foreign markets, the trade-off between savings and consumption becomes irrelevant. It can afford to have a high savings rate domestically. With access to export markets, it can have both high domestic savings and high demand coming from consumption abroad. In addition, there is a much greater choice in what to produce as the world demand is bound to be more diverse than domestic demand.

The manufacturing sector, especially labour-intensive manufacturing, does not require years of university education to acquire the requisite skills. A high-school graduate or less with some on the job training is often adequate for most of the jobs in manufacturing. Surplus labour from the informal sector, including agriculture, can move into labour-intensive manufacturing with minimum additional training, as long as they have basic skills like literacy and numeracy. This is what happened in Taiwan, South Korea, Thailand, Indonesia and China. Lately, even Vietnam and Bangladesh have followed course.

Most importantly, as their industrial sector expanded, they absorbed more and more labour from agriculture – a sector with markedly lower productivity. Poverty declined as labour moved to a more productive sector, and the productivity of the remaining agricultural labour also increased. The growth was fast and also inclusive.

It is important to mention that their respective governments actively aided this effort to develop a manufacturing sector in select areas with an eye on export markets. This was done through an industrial policy that included low interest loans, land grants, tax holidays and requisite infrastructure like power, container ports and other transportation networks. Albeit, it is easier to do it in countries where the democratic norms are rather flexible.

3. Why has India Failed to Follow the East Asian Script?

Unlike the East and Southeast Asian governments, the Indian government did not direct the course of the post-1991 growth. Liberalisation certainly helped unleash market forces but the course of development was determined more or less through serendipity.

When the licence raj ended in 1991, a few significant aspects of the reforms determined the subsequent course of the Indian growth story. In 1992, the government monopoly on the communication sector officially ended. The years between 1994 and 1999 saw a great deal of churning in this sector. Gradually, cell phones became pervasive. This was an opportune time for communication technology to take off in India. Due to excessive emphasis on public sector investments since 1960s in high-end technical and managerial institutions like the IITs and IIMs, there was a surplus of highly trained manpower available.

At the same time, there was a sudden surge of demand all over the world for IT professionals as the Internet was appearing on the world stage. Indian engineers who were over-skilled for the Indian market had been migrating to the US since the 1960s where they had managed to establish quite a reputation. All this turned out to be fortuitous for Indian firms like TCS, WIPRO and Infosys to emerge on the world stage. Communications and business services grew to be India’s fastest growing sectors from 1993 to 2004 at 20.7% and 24.3% per annum, respectively. Software exports grew at the astronomical rate of 34% per annum over that period 1 Gangopadhyay. S., M.G. Singh, and N. Singh, "Waiting to Connect: Indian IT Revolution Bypasses the Domestic Industry," New Delhi: Lexis – Nexis Butterworth, 2008. .

[I]nclusive growth in India is a far more difficult prospect for India in 2020 than for China in 2000.

India’s fast growth episode was propelled by exports of IT services. It was indeed an export-led growth. However, unlike China’s or South Korea’s growth through manufactured exports that absorbed low-skilled labour in vast numbers, India’s growth episode was led by a high-skilled service sector that failed to adequately absorb unskilled labour from agriculture.

In the early 1990s, India could have also developed its manufacturing exports like China and South Korea. But there were several major obstacles: restrictive labour laws that created incentives for keeping the scale small; an outdated land acquisition law that made the process of acquiring land extremely messy; weak infrastructure limiting access to power, ports and roads and, most importantly, a badly educated labour force. Successive governments have found it challenging to address, let alone overcome, these obstacles.

India has some unique problems that make any progress on this front difficult. First, any laws pertaining to agriculture and land are in the State List of the Constitution. This means that each state makes its own laws. The Centre can only override them if and only if they are repugnant to a law passed by Parliament. Land is also designated by whether it is agricultural land or not. In order to locate a large industrial project on any land designated as agricultural land, the state government needs to buy it from the farmers and sell it to the industrial house or change the land-use classification of the concerned area. In most states, this is a source of massive corruption and creates incentives for state politicians to block any attempt by the Centre to change these laws.

Labour laws are in the Concurrent List of the Constitution. This means that the residual powers remain with the Centre, and the Central Government has greater degrees of freedom to change the laws. Yet, successive governments have found it politically difficult to do so. Rajasthan made some changes under the Bharatiya Janata Party (BJP) state government, but these changes were marginal.

The existing laws are set up so as to put more restrictions on larger employers, especially with regard to adjusting the work force in response to changes in demand. This discourages attaining scales that would allow Indian manufacturers to compete internationally. These laws can be endured in situations where demand does not move cyclically, which was the case in India for many years in the past. However, international markets are notoriously cyclical, and firms need to adjust their output with a fair degree of flexibility.

More importantly, since the mid-1990s, the Indian economy too has been displaying distinct business cycle behaviour, which makes the impact of these laws even more damaging. In fact, this could be an important factor driving the process of automation and robotics in Indian industry.

After China entered the World Trade Organization (WTO) in 1999, it went on to occupy most of the unfilled space in the developed countries’ markets for manufactured goods. “Made in China” became a universal brand. It became much more difficult for countries like India to compete with China after that. In addition, the climate for international trade has recently changed. Developed countries have witnessed a denuding of their manufacturing sectors and the widespread resentment due to it has led to the election of right wing nationalists like Donald Trump. Countries such as the US are not so receptive any more to importing cheaper goods from low wage countries.

Moreover, Indian workers now have to compete not just with Chinese and Vietnamese workers but also with robots and artificial intelligence. Even in India, firms have strong incentives to make production more capital-intensive. This is not just because of labour laws but also because long-term interest rates are not that much higher than short-term interest rates. The long and short of this is that inclusive growth in India is a far more difficult prospect for India in 2020 than for China in 2000.

Yet, we must ask how other democratic nations like Thailand, Malaysia, and Indonesia have managed to solve these problems. Especially the problem of skilling the labour force. Even Bangladesh managed to develop a strong textile sector that could compete in international markets. When primary and secondary education itself fails to impart basic literacy and numeracy, any subsequent skilling programme is bound to fail. Why has public education been such a challenge for India?

The genesis of India’s present problems of a lack of job creation and rural distress lies in these factors.

Why did the growth of domestic investment and consequently the rate of gross capital formation slow down after 2008?

It is important to note that the Asian success stories including that of China were based on an extremely high rate of investment. You need investment to create jobs and wages by bringing in new technology as well as by adding more capital (machines). India’s investment rate has not been bad at all, compared to the other Asian countries, except China. But it has faltered of late, particularly post the Global Financial Crisis of 2008.

Why did the growth of domestic investment and consequently the rate of gross capital formation slow down after 2008?

4. Investment Slowdown

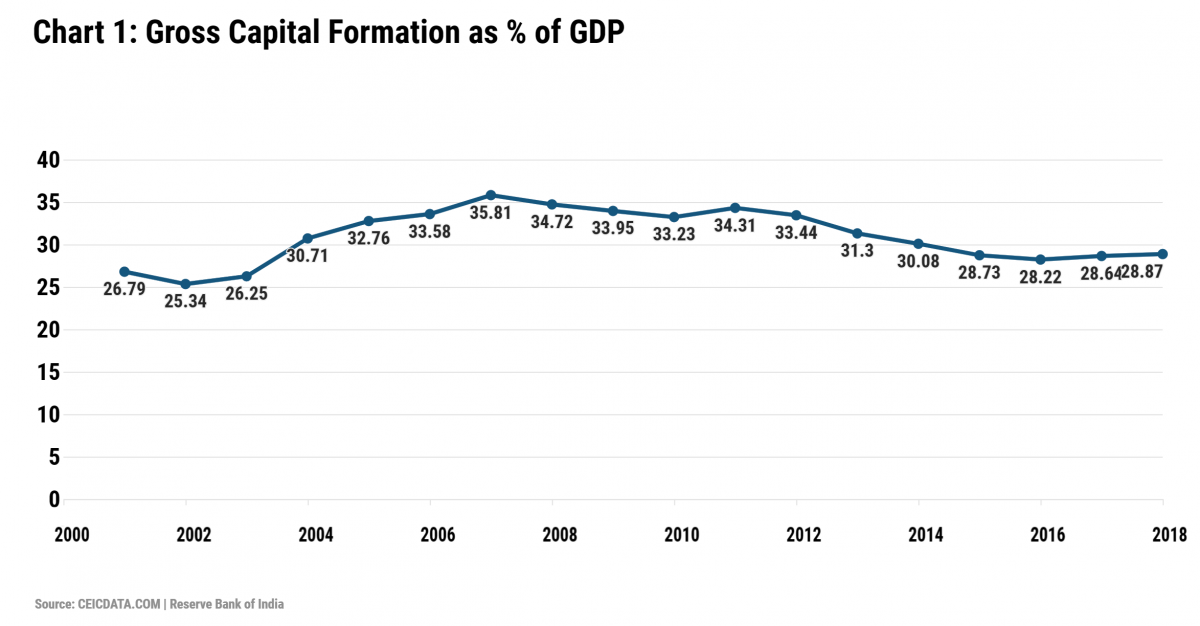

To understand the present slowdown it is useful to examine the ups and downs in the rate of domestic investment or gross domestic capital formation (GDCF) as a percentage of GDP between 2001 and 2018 as in Chart 1 below.

It is easy to see that GDCF as a percentage of GDP grew impressively from 25.3% in 2002 to 30.7% to 2004, then kept growing to 35.8% in 2007 (the highest rate of investment reached so far). This was a high growth period for the Indian economy. However, it was also a period of high credit growth. The investment spree was financed by heavy borrowing by the corporate sector. Corporate exuberance during the boom period of 2002-08 partly explains the present state of indebtedness of the corporate sector, but it is a necessary corollary to a high investment/high growth development process.

In the aftermath of the Global Financial Crisis of 2007-08, corporate investment fell. The post-2011 period is a period of decline in investment as massive corruption scandals rocked the Indian economy and the corporate sector faced a backlash from watchdogs like the CAG and from investigation agencies like the CBI etc. There was some recovery after 2014 but that was torpedoed by demonetisation at the end of 2016. Initial exuberance during the high growth period of 2002-08 and then the shock of the 2008 financial crisis are the root causes of corporate indebtedness of today.

There was a major slump in international demand after the 2008 crisis and inevitably Indian exports slumped. There is no doubt that the slowdown in the Indian growth rate as well as in domestic investment should be attributed to this world-wide phenomenon.

What is surprising is the fact that the GDCF rate does not decline that much and in fact recovers to 34.3% in 2011. A plausible explanation for this is that in 2008 international food prices rose due to many extraneous reasons, including because following high oil prices, large food producers in North and South America shifted their land to cultivation of crops to produce crops for gasohol. This rise in world prices pulled up domestic agricultural prices in India. (Minimum support prices — MSPs — were repeatedly raised during this period.) As a result, the terms of trade shifted in favour of agriculture. This most likely brought about a significant redistribution of income in favour of the rural sector which, in turn, gave a boost to investment in the informal sector. This compensated to some extent a fall in corporate investment.

[A] change in the terms of trade probably played a significant role in maintaining a high rate of investment even after 2008.

This hypothesis is supported by the fact that this was also a period of rising rural wages and declining poverty numbers. Perhaps the introduction of the National Rural Employment Guarantee Scheme (NREGS) helped to some extent. But the scheme took several years to get going in many parts of the country. We believe that a change in the terms of trade probably played a significant role in maintaining a high rate of investment even after 2008.

This episode does offer a clue as to how a transfer from the urban to the rural sector suggests itself as an antidote to the present slump in aggregate demand. This is an issue that we will explore toward the end of this essay.

GDCF declined steadily from 34.31% to 28.73% in 2015 and has stayed stagnant thereafter. There are two big reasons for this. First, by 2015, it had started to become clear that the Indian corporate sector was heavily indebted. As debt soared, investment growth declined. Also, at the end of 2016, the Indian economy had to suffer the enormous shock of demonetisation that hit the informal sector especially hard. A decline in the demand from the informal sector also resulted in unsold inventories of the corporate sector. In a 2017 report, Credit Suisse pointed out that 40% of corporate debt was held by firms that could not hope to earn enough to even cover their interest costs. There was an alarming growth in corporate debt. It grew from 34.2 % of GDP in 2002 to 56.8% of GDP in 2018. (https://fred.stlouisfed.org/series/QINPAM770A, Original Source: Bank of International Settlements.)

Why did corporates over-borrow? Was it just irrational exuberance? Or was it the result of the weakness of the Indian banking system? Unfortunately, it was both. After the heady days of fast growth from 2002 onwards, faster growth was anticipated despite the fact that world demand had slackened. Corporates invested heavily on the back of bank credit. Infrastructural investments, clearly essential for long-term development, also reached a peak around 2012.

Much more importantly, there is systemic moral hazard built into the Indian banking sector. Public sector banks can always rely on public revenues to bail them out. As a consequence, they have never bothered to develop a decent risk assessment system. Moreover, politicians have often directed them to loan money to their pet projects. For example, there is the present government’s MUDRA programme that obliges banks to give small loans to informal sector businesses without collateral. Or, periodic loan waivers to farmers. All this has made the Indian banking sector prone to moral hazard.

5. Financing Infrastructure

Infrastructural projects are typically long gestation projects. They take a long time to complete and a long time to start yielding financial returns. To preclude the strain on public revenues, the government resorted to Public Private Partnerships (PPPs). It was both, the public sector banks as well as private banks, that provided funding for these projects. Both types of lenders exhibited poor risk assessment. Non-bank financial corporations (NBFCs) also joined in the lending spree and faced even fewer obstacles in doing so as they were not constrained by even the kind of regulation that commercial banks have to observe.

There was a great deal of infrastructural building during the years 2006 to 2012. Infrastructural investment went from 4.7% of GDP in 2006 to 8.4% of GDP in 2012 and then declined to 5.1% in 2013. It very gradually rose very slightly to 5.6% of GDP by 2017 2 Nikore, Mitali, “Infrastructure Financing Gaps in India: Need for Focused Resource Mobilization in Irrational Economy", Times of India Blog, March 27, 2019. .

Large-scale projects have to face many hurdles – acquiring land and then getting environmental clearances being two of the most difficult ones. Even the most recent land acquisition legislation (2013) makes acquiring land for industrial production a complex and time-consuming process. You can now understand why private investors especially those who had borrowed for infrastructural projects ended up defaulting on their loans. If the project gets stuck in legal wrangles for a few years, the horizon for getting returns from the project moves away while they are obliged to pay interest on their loans over a longer period. At some point, the project becomes worthless and investors walk away or default.

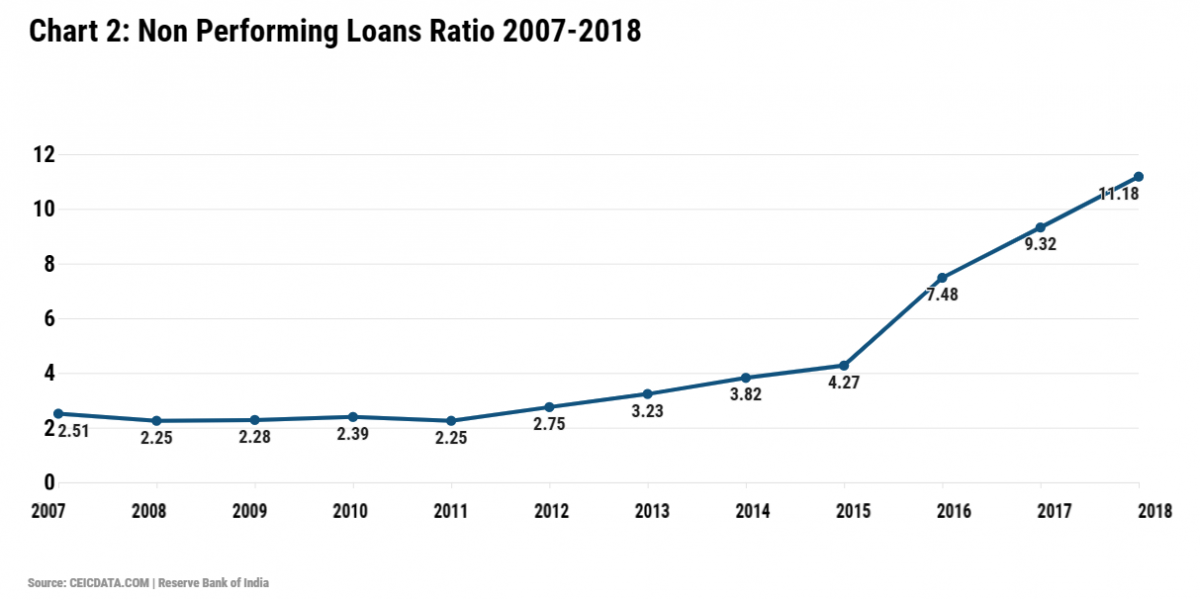

Roads and power stations can remain half built and end up as non-performing assets on the balance sheet of the lending agency. See Chart 2 to appreciate the rise in non-performing loans ratio (defined as the ratio of ‘loans overdue by more than 90 days to the total loans (which defines a NPA)’) over the last decade. Notice how steeply it goes up after 2015.

What happened in 2015? That was the year when RBI Governor Raghuram Rajan asked the banks to clean up their bad balance sheets and applied much greater scrutiny of their affairs. It would, therefore, be misleading to interpret this sharp rise in NPAs purely to imprudent lending in the recent past, as some of the current narratives would have us believe. It should be noted that even in developed countries, gross NPAs are around 4%. There is no reason to believe that India was consistently superior on this count; indeed to the contrary.

Thus, there was a 10-year period from 2004 to 2014, when India NPAs were lower than the global norm. Not because of superior banking skills, but because of pervasive “evergreening” of bad loans. These chickens finally came home to roost in 2015. What is happening today is a stock effect that should gradually correct itself through a combination of write-offs and much lower levels of new NPAs.

But there are new problems looming before the banking sector — a potential meltdown in the NBFCs triggered by the IL &FS crisis, and growing defaults in MUDRA loans.

When large NBFCs like IL & FS default, it also creates NPAs on the balance sheets of the banks they borrow from. When corporates cannot complete their projects, their own balance sheets as well as the balance sheets of the banks and NBFCs develop a large set of NPAs. This is the twin balance sheet problem that the Indian economy is plagued with today. This is a serious problem for the economy as it results in corporates curtailing their investment and banks curtailing their lending. As of January 2019, the gross NPAs to total outstanding loans ratio stood at over 10% and it is disproportionately born by public sector banks.

The MUDRA loans are a different story altogether. In the aftermath of demonetisation, when the informal sector was faced with a serious liquidity crunch, MUDRA loans enabled a number of these firms to stay afloat by repaying the outstanding bank/NBFC loans. Unfortunately, things have not improved sufficiently since then for the informal sector and now they face the prospect of defaulting on their MUDRA loans.

Demonetisation in 2016 was a serious negative shock to the rural economy that had already been reeling under successive drought years since 2014. Rural investment as well as consumption declined after demonetisation.

One thing that is clear from the above account of how we got here is that this sort of problem will keep recurring until there are structural reforms in land acquisition, banking regulation, labour etc. One step was taken with the passage of the Insolvency and Bankruptcy Code Act in 2016. It allowed lenders to put a closure on bad loans that were never going to be paid back. They could write off the bad loans but could get quick access to the borrowers’ collateral that they could then liquidate. This will help in relieving the gridlock in the financial system, but not entirely. In the first place, NBFCs have very few assets other than their loan portfolios, which may not be easy to unwind. Second, MUDRA loans are non-collaterised, so there is nothing to liquidate.

There are also a number of systemic problems with India’s banking system that cannot be easily solved. First, public sector banks that hold three-fourths of the total deposits have been unabashedly used by politicians and their management is very much subject to a serious moral hazard. Second, commercial banks in India are ill-equipped to be effective lenders for long-term projects on the basis of short-term deposits. Long-term bond markets are not yet well developed in India. Third, financial institutions in India are poorly regulated.

The problems in the financial sector have now affected overall demand in the economy. Aggregate demand consists of private investment by domestic producers (rural and urban), public investment, export demand and consumption. Demonetisation in 2016 was a serious negative shock to the rural economy that had already been reeling under successive drought years since 2014. Rural investment as well as consumption declined after demonetisation. Export demand was already declining due to slow growth in developed countries. The indebtedness of corporations dampened corporate investment. As inventories started piling up, the corporates started laying people off. Firms invest when they see signs of rising demand for their products. Presently, they see none. This, in turn, resulted in the slowdown of consumption growth. This is why we are witnessing signs of an onset of a more serious slowdown today.

We do not think the recently announced cut in corporate tax is an effective way to stimulate demand.

Will the new bold initiative of corporate tax cuts help arrest the slowdown? The main idea behind the tax cut is to remove the disincentives for corporate firms to produce in India by bringing down the corporate tax rates to those prevailing in competing nations like Vietnam. But is there any reason for us to believe that this would stimulate demand by inducing corporates to increase investment? For it to work as a demand stimulant, the logic would have to be as follows: tax incentives would encourage firms to cut prices that would tempt reluctant consumers to the market and spend. But there are better ways to bring prices down – for example, a cut in the Goods and Services Tax (GST). We do not think the recently announced cut in corporate tax is an effective way to stimulate demand.

As mentioned before, corporate investment is being withheld because they do not expect any increase in consumption demand. If nobody is going to buy, why produce? We called it a bold move because at least over the short run, the proposed tax rate would also cause a substantial revenue loss to the government hurting for revenues. If the aggregate demand does not budge, the revenue loss is estimated to be very substantial – Rs. 1.45 trillion. It is worth asking if it might not have been more effective to use this huge sum to stimulate demand in a more direct fashion.

However, in the long-run perspective the move makes good sense. Nations do compete with each other to attract foreign investment and the corporate tax rate is certainly one aspect of this competition. However, it is not the only one. The ease of doing business, the integrity of the legal system to enforce contracts, the state of the infrastructure, and the quality of the labour force are equally important. In the absence of structural reforms, it seems unlikely that even in the long run the new initiative of the corporate tax cut alone will make a substantial difference to India’s fortunes in attracting multinational investment.

In our story, the demand slowdown today is not just a cyclical slowdown that can be cured by a monetary measure like lowering interest rates or a fiscal measure like a tax cut. Instead, it is a combination of having missed the express bus of export-led growth with manufactures through our tardiness in carrying out structural reforms, and then the shocks of demonetisation and messy implementation of the GST that flattened the informal sector of the economy. The challenge of structural reforms is a long-standing one. The rest of the factors are of a more recent vintage.

In addition to the above factors, there is growing unease among the corporate executives about harassment by tax authorities. This stems from a peculiar world-view held by the top level of the government that all bad economic outcomes have at their source bad or corrupt people. “If we use the disciplinary organs of the state to go after everyone who could be potentially corrupt, the system will be cleansed and the economy will start humming again.” This kind of thinking may win elections but does little to perk up the economy. Demonetisation and tax raids are a testament to this. But draconian and extra-judiciary measures ensnare the innocent as well as the guilty and make the country inhospitable for business. This is an additional reason for the slowdown of business investment over the last few years.

6. The Way Forward?

It is clear that fast, sustained and transformative growth that will create good jobs, relieve rural distress and take India to the ranks of a developed country is not possible unless some structural problems are solved. These include vastly improving the public education and public health system to improve India’s human capital, reforming labour and land laws, improving the financial system, and changing the suspicious and punitive attitude toward business.

The idea of a rural-led strategy is predicated on the notion that at this juncture in time it might be easier to revive demand in rural India than in urban India.

Market forces operate through the animal spirits of entrepreneurs and there is little scope for these to manifest themselves unless the structural bottlenecks are cleared. Governments of different parties have come and gone and these structural problems have remained unresolved.

Yet, it is not clear that even if the domestic obstacles are overcome, India will succeed in charting the East Asian course of development (through labour-intensive exports of manufactures) to the extent that China and other Asian countries did. As mentioned earlier, the times are different now. Developed country markets are less receptive to imports from low wage countries. Automation has eroded the comparative advantage of cheaper Indian labour. What then is the way forward?

7. Rural-led Strategy

An approach worth trying is a rural-led growth. The idea of a rural-led strategy is predicated on the notion that at this juncture in time it might be easier to revive demand in rural India than in urban India. Growth driven by productivity growth in agriculture and the informal sector would be slower than industry-led growth. But it would make more sense given the state of affairs today.

Urban demand growth has slowed down due to the myriad reasons recounted earlier. The skewed pattern of growth in India over the last several decades implies that income growth has been concentrated in the same upper crust of the population that benefited from skill-biased technology. Their demand for consumer durables may have now reached a saturation point. If a person who already owns a house gets richer, he or she is not likely to buy another house. If on the other hand, a person marginally below the income that makes house ownership affordable experiences an income increase, he or she may be inclined to buy a house. Here we are taking the “house” just as an example of an urban product. But the principle is valid for any consumer durable. In general, the marginal propensity to consume will be higher for lower income consumers.

[O]ne way for the Government to arrange for an urban to rural transfer is by increasing the terms of trade for agriculture through an increase in MSPs.

Rural consumers, on an average, are poorer than urban consumers. A transfer of income from the urban to the rural would therefore tend to increase overall consumption demand. Some of this will be for goods produced in the urban sector such as two-wheelers and other consumer durables. Farmers in the upper strata may also be induced to buy expensive items like cars, pick-up trucks and tractors if they experience an income boost.

It is also true that after repeated drought years, demonetisation and GST, the rural population has been in distress for several years. They are likely to have a great deal of pent up demand. Any transfers to them are likely to spill onto a demand for durables as well as non-durables. All this suggests is that transfers to rural areas through different government schemes such as the NREGS, the Public Distribution System (PDS), the Pradhan Mantri Awas Yojana (PMAY) and pensions, should be regarded not just as poverty alleviation schemes but also as antidotes to the present slowdown.

Most forms of urban to rural sector transfers would require the government to tax urban residents and subsidise rural residents. However, the claims on the existing revenues are many and the Government’s capacity to garner more revenues is limited. Under the circumstances, one way for the Government to arrange for an urban to rural transfer is by increasing the terms of trade for agriculture through an increase in MSPs. Of course, this would also mean an increase in food subsidy through PDS to prevent an increase in the issue price. However, such an increase in government expenditure would be a more effective stimulant since the entire burden of increasing demand would not fall on the treasury. Demand for food of the urban consumers is inelastic. An increase in the MSP would result in a direct transfer of ready cash income from Urban to Rural. It would no doubt increase the hardship of the urban poor who are not protected by access to PDS. However, it would help the urban residents by alleviating the demand slowdown in their economy. The Government did increase the MSPs for several crops in July 2019 but they could be raised higher.

We would like to suggest that under the present circumstances when the prospects of exporting to developed countries are weak, when structural reforms in land and labour laws are not easy to implement, and when reforming public health and education is taking a very long time, it would make sense to explore ... a rural-led strategy.

Note that an increase in MSP is only the second best option of bringing about an urban to rural transfer when fiscal constraints make other avenues of transfers infeasible. It may distort the crop choice toward crops whose MSPs are raised. It may create storage problems and frictions with WTO. Worse still, it will create inflationary pressures making the measure politically difficult. Yet, we are suggesting it as an effective way to bring about transfers to the rural economy if all other avenues are blocked. We find support for our idea in the events following 2008 when MSP increases prevented a growth collapse, despite the crippling effect of a slow-down in demand for software exports after the Global Financial Crisis.

Is this just short-term thinking? Do we not think of industrialisation as synonymous with development? We would like to suggest that under the present circumstances when the prospects for exporting to developed countries are weak, when structural reforms in land and labour laws are not easy to implement, and when reforming public health and education is taking a very long time, it would make sense to explore the avenue of a rural-led strategy.

Urban manufacturing requires a larger scale and this is what is running smack into India’s hard-to-reform land and labour laws. Large manufacturing units also need environmental clearances, delays in which are partly the reason for many projects being stalled. Rural growth may steer clear of these obstacles.

Why is the rural economy poor and stagnant? If they just produce to satisfy their own demand, there is no point in raising productivity. If they increase the output of food, prices will fall as their own demand for food will not be elastic enough. They would ideally like to export to the urban economy and perhaps also to the rest of the world. To accomplish this they must diversify into fruits, vegetables, flowers, dairy, poultry etc., for which urban consumers will have a relatively elastic demand. They need infrastructural facilities like refrigerated storage, suitable transport, even agro-processing industry.

A rural-led strategy should prioritise this type of investment. A rural-led strategy would imply diverting some of the public investment from urban to rural areas. Even though in principle there is greater potential for productivity growth in urban industry, the systemic obstacles to industrial development makes a rural-led strategy relatively more fruitful. The additional advantage this sort of strategy would generate is that it would create a lot more jobs for unskilled and semi-skilled labour. Consequently, growth would be much more equitable and the trend towards widening inequality would be thwarted.

It is worth noting that though now China has become the manufacturing hub for the whole world, the first steps it took after it started liberalising from 1979 to 1986 focussed on increasing agricultural productivity. The intermediate stage of Township and Village Enterprises (TVE) was an attempt to utilise the resources available in its rural areas and for providing employment there. Even other successful countries like Taiwan, Indonesia, Malaysia, and Thailand paid a great deal of attention to the development issues in their countryside. Indian policymakers should take notice.

We believe that it does not make sense to set economic goals in terms of GDP (a 5 trillion $ economy) for a country like India. Growth is just the means to the end of poverty reduction. A high growth rate is desirable because it may lead to a faster poverty decline. But how much impact an increase in the growth rate would make on poverty would depend on the pattern of growth. Himanshu reports on the basis of the 2017-18 Periodic Labour Force Survey that despite the fact that the growth exceeded 6% from 2015 to 2018, consumption expenditure per capita has declined at the rate of 4.4% per annum in rural areas and by 4.8% in urban areas 3 Himanshu, “What happened to poverty during the first term of Modi?”, Live Mint, 15 August 2019 https://www.livemint.com/opinion/columns/opinion-what-happened-to-poverty-during-the-first-term-of-modi-1565886742501.html . This is much more alarming news than the growth slowdown.

A rural-led strategy will deliver slower overall growth but it will have a bigger impact on poverty under the present circumstances that keep the East Asian strategy out of India’s reach for now.

The analysis and arguments in this article have benefited from discussions in recent times that both authors have had with a large number of individuals, far more than can be named here. Our thanks to all of them. Ashok Kotwal would like to thank Parikshit Ghosh, Ashwini Kulkarni, Milind Murugkar and Bharat Ramaswami for many useful conversations.