Much of the discussion during the past few years on the economic slowdown in India has focused on supply-side remedies such as lower corporate taxes that would increase the profitability of investment. Even now, the government’s measures to tackle the economic crisis due to the Covid-19 induced lockdown are largely supply-side measures. Yet, many corporates have shown a great deal of hesitation in making new investments. A big part of this hesitation comes from the perception of investors that they see only lacklustre growth in the demand for their products.

Low investment translates into slower growth and this makes it a vicious spiral— it can stop a growth spurt in its tracks. We argue in this article that this is the fate of any growth episode that is not inclusive.

Our aim is not just to outline our view of how to tackle the immediate problems facing the Indian economy, but more to reflect on the general question of what is a desirable path of development for a country like India, one that will sustain growth over a long time in the conditions now prevailing in the world. In order to understand this better we must first understand the role of perceived demand in the process of growth. For sustained growth, there has to be a self-reinforcing process that generates virtuous cycles of economic expansion. Any impetus to growth through either technological improvement or through access to a new market must generate new waves of demand in its wake, otherwise the growth episode risks turning out to be short-lived.

Domestic firms will be emboldened to venture into unknown territory and invest serious amounts of money if, and only if, they are certain about a market for their products.

There are, of course, many lessons to be learned from the model of ‘export-led growth’ of the East Asian economies. The name of the game was to effect a transformation from a relatively low productivity economy to a high productivity economy. How did they do it? The East Asian economies saw a huge reservoir of latent demand in richer countries waiting to be exploited. They realized that if they could tap this demand, they could pull themselves up by their bootstraps. Their strategy was simple: start by exporting primary products, buy technology from developed countries, skill your labour force, produce cheaper goods with the help of cheaper domestic labour, and flood the markets of developed countries. As more and more of the East Asian labour force moved from the informal (less productive) to the formal (more productive) sector, their incomes rose, increasing domestic demand. Fast growth was achieved as an increasing proportion of the labour force became engaged in high productivity activities.

Domestic firms will be emboldened to venture into unknown territory and invest serious amounts of money if, and only if, they are certain about a market for their products. As long as they can produce quality goods at lower prices than those prevailing in developed markets, they would feel assured enough to take the risk. As the economy gets transformed, national income and consequently domestic demand keep growing, giving a further boost to their confidence.

However, the first prerequisite for such a process to play out is that there has to be a sizeable pool of demand waiting to be tapped. The period of 1970 through 1990 was propitious for this strategy for the small countries that became known as Asian Tigers. China, the world’s most populous country, came on to the scene in the 1990s. In 2000, it joined the World Trade Organization and followed this strategy with gusto. Within 10 years it managed to flood world markets with its exports. It managed to become the fastest growing country over a long span of time and lifted 800 million people out of poverty.

[F]or a country like India, or for that matter for any other country, to now try and emulate the Asian Tigers model is a daunting task as China has occupied much of the space in global markets.

There is little doubt that an export-led strategy is attractive. Data from the Centre for Monitoring the Indian Economy’s (CMIE) consumer pyramids show that even after nearly two decades of relatively high growth in India, 60% of India's consumer expenditure is on food and energy. For the bottom half of the population, this proportion is 70%. The domestic market for goods and services beyond these essentials is still quite limited in India. When export markets are open, the limited domestic demand ceases to be a constraint.

But for a country like India, or for that matter for any other country, to now try and emulate the Asian Tigers model is a daunting task as China has occupied much of the space in global markets. Smaller countries like Bangladesh can find a specialized area like garments where they can still carve out their own space, but for a large country like India it will be a very big challenge.

There are also some India-specific factors that work against export-led growth.

First, the infrastructure sectors that can facilitate industrial growth and exports are subject to regulatory agencies of varying quality: either because of a lack of capacity, or because of ambiguity about the independence of the regulators, or because of excessive dependence on judicial review (Kapur and Khosla 2019).

Second, there is now an unmistakable trend towards protectionist trade policies that will discourage firms that are a part of global supply chains from locating in India.

Third, while it is well understood that our laws relating to labour and land serve neither equity nor growth very well, our democratic federal polity has been unable to reform them in a decisive fashion. Without such reforms, it is hard to build manufacturing units with large enough scale that could compete internationally.

What then?

Of course, whatever progress that can be made toward facilitating export-led growth will be welcome, but it is also important to explore a parallel path. There is much discussion now about focusing on domestic demand. What would be a growth process if it were to depend solely on domestic demand?

How would a corporate CEO, say of an auto manufacturing firm, make a decision to invest? Even if she has adequate funds or access to ample credit to make fresh investments, she would first want to be certain that there is enough demand in the market to absorb an increase in output. If she overestimates the demand, inventories would accumulate, as is presently the case.

When most of the growth accrues goes to a thin top layer of the population, the demand for an existing industry does not grow that much.

The high growth rate experienced by the Indian economy during 2002–2012 was driven by a rapid growth in exports, particularly of software services. It so happened that there was a burst in demand across the world for software services at the beginning of the millennium, at which point in time India happened to have an excess supply of appropriately trained manpower (Kotwal et al 2011). The incomes of workers in software services rose rapidly and so did their consumption levels. They bought houses, cars, and restaurant meals, which created jobs in construction, manufacturing and services. This in turn had a spillover effect on the rest of the economy. Some segments of the manufacturing sector such as pharmaceuticals and auto parts found export markets, and this had a similar spillover impact on the economy. However, those whose incomes were directly earned from export opportunities constituted a very small part of the labour force.

Moreover, any possible trickle-down effect depended on how the thin layer of initial beneficiaries from the increased demand for their services spent their higher incomes. Do they spend them on goods and services produced by low-skilled and poor workers?

When most of the growth accrues goes to a thin top layer of the population, the demand for an existing industry does not grow that much. When a software engineer experiences a substantial wage hike, she graduates from a two-wheeler to a car. But when her salary moves up further, she does not necessarily go out and buy another car. She would likely save much of the increase or probably plan a trip to Europe.

The central role occupied by effective demand in this analysis follows a distinguished tradition that goes back to John Maynard Keynes, Michal Kalecki, and Marx.

On the other hand, when families that cannot afford cars see a sufficient rise in their incomes to cross the threshold of affordability, they create an additional demand for cars. A car here is just an illustrative example. This would apply to any consumer durables or non-durables. A pattern of growth that generates sustained growth is one in which there is a continuous upward movement of people coming out of poverty into middle and then higher incomes. Such a process creates a continuous increase in new demand, incentivizing firms to invest and expand production. The income generation process and the resulting demand patterns have to be in sync for the process to be sustained (Murphy et al 1989).

The central role occupied by effective demand in this analysis follows a distinguished tradition that goes back to John Maynard Keynes, Michal Kalecki, and Karl Marx. This was referred to by Marx as the “realization” problem. He argued that the "ultimate reason for all real crises always remains the poverty and restricted consumption of the masses" (Sebastiani 1989).

Given the spending patterns of the `haves’ (discussed in more detail below), not much of their income increases translates to demand for the goods produced by low-skilled workers. The growth episode of 2002–2012 had a small trickle-down effect. But the effect was limited. given the vast reservoir of unskilled workers in the informal sector engaged in subsistence activities.

Leaving aside the fall-out of the coronavirus-induced crisis, taking a long-term view, the international demand for software services is no longer as strong as before. The Indian economy is waiting for another autonomous increase in demand. Where can it come from? The current slowdown pre-dates the coronavirus crisis and was an inevitable consequence of a weakening of the demand for India’s software services. Even if Indian financial institutions had been in a good shape, GDP growth would have slowed down. This sort of growth episode inevitably fails to maintain its momentum and unless new triggers are either created or present themselves, it will sputter to a halt.

To see this more clearly, let us first look at what incomes at the top end look like.

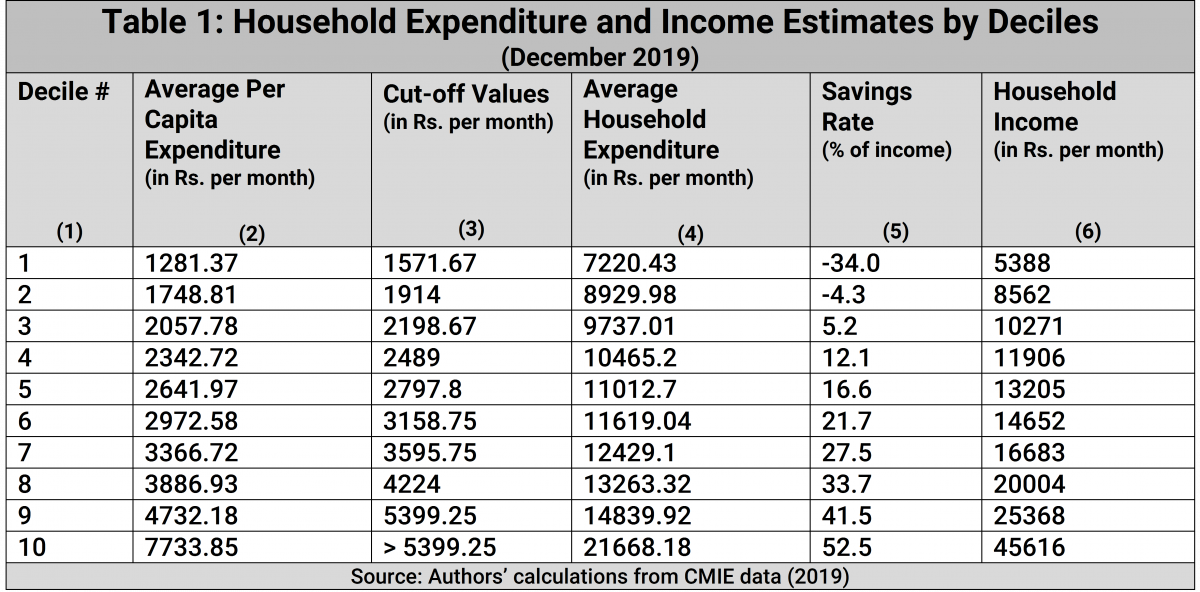

As an illustrative example, we looked at the consumption expenditure data from CMIE’s consumer pyramids (Table 1). We picked the month of December 2019, which is a recent enough period and yet distant enough from the pandemic-induced slump. From this data, we use per capita expenditures to order the population.

The second column of Table 1 reports the average per capita expenditures of 10 deciles (containing one-tenth of the population) from the lowest spending (Decile 1) to the highest spending (Decile 10). The third column reports the maximum per capita expenditures in each decile. The fourth column reports the average household expenditure in each of these deciles.

To convert these expenditures to household income, we need to know the savings rate. We turn to the ICE survey of the People’s Research on the Consumer Economy that was conducted in 2013/14. In their 2016 article Shukla and Sharma reported the savings rate by income deciles. We assume that these income deciles and the respective savings rates have remained stable from 2013/14 to 2019. These savings rates are reproduced in the fifth column of Table 1. The last column contains the estimates of income in each decile. No doubt these are rough estimates, but they are comparable to other estimates and are useful to understand the possibilities of a domestic demand-led growth process. 1 Bhattacharya (2016) reports the distribution of income from the 2013/14 ICE survey. The top 20% earn 45% of disposable income as against our rough estimate of 41%. The bottom 60% earn 32% of aggregate disposable income as against our estimate of 35%.

First, note that the richer a household, the higher its savings rate. Thus, when incomes grow for a higher rather than a lower income household, a significant part goes toward savings rather than consumption demand.

Notice that the cut-off value between 9th and the top (10th) decile is Rs 5,400 per capita. According to CMIE data, the average of household sizes between the 9th and 10th deciles is 3. Therefore, we can take the cut-off value of the household monthly expenditure as Rs 16,200 (5,400 x 3). Taking the savings rate of 46% (average of 41.5% and 52.5%), we have the cut-off value of household income per month of the marginal household between the 9th and 10th decile as Rs 30,000 (16,200 / 0.54). In other words, all households with a total monthly income of Rs 30,000 or above belong to the top decile. As a comparison, the typical salary for an engineer at the leading software firm Infosys in 2020 is Rs 450,000 per annum, or Rs 37,500 per month.

Hence, it is safe to assert that the skilled technical and managerial workers in the organized sector mostly fall within the top decile of household incomes. Conservatively, we can say that they would at least fall in the top two deciles. This is also supported by the ICE data, which shows that the top two deciles to be overwhelmingly urban. It also shows that `middle India’ (located between 20 and 80 percentiles of the income distribution) is “largely composed of those who lack a high school education” (Bhattacharya 2016). Bhattacharya concluded: “What this means is that you are quite unlikely to encounter the truly poor in your daily life if you live in a metro, and those you think of as the urban poor (your maid or your driver, for instance) are likely to be closer to the top of India’s income distribution than to the bottom.”

Many of us euphemistically call ourselves ‘middle class’ but though we may not be rich by international standards, we belong to the richest 10% in India.

Notice also how poor most people are in India. The urban poverty line in India of Rs 1,410 per capita (in terms of monthly expenditure) as per the Rangarajan (2011–2012) estimates, adjusted for inflation, in 2019 would have been equivalent to Rs 1,984. The fact that the top decile of the population has a monthly expenditure above Rs. 5,400 suggests that the richest 10% have incomes just between two to three times the urban poverty line. It is a safe guess to claim that most of the readership of this article belong to the top decile. Many of us euphemistically call ourselves ‘middle class’ but though we may not be rich by international standards, we belong to the richest 10% in India. 2 This is hardly a novel observation. Consumer marketing experts have remarked on it often. Of course, as Chancel and Piketty (2019) have shown, there is a huge disparity within the top 10% 3 Figures 10 and 11 in Chancel and Piketty (2019) show how the bottom 50%’s share of national income has declined steadily and how most of the growth since 1990 has been captured by the top 10%. Figure 11 also showed that the tremendous disparity even within the top 10%. The richer you are, the faster has been your growth rate. .

It is well known that workers in the organized sector constitute less than 10% of India’s labour force. In a skill-biased technological growth spurt, as experienced in the decade of 2000–2010, the positive shock to incomes was first experienced largely by the top two deciles. The extent of the subsequent trickle down would be determined by what sort of consumption items the initial beneficiaries would spend on. Would it be things that unskilled and hence poorer workers produce (such as food, clothing, or labour-intensive services) or would it be goods that have a high content of value-added by high-skilled and hence high-income workers? Richer consumers are already satiated with essential items of consumption like unprocessed food. Any income increases to them spill into demand for relatively higher quality services and appliances produced by high-skilled workers.

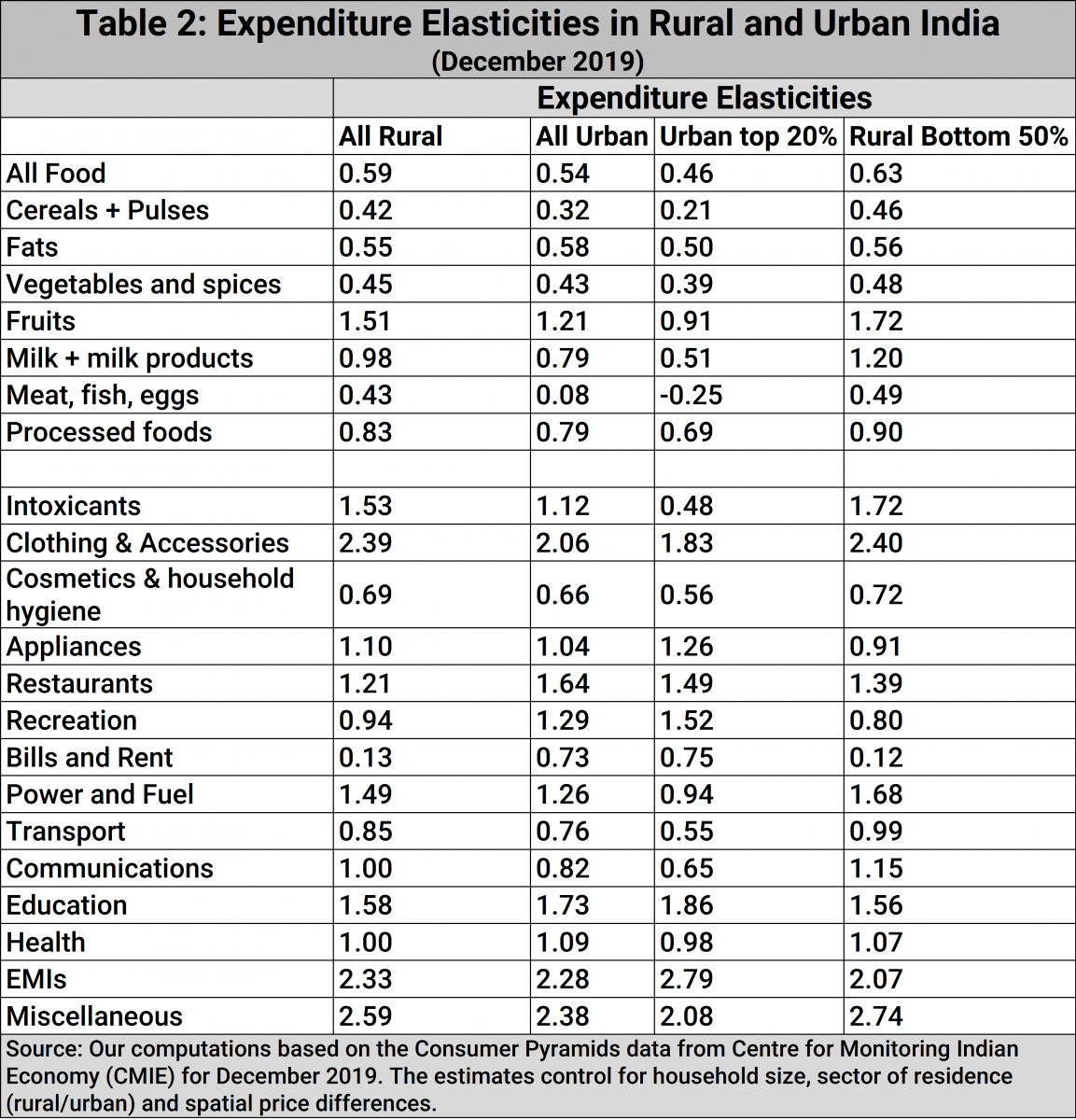

How do the expenditure elasticities — the percentage change in expenditure on a particular consumption good because of a 1% increase in total expenditure — differ across income classes? The contrast is even greater when you compare the bottom five deciles from rural areas with the top two deciles from urban areas.

Table 2, which has been computed from CMIE data collected in December 2019, shows that the expenditure elasticities for the richer consumers (the top two urban deciles) are lower than for the bottom 50% of rural consumers for all goods and services, other than appliances and EMIs, recreation, restaurants, bills and rent, and education. These items clearly have a greater value added by skilled workers and are typically produced in the organized sector. The bottom five rural deciles have far greater expenditure elasticities on all foods, clothing, intoxicants, cosmetics, transport, communications, health, and miscellaneous items. Thus, any autonomous increases in incomes of the bottom five rural deciles would create subsequent spending cycles for goods produced by low-skilled and hence low-wage workers (those in the bottom five deciles) as well as for several goods and services produced in the organized sector. This will generate a bottom-up growth that would be sustained for a longer time.

Note also that the expenditure elasticities for rural residents in general tend to be higher than those for urban residents as a majority of the poor live in rural areas. A majority of the households in the bottom deciles happen to be rural residents.

If business confidence is low due to a perceived lack of demand by the investors, growth skewed in favour of high-income households perpetuates the problem. Indian growth has been remarkably skewed, so it was inevitable that at some point it would slow down.

It may be asked at this point as to why it is that aggregate demand is raised as an issue only for an economy that is performing in a state of recession or excess capacity— a down phase of the business cycle. In other words, any measure like an expansionary fiscal or monetary policy is invoked only to correct a short-term fall in aggregate demand. As far as long-term growth is concerned, what is supposed to matter are supply-side factors like technology, the availability of inputs such as skilled labour, or capital.

We feel that mainstream macroeconomists seem to have in mind a world of atomistic firms who make their decisions by looking only at market prices and their marginal costs. However, for a country like India, where most of the population is employed in low productivity activities in the informal sector and where the size of the firms scarcely exceeds 10 workers, the task of productivity improvements falls on the formal sector that is capable of absorbing new technologies and can have a viable scale of operations. Such a formal sector typically consists of corporate oligopolies. These firms do consider the expected aggregate demand and from that they deduce the demand for their own products.

This background discussion helps us understand the relevance of arguments such as growth having stalled because corporations are not investing and that, in turn, is because they see no emerging demand on the horizon. It is well accepted in the corporate world that expected demand is always the most important factor in explaining investment growth (de Vijlider).

One way of kick-starting aggregate demand is to generate autonomous demand domestically. How likely is it in India?

The problem of stagnating investment in an oligopolistic economy was discussed by Paul Rosenstein-Rodan in the context of post-war Italy in the late 1940s. He illustrated it with the story of a shoe factory. The CEO of the factory wonders whether he should invest more to expand production. By hiring more workers, he would raise the incomes of the workers, but they would spend only a tiny fraction of this additional income on shoes. What if he is the only investor who expands production capacity? If no other business owner follows suit, who then would buy his shoes? If each CEO thought this way and decided not to expand production in their respecive factories, the economy would stagnate.

Rosenstein-Rodan suggested that a possible solution to the problem is a 'Big Push’ by government to coordinate investment by all corporations across different sectors. This would assure all firms that an increase in aggregate demand is imminent and they should have confidence in the economy. This requires adroit coordination of private investment by the government while resisting interference. A formal analysis of the Big Push idea was presented by Murphy, Shleifer, and Vishny (1989 a).

One way of kick-starting aggregate demand is to generate autonomous demand domestically. How likely is it in India? In another paper published at the same time, Murphy, Shleifer, and Vishny (1989 b) focus on growth in agriculture, where reside more of the low-income households. The economic structure Murphy, Shleifer and Vishny adopt is very similar to the one that exists in India today.

Eighty-five percent of India’s labour force makes its living in the informal sector, which consists of tiny firms with little access to credit, knowhow, or skilled manpower, and produces 50% of GDP. Seventy percent of the population lives in rural areas and that includes 89% of the bottom quintile (ICE 360 Household Survey). Only 39% of rural India’s GDP is produced in agriculture and the rest (manufacturing, construction and services) of the economic activity is sensitive to changes in agricultural incomes. When farmers experience an increase in their incomes, they spend it on goods and services produced locally as well as in the formal sector, often located in urban areas. Given the extremely low productivity of much of Indian agriculture, the wrong crop mix in cultivation, poor rural infrastructure, and low connectivity to markets, it is clear that there are a lot of low hanging fruits to pluck in the agricultural sector. 4 In a recent article Abhijit Banerjee and Esther Duflo (2019) have opined that high growth rates are achieved only when there are a lot of low hanging fruit to be plucked and yet much can be achieved even under low growth rate to improve the well-being of masses. We agree completely, but we think that there are still a lot of low hanging fruit to be plucked in India and especially in the agricultural sector.

For the millions of low-skilled workers locked into grain cultivation, diversification represents a real opportunity to advance their incomes.

The challenge is to increase rural incomes and not just output. Without drastically changing the crop mix, a mere output increase would result in a price fall making the rural poor poorer. The key is to change the crop mix so that rural products find demand in the urban sector where incomes are growing. A transition from grains to horticulture, dairy, wine, or poultry will increase incomes. Economists rightly stress the movement of labour and other resources from agriculture to other sectors as the key to increasing incomes, especially among the poor. However, they often fail to realize that an equally important transformation, especially at low incomes, occurs within agriculture: from predominantly grain-based agriculture to one that is diversified and produces grain as well as fruits, vegetables, milk, eggs, meat, and fish. The latter foods have higher income elasticities and demand shifts in their direction when incomes rise. For the millions of low-skilled workers locked into grain cultivation, diversification represents a real opportunity to advance their incomes.

Diversification requires supporting research and dissemination, a build-up of rural infrastructure, cold storages, and the availability of credit. It also requires the development of cooperative societies and similar aggregation services to make marketing easier. This, in turn, would increase rural demand for urban products (in addition to demand for locally produced goods and services) and a virtual cycle can then be established. Growing urban incomes will stoke rural economic activity and rising rural incomes will, in turn, create an upsurge in the demand for urban produced goods. There will be a healthy resonance across the urban and rural economies, making growth self-sustaining.

If the rural economy starts humming…the rise in rural incomes will persuade the formal sector in urban areas to start investing and absorbing the excess labour from the rural areas.

Since mass psychology is an important ingredient of an economic resurgence, it is also worth asking whether a virtuous cycle through a rural-led growth strategy would dispel the present despair engulfing the country. We think that the answer is definitely ‘yes’.

Currently, formal sector is not absorbing enough of the excess supply of labour accumulating in agriculture. In addition to depressing per capita incomes in rural areas, this is creating armies of frustrated and angry youth. Countries do not have too many opportunities to reap a ‘demographic dividend’. India is wasting its golden opportunity. If the rural economy starts humming, it will not only create local jobs in manufacturing, construction, and services, but the rise in rural incomes will persuade the formal sector in urban areas to start investing and absorbing the excess labour from the rural areas. The start of such a process will no doubt create a buoyant mood among investors as well as consumers. A rudimentary form of this argument stressing the importance of a rural-led strategy appeared in Kotwal and Sen (2019).

To summarize, the overall argument underlying the suggested rural-led growth strategy is based on three separate but connected points, all valid in an environment of low aggregate demand.

First, autonomous income increases that go to the poorer segments of the population give a bigger boost to aggregate demand as the poor tend to spend a larger fraction of their income increases.

Second, the poor tend to spend more of their income increases on the kind of goods and services produced by low-skilled labour. This has a more benign distributional impact, which also contributes towards raising aggregate demand.

Third, the policy solution we suggest is capable of generating complementary demand cycles between rural and urban economies, making the growth spurt last longer. This lies behind the title of this essay. For example, when policy interventions enable a change in the rural crop mix, the rural economy starts producing goods that urban consumers want. As urban consumption of these goods rises, it will channel more income towards rural producers. But as Table 2 indicates, when compared to the top two deciles of urban consumers, the rural population, especially the bottom half, spends a higher percentage of their income increases on the more labour-intensive urban-produced goods. These further increase demand for the urban produced goods and consequently raise urban incomes, and so on.

None of these arguments are meant to suggest that the path of export-led growth is completely blocked. The usual suggestions like the reform of factor markets are still very much valid. However, rural development has been neglected so far and a rethink along the lines we suggest will aid rather than inhibit the process of transformation of the Indian economy.

Yet, it must be acknowledged that fast growth rates (over 5% in per capita real growth) have only been possible for the East and Southeast Asian countries that employed the strategy of export-led growth at a propitious time in history. Rural-led growth relying on domestic demand is not likely to generate such high rates of growth. However, slower growth that directly benefits the bottom tier of population and generates its own momentum for a long enough time to transform the whole economy is preferable to a rapid burst that benefits only a few and exhausts itself in a short time.