At the Davos Summit of the World Economic Forum in mid-January, India was clearly a favoured country. Multiple reasons were given to support the view that India is rising, while China weakens.

“I see a lot of businesses, a lot of companies looking to India as an investment destination as they try to diversify away from other countries, including China,” Gita Gopinath, deputy managing director of the International Monetary Fund (IMF), is reported to have said. Even prior to Davos, World Bank country director Auguste Tano Kouamé had stated that “India’s economy has been remarkably resilient to the deteriorating external environment.” Bank estimates suggest that India’s GDP growth would touch 6.6 per cent in 2023, as compared with just 4.3 per cent for China.

The resulting optimism is spurring projections that India is likely to be a new leader of sorts in the world system. The London-based Centre for Economics and Business Research has predicted that the country, now a close to $3.5 trillion economy ranked 5th in the world, will grow at an average rate of 6.4 per cent over the next five years, and at 6.5 per cent over the following nine years. This would make it the fourth largest economy, ahead of Germany in 2026, the third largest economy ahead of Japan in 2031, and a $10 trillion economy by 2035. Others see India powering ahead even quicker. Shigesaburo Okumura, the editor-in-chief of Nikkei Asia has declared that “2023 will be remembered for India’s emergence as the third pole of the world,” alongside the US and China.

Such projections and claims from outside the Indian ruling establishment carry with them some credibility. However, experience suggests that the community of financial investors, institutions and analysts often tend to talk up chosen markets in order to keep investments going, especially when the global environment is uncertain. And India is currently a good choice for the purpose for a few reasons.

Talking up India’s growth

First, going by the gross domestic product (GDP) numbers, determined largely by the figures put out by national statistical agencies, India is performing better on the growth front than most other countries. It has emerged out of the worst of the Covid-induced downturn and appears to be managing the effects of the fallout of the Ukraine war much better than many other similarly placed middle-income countries. When a third of the world is headed for a recession according to the IMF, India’s projected 6.8 per cent growth in 2022-23 and 6.1 per cent in 2023 appears creditable. There are downside risks, but those are seen as resulting from the depressed conditions elsewhere in the world.

Second, China is losing its sheen in the perception of international investors, what with western sanctions, domestic efforts to rein in corporates that are favourites of foreign investors, and the recent Covid wave, all adversely affecting investment opportunities in that country. That encourages speculative predictions that India would be a major beneficiary of the relocation of established capacities or shift of new capacities away from China, flowing from the China+1 strategy expected to be adopted by major international firms and the “friend shoring” policies being espoused by the United States and its allies.

Third, there could be a larger agenda here. The advocates of neoliberal policies for the less developed countries have always derived their strength from pointing, often wrongly, to the exceptional economic performance of one or more countries that are identified as having adopted such policies and maintained a close and subordinate relationship with the advanced capitalist world. In the 1970s, South Korea and Taiwan were the favourites, though many pointed to the fact that these governments were by no means neoliberal in terms of their policy stance. The second-tier Asian industrialisers like Thailand and Malaysia, with their manufacturing export boom, were the choices in the 1980s and early 1990s. The Southeast Asian crisis of 1997 that resulted directly from the liberalisation of financial sectors in these economies deprived advocates of liberalisation of these ‘miracles’ that were showcased as examples of the benefits of neoliberal policy regimes.

The West needed a new neoliberal exemplar, and India given it size, its hostility to China, its willing to ally with the US, and with its commitment to neoliberal policies that has only intensified, was an obvious candidate.

For a time, China, recording spectacular growth while it embraced market-friendly policies and relied on export markets and foreign investment to raise rates of growth, appeared to offer an option. But what it lacked was the willingness to maintain a close, let alone subordinate, relationship with western powers. After a brief period of bonhomie, China became the enemy rather than an ally of neoliberal advance, accused of turning surreptitiously protectionist, stealing technology and trade secrets, and posing a geopolitical challenge to peace in Asia and elsewhere in the world.

The West needed a new neoliberal exemplar, and India given it size, its hostility to China, its willing to ally with the US, and with its commitment to neoliberal policies that has only intensified, was an obvious candidate. The difficulty was that India was no export-led manufacturing success. Rather, it was a failure as a manufacturing nation, with the share of manufacturing in total value added in the post-Independence era peaking at around 18 per cent, as compared to the 35-40 per cent standard set by the earlier models of neoliberal success.

Services-led growth

Attempts have been made to counter critical assessments based on this evidence, by arguing that India is forging a new path of services-led growth. The country’s success in software and IT-enabled services exports and the unusual and premature rise in its share of services valued-added in total valued-added from 38 per cent in 1990-91, when liberalisation was formally embraced, to 55 per cent in the pre-pandemic year 2019-20, seemed to justify that perception. Around 59 per cent of the increase in economy-wide gross value added between those two financial years was on account of services.

However, the numbers indicate that not all that increase can be attributed to software and IT-enabled services or even all “modern” services including public administration, health and education. Moreover, the contribution of those services to aggregate employment was far lower than their contribution to value-added and GDP. Low productivity, poorly paid, informal services, such as in retail trade, contribute a large chunk of services value-added and an even large share of employment, much of which tends to be precarious, casual or self- employment. The rapid growth of such services points to the elastic nature of employment in that sector. Absent even minimal social protection, those unable to find gainful employment in agriculture or industry turn to this sector, which has displaced agriculture as the sink for the unemployed or underemployed.

In this connection, recent evidence on sectoral value-added shares is telling. It is known that the Covid-19 pandemic with its requirement of physical distancing, while resulting in a stop in almost all economic activity for varying periods, affected most adversely the services sector. That differential impact seems to be reflected in a reversal, perhaps temporary, of the phenomenon of ‘services-led’ growth with the onset of Covid. The share of services in aggregate gross value-added declined from 55.3 per cent in 2020-21 to 53.6 and 53.7 per cent in the subsequent two financial years, 2020-21 and 2021-22, respectively. The ostensibly leading sector seems to have lost momentum during the crisis year as well as in the subsequent year of recovery.

Fluctuating GDP growth

This tenuous nature of the services driven growth trajectory possibly explains the drive internationally, underway over the last decade or more, to hype up India’s economic performance, using other arguments such as comparative GDP growth. More recently this effort has benefited from idiosyncratic or exceptional factors. One is that the violent fluctuations in production and economic activity resulting from the “exogenous” shock that the Covid pandemic imparted makes it difficult to sort through the evidence. All economies took a hit. So, pointing to numbers in any one of them that would normally reflect poor economic performance seems unfair. No economy, whether rich, middling, or poor was unaffected, so those numbers don’t tell a meaningful story of the “inner” health of the system. On the other hand, the lockdowns that put a sudden stop to economic activity for varying periods of time ensured that both the declines and recoveries were sharp. As a result, the rebound from the depths of the pandemic-induced crisis makes growth appear more robust than it actually is.

The damage inflicted by the pandemic and the government’s response to it on an economy that was already losing momentum was severe. And the economy had not returned to pre-pandemic levels even as late as September 2022.

Yet, in India’s case, comparative GDP growth numbers are most used to hype its performance. That calls for caution when accepting those assessments. Besides the fact that GDP is not the sole or even the most appropriate indicator of development, there has been much discussion about the robustness of the current series of GDP with 2011-12 as base. Methodological changes have resulted in an exaggeration of growth, as suggested by the lack of correspondence with other indicators of output performance. And the estimates leave out of coverage much of India’s overwhelmingly dominant informal sector that has been the hardest hit by demonetisation, the GST regime and the Covid pandemic and its handling.

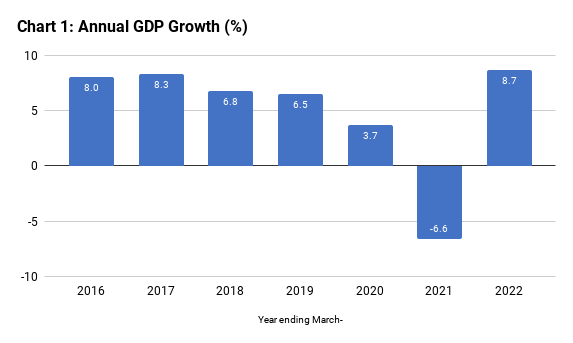

In addition, given wide fluctuations in GDP, conventional ways of reading GDP growth figures can be misleading. Specifically, with dips as significant as during financial year 2020-21, point-to-point growth rates may not present a correct picture. GDP growth that had declined from 6.5 per cent in 2018-19 to 3.7 in pre-pandemic year 2019-20, turned negative in 2020-21, standing at minus 6.6 per cent. What is being celebrated is that GDP rebounded to 8.7 per cent in 2021-22, and the government’s (perhaps over-optimistic) projection is that it would touch 7 per cent in 2022-23 (Chart 1). It is this set of rebound rates that are being cited to say growth in India is strong. But, even accepting the 7 per cent projection for 2022-23, the increase in real GDP between pre-pandemic year 2019-20 (which was by no means a ‘good; year) and 2022-23 would be just 8.6 per cent, which amounts to an average rate of growth of less than 3 per cent a year over three years.

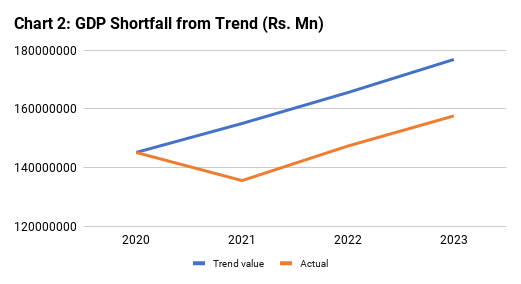

The shortfall in GDP in 2020-23 relative to what it would have been if the trend growth rate of 2010-11 to 2019-20 had been sustained is more than 11 per cent (Chart 2).

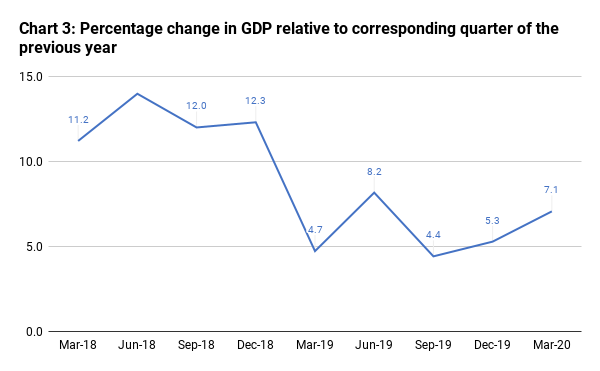

The figures of quarterly GDP, though even less robust, present a more nuanced picture. As Chart 3 shows, the rate of increase of GDP relative to the corresponding quarter of the previous year had been decelerating almost consistently from the second quarter of 2018 (Apr-Jun) till the quarter prior to the pandemic (Jan-Mar 2020). So, when Covid hit, the Indian economy was already slipping. The damage inflicted by the pandemic and the government’s response to it on an economy that was already losing momentum was severe. And the economy had not returned to pre-pandemic levels even as late as September 2022.

External front

This disappointing picture on the growth front is, however, not the principal area of concern about the Indian economy. One disconcerting trend is that, even with growth subdued, India’s deficit in the trade in goods has ballooned, from an average of $37 billion in the three quarters preceding the onset of the pandemic (ending March 2020) to $67 billion in the three quarters ending September 2022. This was not predominantly due to oil. In fact, the oil deficit increased from an average of $21.6 billion to Just $29.1 billion over those two periods, whereas the non-oil deficit rose from an average of $15.7 billion to $37.2 billion.

Services exports and remittances have not neutralised this trend. Therefore, accompanying, the worsening trade deficit was a worsening of the current account deficit as well. That deficit fell from an average of $3.1 billion in the three quarters preceding the pandemic, to an average of $22.6 billion in the three quarters ending September 2022.

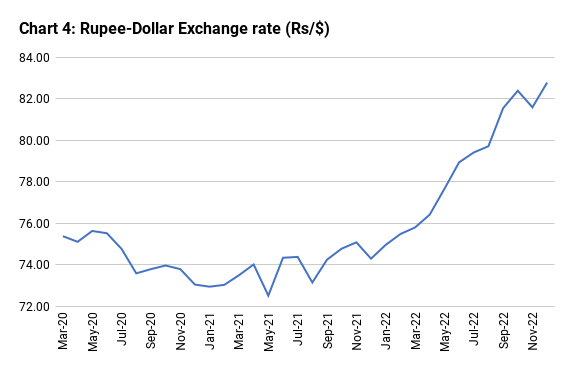

The worsening trade and current accounts deficits are troubling also because they occur in a context in which the rupee has been depreciating. The Reserve Bank of India’s rupee-dollar reference rate depreciated from Rs.72.52 to the dollar in May 2021 to Rs. 82.79 to the dollar in December 2022 (Chart 5). This decline occurred despite the effort of the RBI to stall the rupee’s depreciation by selling dollars from its reserves. Total sales of foreign currency amounted to $227 billion between December 2021 and November 2022, with net sales amounting to $53 billion.

Part of the reason why such action was needed and was not adequately effective was the outflow of portfolio capital resulting from the hike in interest rates in the advance economies and the uncertainty in global financial markets. Net sales by foreign portfolio investors amounted to $18 billion in 2022. While that may be small relative to reserves, the fact that reserves had to be depleted to defend the rupee in the context of rising current account deficits and financial investor exit has increase downward pressure on the rupee.

This vulnerability is a direct fall out of the neoliberal policy regime. An essential feature of neoliberalism in India (and elsewhere) has been the liberalisation of the capital account, with foreign investors allowed easier and more widespread access to equity and bond markets. Combined with a degree of tax forbearance, this had resulted in large net inflows of foreign financial capital and the accumulation of legacy investments in the domestic market. Since India’s current account was mostly in deficit, this had meant that India’s reserves were “borrowed”, resulting from accumulated liabilities to investors abroad rather than of earned foreign currency assets. That increased external vulnerability, since financial investors could exit, and capital could flow out when any developments internal or external adversely affected the “confidence” of speculative investors. Early signs of such outflows triggered responses in foreign exchange markets that have weakened the rupee.

[T]he fact that India’s exports do not include more resilient manufacturing goods, because of the country’s poor manufacturing growth, limits its ability to retain or increase export shares in global markets.

The depreciation of the rupee did not, however, halt, let alone reverse, the deterioration of the trade and current account deficits, by rendering exports competitive and imports more expensive. This is attributable to two factors. First, weaknesses in other countries that are competing for a share of the shrinking global market has meant that their currencies have been depreciating as well, eroding India’s advantage. Second, the fact that India’s exports do not include more resilient manufacturing goods, because of the country’s poor manufacturing growth, limits its ability to retain or increase export shares in global markets. In fact, industry appears to be doing poorly in the post-Covid rebound. In the first eight months (April-November) of 2022-23, industrial output as measured by the Index of Industrial Production rose just 5.5 per cent, and even in ‘rebound’ year 2021-22 industrial growth during April-November was just 7.1 per cent. Clearly, India’s effort to become a manufacturing hub that would in time displace China in global value chains, pursued by means that include the Production-Linked Incentive (PLI) scheme, is not yielding results. India has lagged in manufacturing in the past and continues to do so even after embracing neoliberalism.

A disconcerting aspect of this failure is that even when strategic considerations have pushed the government to adopt a protectionist stance, as suggested by the rhetoric with respect to China, the performance has been exceedingly poor. Trade data released by China indicate that in calendar year 2022, while China’s exports to India rose to $118.5 billion, recording a 22 per cent rise, India’s exports to China fell to 17.8 billion, recording a 39 per cent decline. That took India’s trade deficit vis-à-vis China to $101 billion, as compared with $69.4 billion in 2021. Moreover, while China’s exports to India consisted of relatively high-tech goods like electrical machinery and equipment, machinery and mechanical appliances, organic chemicals and fertilisers, India’s exports consisted of primary products like iron ore, mineral oils, cotton, and cereals.

Conclusions

In sum, neoliberalism has not delivered on its promise to restructure India’s industrial capacity to make it internationally competitive and raise manufactured exports and manufacturing growth. In fact, the evidence seems to be that Indian manufacturing has weakened, with excessive dependence on imports of manufactures, especially intermediates and components, including in areas like pharmaceuticals. On the other hand, the opening of the capital account has rendered India vulnerable to the shocks that can flow from an exit of foreign financial investors.

For a considerable period of time these weaknesses were shrouded by the fact that India was a favoured destination for foreign financial investors and the liquidity this infused into the economy sustained a debt financed investment and consumption boom. As even the official position goes, “aggressive lending practices” in the years after 2003 led to a spike in outstanding advances of the banking system. As a result, growth was high, but was accompanied by the accumulation of a large volume of non-performing assets (NPAs) that remained concealed through restructuring exercises that allowed stressed assets to be treated as standard.

Restoring growth by unleashing another credit bubble is difficult even for a government committed to neoliberalism.

Stressed assets in the public banking system rose sharply along with a rise in aggregate gross advances of public sector banks from Rs. 16,98,570 crore at the end of March 2008 to Rs. 45,90,570 crore at the end of financial year 2014. When in 2015 the RBI decided to mandate an asset quality review based on stricter guidelines, gross NPAs of public banks rose sharply from Rs. 2,16,739 crore on 31 March 2014 to Rs. 8,45,475 crore on 31 March 2018, or from 4.72 per cent of gross advances to 15.52 per cent of gross advances. A consequence was a deceleration in credit growth that was soon reflected in a setback in growth when compared to the heady 2000s. It was on this slowing economy that demonetisation, the Goods and Services tax regime and the Covid pandemic inflicted their damaging effects.

Restoring growth by unleashing another credit bubble is difficult even for a government committed to neoliberalism. While, barring a few exceptional cases, recovery of loans to defaulters has been poor, provisions against bad loans and subsequent write-offs, supported with recapitalisation, have brought down the gross NPA ratio quite sharply. But, having burnt their fingers once, it is perhaps unlikely that banks would be willing to lend, and firms and households be willing to borrow to spur another debt-fuelled growth revival. Meanwhile, inflation driven from the cost side has crossed the ceiling in the central bank’s comfort range, leading to hikes in the RBI’s policy rate. That may not be adequate to attract back foreign investors but could dampen debt financed spending. In the event, even as the global recession intensifies, there seems to be little evidence of any strong revival of growth.

The available evidence on unemployment, underemployment and inequality over the last two decades or more suggest that even in the best of times in terms of growth, a majority of Indians have not derived much benefit. What is emerging now is that a development trajectory that excludes the majority cannot deliver sustained GDP growth either.

C. P. Chandrasekhar retired as Professor from the Centre for Economic Studies and Planning, Jawaharlal Nehru University, New Delhi.