Introduction

The current financial year of 2022–23 has witnessed a sharp recovery of the Indian economy in spite of being buffeted by supply disruptions caused by the Russia-Ukraine war and a consequent rise in commodity prices. In 2022–23, according to the first advance estimates, the economy is expected to expand by 7% over the last year.

Policymakers claim success in having met the challenges of global health and economic shocks because India has reportedly emerged as one of the fastest growing countries in recent quarters. There is therefore considerable optimism that India is now on the cusp of an economic upswing.

Contrary to many apprehensions, output recovery from the pandemic has been sharp and V-shaped. India’s real gross domestic output (GDP, net of inflation) grew at 1.5% in 2021-22 over the pre-pandemic year (2019–20) (Figure 1). According to World Health Organization (WHO) estimates, Covid-19-related deaths were said to be high in India – much higher than the officially reported figures – but they were modest relative to the country’s population.

How did India manage to restrict the negative economic fallout of the pandemic? Reportedly, public expenditure on both consumption and investment as a proportion of GDP were higher during the pandemic years compared with 2019–20 (Economic Survey, 2022-23). An increase in public consumption expenditure partly made up for the decline in private expenditure. The rise in public investment was mostly on road construction – a labour-intensive activity that created much-needed unskilled employment.

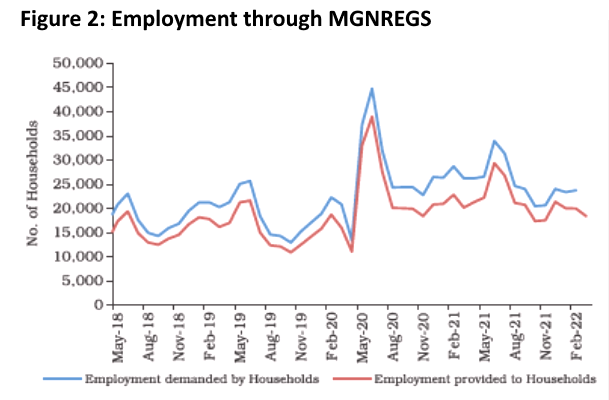

Public consumption was raised largely by expanding the distribution of free foodgrains to the poor under the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY). Data show that the offtake (under all schemes) from the Public Distribution System (PDS) peaked at 109.3 million tonnes in April 2020, was 90.8 million tonnes in August 2021, and 67.8 million tonnes in November 2022. Boosting expenditure on the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), a national, legally mandated, food-for-work programme, to meet its growing demand during the pandemic helped mitigate the fall in private employment (Figure 2). It would perhaps be fair to say that these public expenditures during the pandemic helped the economy cushion the crisis of hunger.

India’s recovery looks better compared to China’s self-inflicted wound of the Zero-Covid policy and repeated lockdowns that have caused enormous human suffering and output disruptions.

Be that as it may, India’s claim of a return to 'normalcy needs to be seen against the decade-long derailment of the economy in the 2010s compared to the growth acceleration witnessed after the 1980s. This essay addresses the setback to growth, investment, and consequent deindustrialisation.

Growth During the 2010s

In 2022 India will be the world’s fifth largest economy with a GDP of $3.2 trillion in current dollars, according to International Monetary Fund (IMF) estimates. In July 2019, Prime Minister Narendra Modi set an ambitious growth target of a $5 trillion economy by 2024, up from a $1.9-trillion economy in 2019. That target looks unachievable by 2024. With a per capita income of $2,191 in 2021, India ranked 144th amongst 194 IMF member countries.

Over the long term, India was amongst the countries that witnessed a steady growth in output between 1960 and 1992. India’s annual average GDP growth rate increased from about 3.5% between the 1950s and 1970s to 5.5% per cent during the 1980s and 1990s. According to a well-known classification of global growth patterns, India was one of the very few “growth accelerators” in the 20th century (Hausmann et al. 2005). Growth further increased to more than 7% per year in the 2000s coinciding with a global boom in trade, output, and capital flows. I had termed this “India’s Dream Run” (Nagaraj 2013) and it lasted till the global financial crisis in 2008.

Never in the past seven decades has India witnessed such an economic reversal, and the gravity of the problem is perhaps yet to sink into the minds of policymakers and the public.

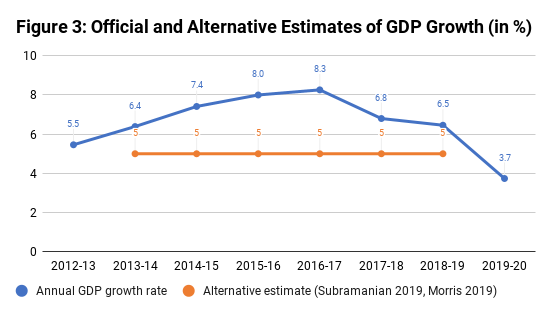

However, India went off the rails in the 2010s as the growth momentum petered out and it staggered into the “mountain” category, according to Prichett’s description of patterns of development (Pritchett 2000). Annual GDP growth rate slowed to 3.5–4% by 2019–20 from 7–8% until 2010–11 If the critics of the current series of GDP estimates are right, the annual growth rate during much of the 2010s decade would be still lower at 4–5% (Figure 3) (Subramanian 2019; Morris 2019).

Expectedly, the deterioration in growth took a toll on related economic aggregates. Well-documented evidence shows a fall in employment levels (with adverse changes in its composition), a rise in the rate of absolute poverty in rural India, and deterioration in the rate of malnutrition (Nagaraj 2020; Kapoor 2020; Subramanian 2019). Never in the past seven decades has India witnessed such an economic reversal.

The gravity of the problem is perhaps yet to be fully appreciated by policymakers.

Deindustrialisation

A notable manifestation of the decade of declining growth rates is premature deindustrialisation which is defined as a sustained decline in the share of output and employment in the manufacturing sector before attaining industrial maturity as the developed nations did. On premature deindustrialisation, Dani Rodrik writes:

In most of these countries, manufacturing began to shrink (or is on course for shrinking) at levels of income that are a fraction of those at which the advanced economies started to deindustrialise. These developing countries are turning into service economies without having gone through a proper experience of industrialisation (Rodrik, 2015).

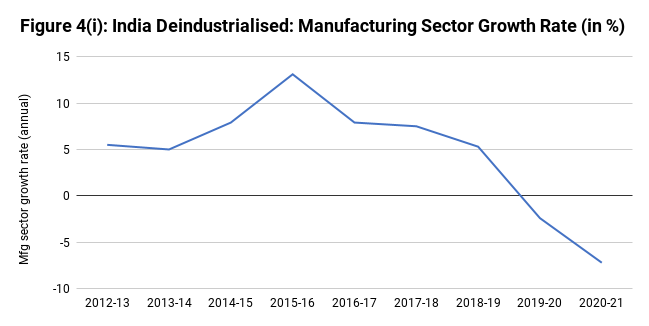

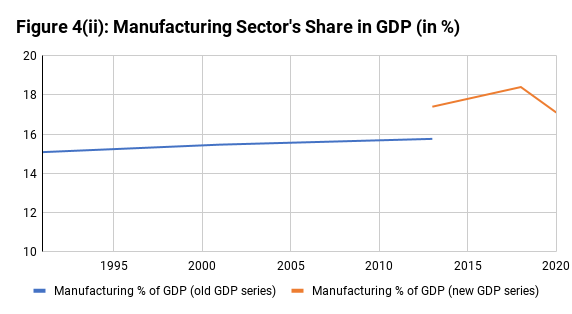

India’s manufacturing sector output growth rate had fallen to a negative 0.4% in 2019–20 from 13.1% per year in 2015–16 (Figure 4 (i)). (All growth rates are at constant prices, unless otherwise specified. ) The deceleration in the growth rate needs to be seen against the stagnant share of manufacturing in GDP for three decades since 1991 (Figure 4 (ii)).

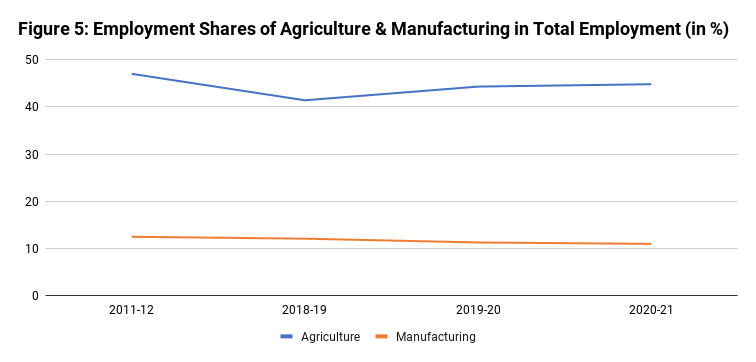

The manufacturing sector’s share in employment fell to 11.3% in 2019–20 from 12.5% in 2011–12, with a corresponding rise in agriculture’s share in the second half of the 2010s (Figure 5). This indicated a reversal of the structural transformation of the labour force (that is, workers moving to lower-productive sectors from higher-productive sectors, including to construction in the informal sector). There was a further decline in 2020–21. However, we ignore this because the pandemic contributed to the decline in 2020-21. It is perhaps worth remembering that structural transformation of the labour force is a defining characteristic of Kuznetsian modern economic growth.

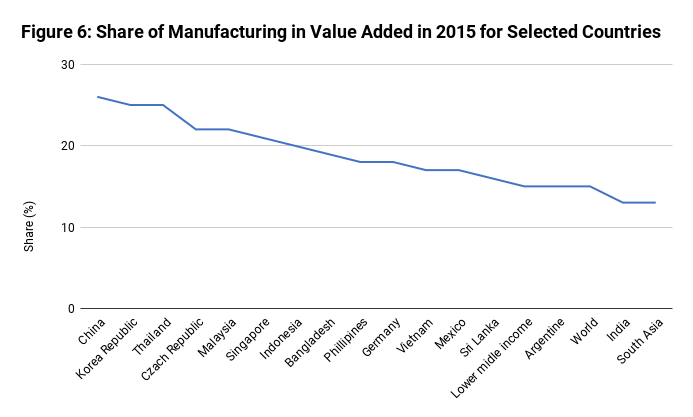

From a comparative perspective, the regression is even more striking. The manufacturing sector’s share in GDP at 13% in 2015 was the lowest amongst industrialising countries, and China’s share was double that of India’s at 26% (Figure 6). (The figure is taken from RBI Deputy Governor Micheal Debabrata Patra’s lecture 'India@75', of 13 August 2022.)

Just three and half decades ago, in 1981, India was a positive outlier amongst industrialising nations with a distinctly higher manufacturing share compared to countries with similar income levels. To quote from a paper authored by Kalpana Koccher, Raghuram Rajan, Arvind Subramanian, and others for the IMF in 2006: “Correcting only for the income terms, India is a positive outlier among countries in its share of value added in manufacturing in 1981 with its share significantly exceeding the norm by 4.6 percentage points” (Koccher et al. 2006).

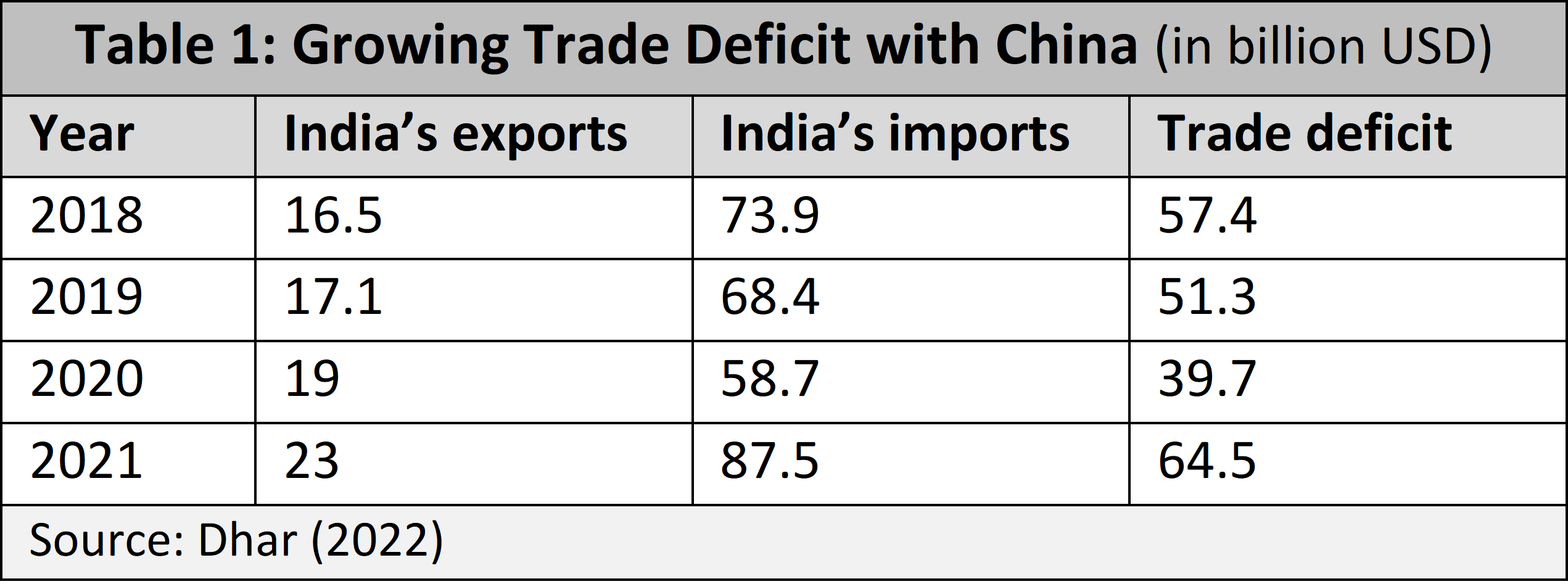

Deindustrialisation has been accompanied by India turning into an import-dependent economy. Between 2005–06 and 2021–22, India’s imports from China, in nominal dollar terms, rose seven times, while its exports increased by just two times. Table 1 shows that the trade deficit has been rising, to $64.5 billion in 2021from $57.4 billion in 2018, according to India’s trade statistics. The deficit is higher according to China’s trade statistics, and it is likely to be even more if the trade from Hong Kong is also included since considerable exports from China are routed via Hong Kong.

These facts tell a story of regression in India’s industrialisation.

The import dependence on China seems structural in that it is not easily corrected by changes in relative prices, but requires long-term interventions. This is best illustrated by what happened during the Covid-19 pandemic. Faced with India’s inability to secure imports of critical intermediate inputs such as active pharmaceutical ingredients (APIs) for the drug industry and fertilisers for agriculture, the Atmanirbhar Bharat Abhiyan was launched in May 2020 to promote self-reliance.

However, after a year or so, swallowing its pride, India quietly undid many such import restrictions as they hurt domestic production because of a lack of suitable intermediate inputs. As a result, imports rose and exports to China fell in 2021–22, over the previous year. Further, to promote industrial investments under the Production Linked Incentive (PLI) scheme, the government is reportedly planning to relax many restrictions on Chinese investment on a case-by-case basis.

Declining saving and investment rates

There could be many reasons for these trends in output and deindustrialisation (Nagaraj 2017a; Nagaraj 2020). However, we would like to focus on the principal reason: the unprecedented retrenchment in aggregate investment rates.

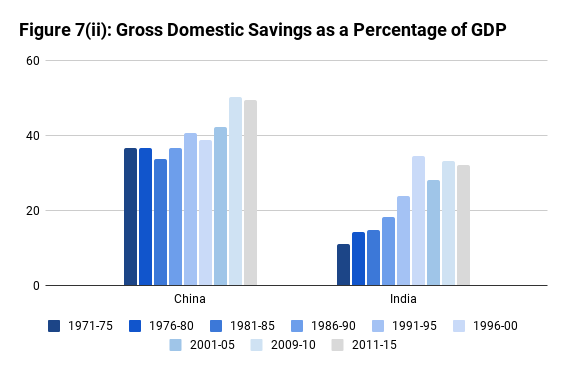

One of the stylised facts of modern economics is that no country has sustained 7–8% annual output growth without attaining steadily rising saving and investment rates close to 40% of its GDP. This is best illustrated by China’s experience.

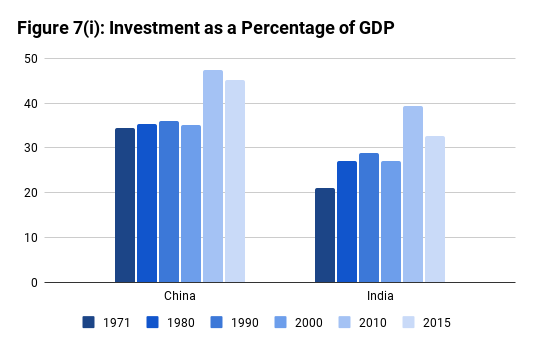

Figures 7 (i) and (ii) show the long-term comparative trends in saving and investment rates in China and India from 1971 to 2015. In 2021, as per the CEIC data, investment to GDP ratios in China and India were 43% and 32.8%, respectively. Likewise, savings to GDP ratios in China and India in 2021 were 45.9% and 28.2% respectively. If recent experience is any guide, it would be wishful to expect India to get back to a sustained 7–8% annual output growth rate (recorded during the 2000s) – and to undo deindustrialisation – without raising these ratios close to the Chinese level.

To be sure, policymakers are conscious of the need to step up not just the investment rate but also the public sector component of it, as evident from recent budgetary statements of the union finance minister. Public investment in infrastructure and public goods, in theory, is expected to 'crowd-in' or 'pull-in' private investment to raise the aggregate investment rate when the economy is operating well below its full capacity. However, the possibility of a rise in interest rates for the private sector would be limited as there would be a slack in aggregate demand, especially investment. But there is little evidence to show that the pious intentions have been translated into tangible policy actions. We document the trends and composition of capital formation during the 2010s to draw attention to the gravity of the situation.

Never in the last seven decades has India witnessed such a sharp reversal of ... crucial macro aggregates.

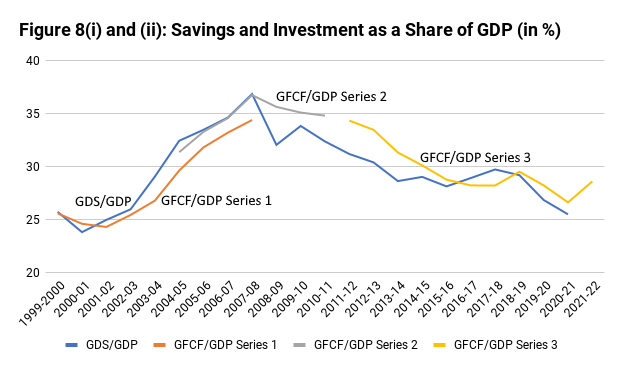

Figure 8 (i) shows that the gross fixed capital formation (GFCF) to GDP ratio at current prices had risen to 36.7% in 2007–08 from 26.6% in 1999–2000, a 10 percentage point rise in just eight years. (Interestingly, the ratio at constant (2011–12) prices shows a mild upward trend, suggesting that in real terms the fixed investment is more valued since the relative prices of manufactured products that go into capital formation have declined. However, over the decade, the decline in the ratio still holds.) This was also the period when the annual output growth accelerated to 7–8%.from 5.5–6%.

However, in the next decade, that is, the 2010s, the trend was reversed. The same holds for the gross domestic savings to GDP ratio (Figure 8 (ii)). Never in the last seven decades has India witnessed such a sharp reversal of these crucial macro aggregates.The RBI’s Report on Currency and Finance, 2022 has the relevant long-term data since 1950, confirming the foregoing observation.

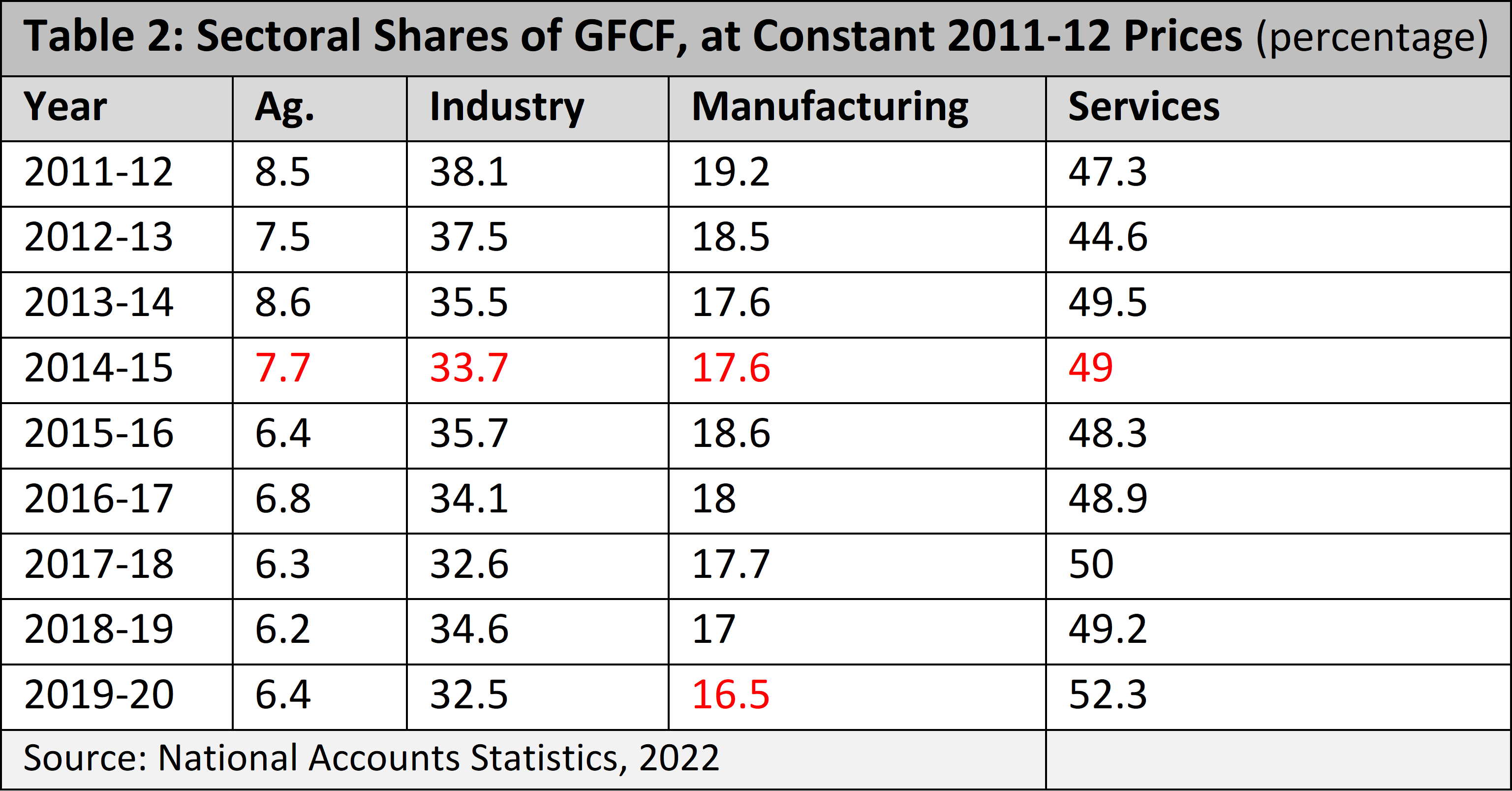

Table 2 reports the distribution of fixed investment by major sectors between 2011–12 and 2019–20. Evidently, the shares of agriculture and industry – and manufacturing within industry – have declined and the share of services has gained. Notably, the manufacturing sector’s share in the total declined by 1.7 percentage points between 2014–15 and 2019–20, suggesting the reason for deindustrialisation. This decline also tells us perhaps that the Make in India campaign, launched in 2014, failed to take off. (For a preliminiary analysis of the reasons for this failure, see Nagaraj (2019)).

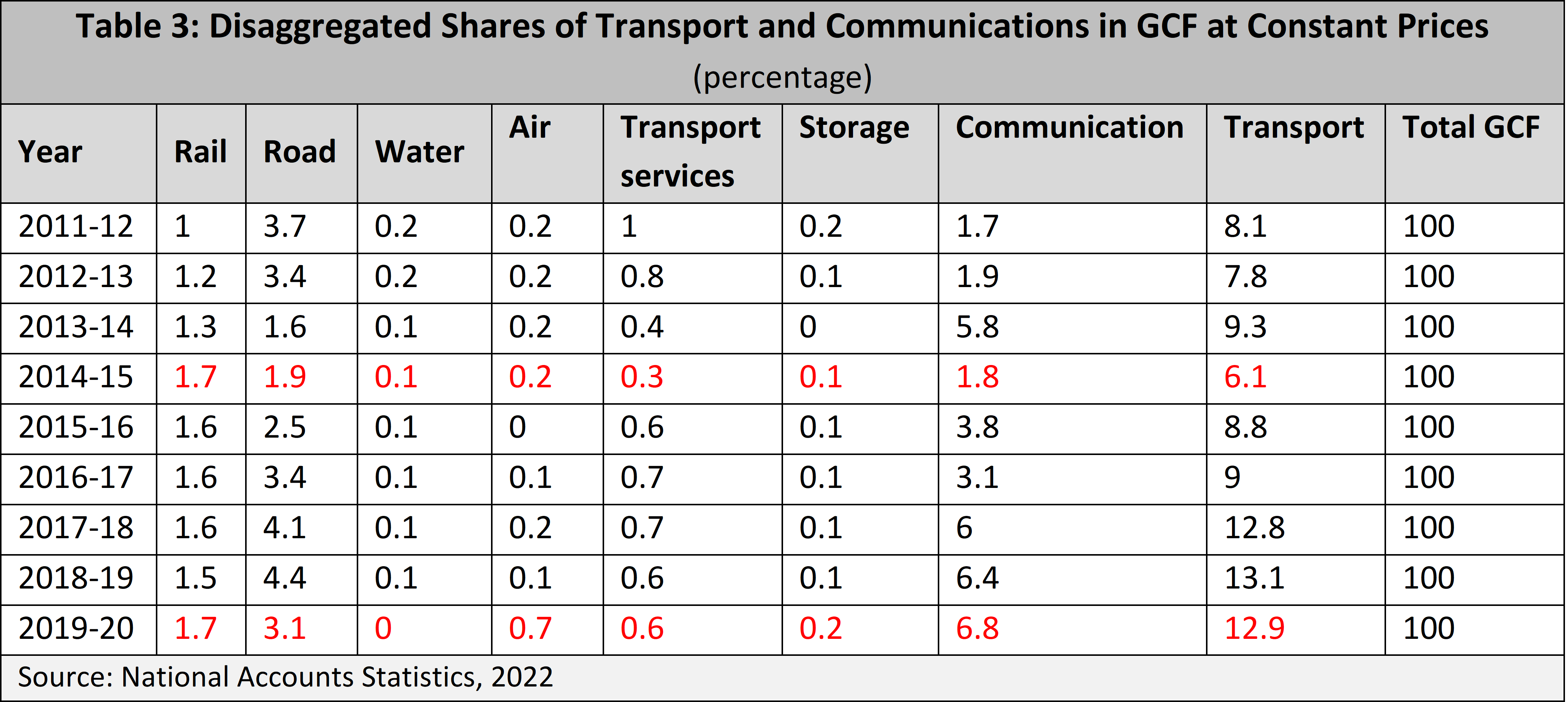

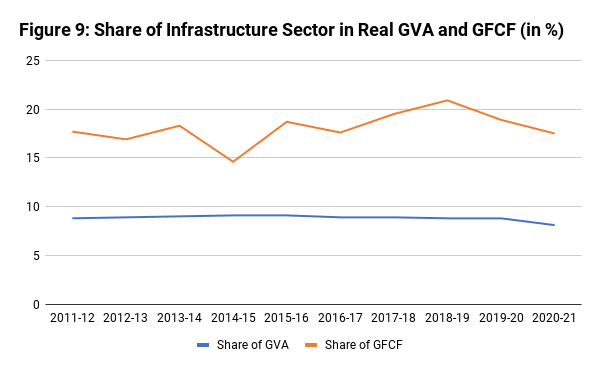

Table 3 reports further disaggregation of the GFCF to GDP ratio for services. The only sectors that gained shares were transport and communication. Within transport, it was mostly roads. Surely, these are crucial infrastructure warranting investments. But such a disproportionate boost while neglecting others such as railways or waterways, is a sign of lopsided development. Sudhanshu Mani, the head of the team that created the Vande Bharat train set at the Integral Coach Factory (ICF), Chennai, in a recent interview said that the train's true potential is not being exploited for lack of high quality rail tracks, which requires substantial investment. Likewise, within roads, overemphasising national highways while neglecting state roads or village roads (under the Pradhan Mantri Gram Sadak Yojana or PMGSY) indicates a skewed priority.

If, such “unbalanced investment growth” filled critical gaps to boost the overall supply of infrastructure, such investments could well be justified. However, surprisingly, the skewed investments in highways and communications do not seem to have augmented the overall share of infrastructure in GFCF or its output growth rate during the 2010s, according to RBI estimates (Figure 9).

While it is recognised that fixed investment rates have to be raised, a similar concern seems missing for the falling aggregate saving rate. There could perhaps be theoretical reasons for it. Arguably, the inflow of foreign capital in an open economy could make up for the lack of domestic savings because the economy could gain from abundant international capital available at low-interest rates (following Ben Bernanke’s “saving glut” hypothesis). But such benign neglect of a domestic savings economic policy seems to ignore historical facts and their underlying analytical considerations. Feldstein and Horioka (1980) demonstrated that despite open capital markets, savings and investment rates across the advanced European economies are highly correlated, implying that domestic savings influence domestic investment rates. The association has not weakened with the recent episode of financial globalisation.

Historically, during the phase of rapid growth and catching up of late industrialising economies, foreign capital inflows at best supplemented domestic savings, but were not a substitute for it. To illustrate, during the boom of financial globalisation (2001–08), the share of foreign direct investment (FDI) in domestic capital formation amongst 14 major Asian economies was, on average, a mere 7.4% (Nayyar 2019). Moreover, it is a historical fact that the real cost of foreign capital, adjusted for risk premium and exchange rate depreciation, tends to be higher than domestic savings.

Foreign capital inflow

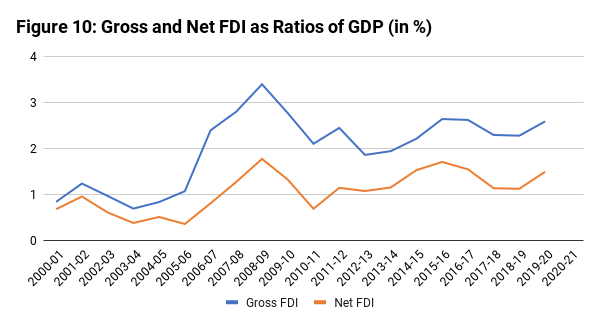

In the light of the foregoing, it is instructive to look at foreign capital inflows since 2000 when India embraced financial liberalisation. FDI and foreign portfolio investment (FPI) inflows, as ratios of GDP, steadily rose till 2008, and declined after that. In absolute size, yearly FPI inflows are less than FDI inflows, with greater (expected) volatility. The yearly FDI inflow has remained a modest proportion of GDP, peaking in 2008 at 3.4% and steadily sliding down to around 2.5% in the 2010s (Figure 10).

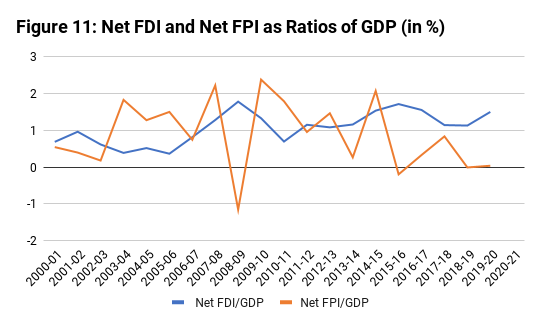

A widening gap between gross and net FDI inflows is discernible, with the repatriation of capital on account of the exit of private equity (PE) investments, reinvested capital, and outward FDI accounting for the gap. As Figure 11 shows, the net FDI to GDP ratio remained between 1% and 2% without an upward trend in the 2010s, and the net FPI to GDP ratio declined almost to zero by 2019–20.

In principle, FDI consists of greenfield investments in factories and firms bringing in much needed capital, technology, and managerial practices, which are not easily reversible. The reality is different, however. FDI inflows increasingly consist of PE and venture capital. Wikipedia defines PE as follows, “In the field of finance, the term private equity (PE) refers to investment funds, usually limited partnerships (LP), which buy and restructure financially weak companies that produce goods and provide services. A private equity fund is both a type of ownership of assets (financial equity) and a class of assets (debt securities and equity securities), which function as modes of financial management for operating private companies that are not publicly traded in a stock exchange.” They are internationally classified as loosely regulated alternative investment funds.

The Securities and Exchange Board of India (SEBI) defines alternative investment funds as any fund established or incorporated in India which is a privately pooled investment vehicle that collects funds from sophisticated investors, whether Indian or foreign, for investing it by a defined investment policy for the benefit of its investors, which exit after three to five years by selling their stakes in stock markets.

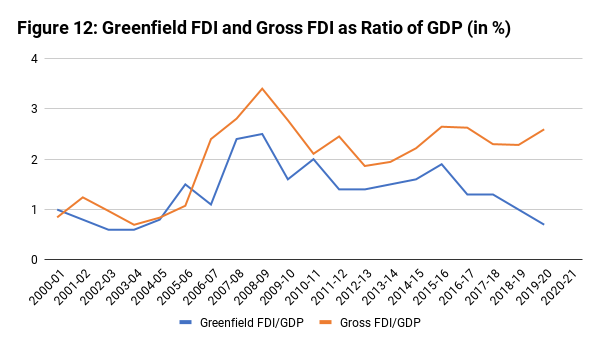

Such funds, by definition, do not undertake greenfield investments but acquire stakes in existing firms, factories, and brands. For instance, Blackstone, during 2019–21, invested $8.4 billion in information technology/information technology enabled services (IT/ITES) in 17 companies such as Hexaware, PGP Glass, ASK and so on with an average deal size of $485 million. In theory, PEs bring with them ideas and expertise to turn around underperforming enterprises to boost their market valuations. However, such a benign view of PE investment seems questionable. PEs are often accused of resorting to asset stripping and retrenchment of workers to boost stock valuations. Their profits are said to be mainly the result of differential taxation and opaque accounting rules, not open to public scrutiny as they are lightly regulated financial entities. Hence, the positive externalities of such brownfield investments of medium-term duration for the economy seem limited, compared to greenfield investments (See Manjoo, 2022)

For India, there is no official data on venture capital (VC) and PE inflows. VC funds and PE firms such as Bain and Company publish annual reports in which data for the two streams of inflows seem combined. We define, as a first approximation, greenfield investment as gross FDI inflow minus the sum of VC and PE funding. VC and PEs now account for about 70% of annual FDI inflows (from about 20% in two decades ago), and their share has steadily risen over the last two decades (Figure 12). The social benefits of such forms of foreign capital seem questionable.

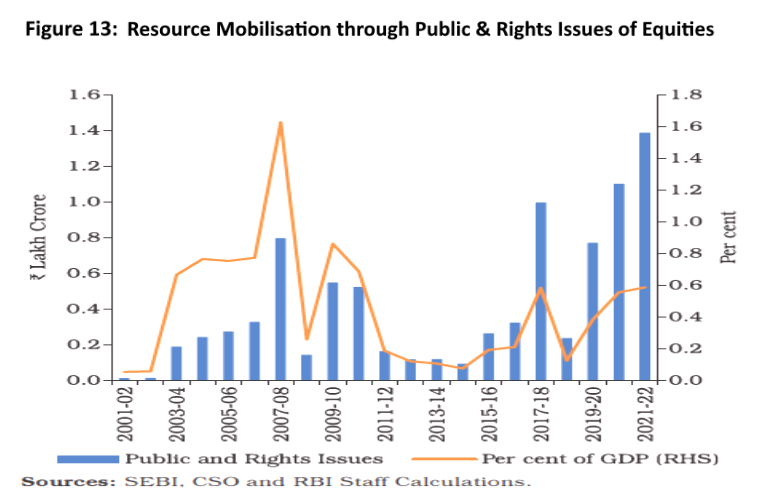

Another source of recent official and public optimism about investment growth is the unprecedented primary stock market resource mobilisation via initial public offerings (IPOs): Rs 150,484 crore in 2021–22 (Figure 13). However, the capital raised, as a ratio of GDP, is modest at 0.6%. The ratio is just about a third of what was recorded in 2007–08 at 1.7% of GDP. Unlike in the 2000s, the recent boom did not contribute to raising capital formation. The raising of capital perhaps stoked stock valuations in the secondary market, enabling private equity investors to quit their positions for greener pastures with hefty profits.

This evidence portrays a grim picture of the investment scenario. Nevertheless, policymakers seem optimistic about start-ups delivering potentially high returns based on technology and innovation and creating long-term value for the economy.

"A start-up is a company or project undertaken by an entrepreneur to seek, develop, and validate a scalable business model. While entrepreneurship refers to all new businesses, including self-employment and businesses that never intend to become registered, start-ups refer to new businesses that intend to grow large beyond the founder. In the beginning, start-ups face high uncertainty and have high rates of failure, but a minority of them do go on to be successful and influential. "

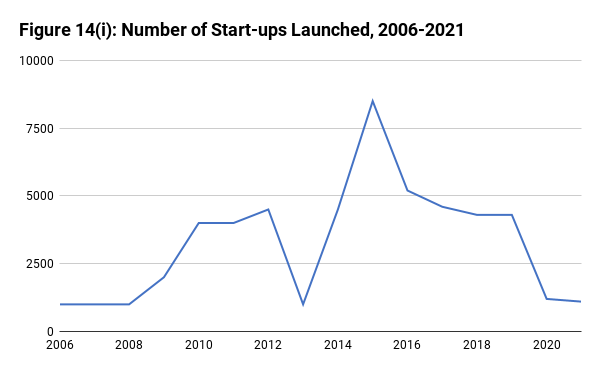

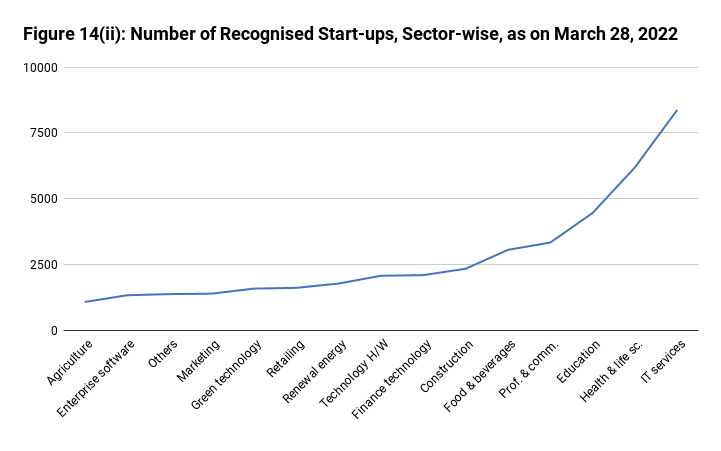

Figures 14 (i and ii) provides the official data on the number of start-ups and their industrial composition since 2006. It shows that their number peaked at 8,500 in 2015 and declined to 1,000 in 2021. However, the quantum of funding secured by start-ups peaked in 2021 (Jayram 2022). Most of the start-ups are engaged in skill-intensive IT and related urban services and very few are in manufacturing.

Incentives for PEs and VC funds, which finance start-ups, to invest in emerging market economies are closely tied to conditions in the global financial markets. Hence such investors tend to have shorter time horizons. When capital is abundant and global interest rates are low, PEs and venture funds tend to flood India (and many emerging market economies) to bet on risky investments – ready to “burn cash” (to use the industry jargon). But when market conditions change, they quickly exit the start-ups, leaving them high and dry, as we are currently witnessing after the US Fed began raising interest rates (Saroy et al 2023).

Evidently, for a largely poor and informal economy, the social value of such services is likely to be marginal as they mostly cater to wealthy urban consumers. Moreover, the global experience calls for tempering expectations about start-ups’ success.

Policy options

India’s accelerating growth path since the 1980s was derailed in the 2010s with a growth reversal on a trend basis. It has been accompanied by a contraction of domestic savings and fixed investment rates, something not seen since Independence.

There seems to be an urgent need to raise the domestic saving rate. Industrial and infrastructure investments require long-term, low-interest capital because such investments yield low rates of private return over a long period. Commercial banks mobilise domestic savings from the household sector and invest in the private corporate sector and government. However, there is a maturity mismatch as bank deposits are for the short to medium term while these investments require long-term capital.

Historically, publicly owned/sponsored long-term saving institutions such as provident and pension funds or post-office savings instruments performed such a function. State-funded or supported development financial institutions acquired these investible resources to channel them into long-term projects with high social returns. The most successful industrialising countries of Asia broadly followed such a pattern of financing (often called a bank-centric financial system), until liberal economic reforms consciously sought to move them towards a stock market-centric (Anglo Saxon model) financial system. India perhaps needs to reconfigure its bank-centric model to fund long-term investments (Nagaraj 1997b). The recently constituted New Development Bank, a move in the right direction, is yet to take off.

Financial inclusion efforts such as zero-balance bank accounts and the Jan Dhan Yojana are mostly perceived as a means of providing direct benefit transfers (DBT) or improving people’s access to bank credit. They are not perceived as a means of mobilising household resources to raise domestic savings and channel them into long-term investment. Though financial inclusion has merits, it is worth recalling that the expansion of the bank branch network in the 1970s after bank nationalisation in 1969 was a very successful move that raised the domestic saving rate (Authukorula and Sen, 2002). The rise in public resources contributed to an expansion of bank credit to finance the Green Revolution and contributed to long-term poverty reduction. To reverse the decline in the aggregate saving rate, there is a need to rethink how the expansion of banking habits amongst the poor can be redesigned with suitable incentives to mobilise domestic savings.

Case for public investment

The public sector now contributes about 20% of domestic output and gross capital formation. Private investment is roughly equally divided between the private corporate sector and the informal or unorganised sector (including agriculture). The decline in the private corporate sector’s investment after the global financial crisis was majorly responsible for the decline in the aggregate investment rate during the 2010s. Large-scale investments made during this period did not fructify as growth slowed down domestically and world trade decelerated. As domestic demand contracted, revenue streams for the private sector thinned down, and their ability to repay bank credit was impaired, turning such loans into the banking sector’s non-performing assets (NPAs).

While there could be valid arguments of malfeasance and crony capitalism in large-scale bank lending to politically connected companies and business groups, such an explanation would perhaps be incomplete if the changed aggregate economic and international conditions are overlooked (Nagaraj 2013). The problem of NPAs was accentuated because a stricter classification of them was followed since 2014, intended to 'clean up' the banking system. Efforts to resolve the NPA problem by creating an Insolvency and Bankruptcy Code (IBC) in 2016 have met with limited success, thus prolonging the slowdown in bank credit to the private corporate sector.

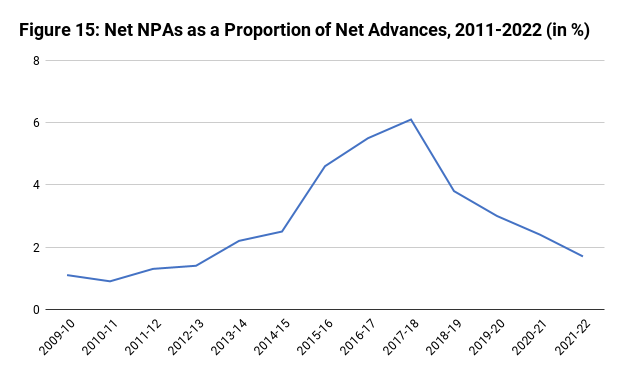

However, over the last five years, the government has written-off substantial NPAs. Net NPAs to net advances have come down sharply (Figure 15), making banks’ balance sheets look healthier. Though overall credit has expanded lately, the share of industrial credit in the total continued to decelerate from 2016 to 2022 for lack of adequate domestic demand and rising global uncertainties.

Considering all this, there seems to be an urgent need to step up public investment in specific sectors to reduce import dependence, to restore the private sector’s confidence, and for strategic considerations. Such a commitment to public investment-led growth – in a global situation of impending recession in about half of the world economy, according to the IMF’s latest prediction – could crowd in private investment to stimulate a virtuous growth cycle. In this context, India’s growing dependence on Chinese imports and deindustrialisation warrant careful consideration.

However, such reasoning is often resisted on the grounds of lack of fiscal space, which appears a specious argument. If additional government borrowing breaches fiscal deficit limits and is fully earmarked for capital formation targeted at reducing imports, inflation would be limited as it would be self-liquidating over the medium term as domestic supplies improve. Moreover, as price rise hurts the poor more, they could be insulated by a commitment to extend public distribution or use the open market for the sale of food grains to tame inflation.

If the additional borrowing is mostly in domestic currency, its spillover into the external deficit would be modest. Recent experience during the pandemic, especially from the US, demonstrated that if additional public expenditure is used for a targeted purpose, such as propping up private consumption, it effectively supports employment. Likewise, if the proposed additional public investment is productively deployed for expanding domestic supply to reduce imported goods, the additional debt could ease the balance of payment constraint and create jobs. However, realising such a positive outcome would call for a well-coordinated investment strategy. Responding to the pandemic and the urgency of developing suitable vaccines, the US administration quickly and effectively mobilised its national resources to pump resources to create the vaccines and make them available to its citizens in the shortest possible time. This was an example of how instruments of industrial policy can be mustered to meet national goals where speed matters. (See Adler (2021) for an account of the American effort.) There is perhaps a lesson for India in this on how to face the challenge of structural dependence on Chinese imports.

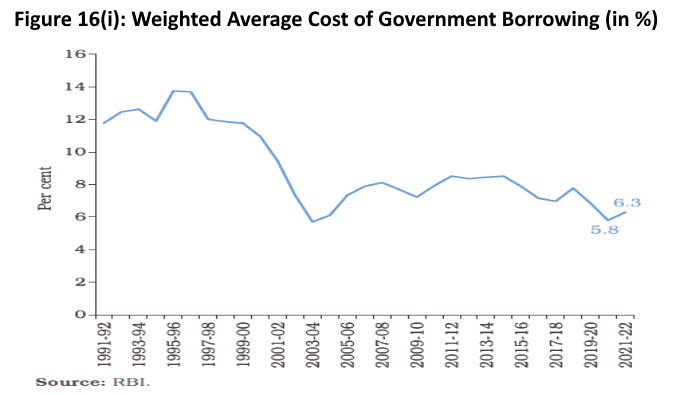

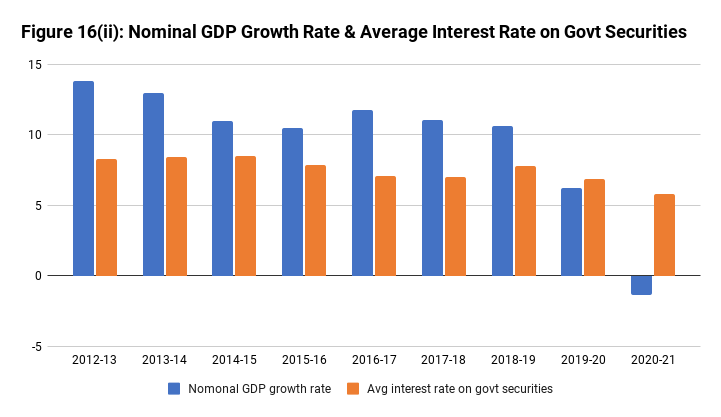

Figure 16 (i) shows that the cost of central government borrowing in nominal terms has steadily declined since the mid-2010s. And over the entire decade, the nominal GDP growth rate was consistently higher than nominal interest rates, implying that the additional public debt is sustainable, as per the Domar rule (Figure 16 (ii)). Evsey Domar famously said, “The public debt and its burden loom in the eyes of many economists and laymen as the greatest obstacle to all good things on earth. The remedy suggested is always the reduction of the absolute size of the debt or at least the prevention of its further growth. If all the people and organisations who work and study, write articles and make speeches, worry and spend sleepless nights – all because of fear of the debt – could forget about it for a while and spend even half their efforts trying to find ways of achieving a growing national income, their contribution to the benefit and welfare of humanity and to the solution of the debt problem would be immeasurable” (1944: 823).

Likewise, if domestic savings are augmented for investing in import-displacing industries and sectors, the burden on the treasury will be lower to that extent and it will also reduce the need for external savings to support the balance of trade. In other words, policymakers would need to be more creative in modifying the fiscal rules or redesign the rules to take care of public investment for a strategic purpose.

Conclusions

In 2021–22, India’s GDP, net of inflation, was marginally higher by 1.5% compared with 2019-20, that is, the pre-pandemic year. It means that the country recovered in a year from the economic contraction caused by the pandemic . It also means that India lost two years of output and employment growth, with the per capita income falling marginally. The human costs of the pandemic may have been substantial – probably much more than what the government cares to admit – but the quick recovery provided a welcome relief. The output rebound was respectable compared to, say, China, which is still grappling with its policy flip-flops.

Though the Covid-19 shock is now behind us now, the world economy is grappling with the Russia-Ukraine war and distinct signs of the end of globalisation as we knew it. The world economy is apparently fracturing along geopolitical fault lines, along axes reminiscent of the Cold War era. With its large domestic market, though at low levels of per capita income, India is perhaps better placed to cope with the possible de-globalisation.

The pandemic, unfortunately, deflected the public’s and policymakers’ attention from India’s decade-long economic slowdown. The country’s growth declined in the 2010s after it witnessed rising growth from the early 1980s to the end of the 2000s. If the doubts raised on the official GDP estimates are reckoned with, the average annual growth rate during the decade is probably 4.5–5%, compared to official estimates of more than 6–7% per year. The growth reversal has reverberated through the economy, resulting in adverse employment effects, and a rise in the levels of absolute poverty and malnutrition.

The decade-long growth derailment was accompanied by an unprecedented fall in the fixed investment and domestic savings rates as proportions of the GDP.

Despite all the public attention the Make in India and Atmanirbhar Bharat initiatives attracted, the manufacturing sector’s share in fixed investment has fallen, contributing to deindustrialisation. India’s import dependence, especially on China, for edible oils to electronics hardware has gone up for lack of domestic production capacity. The dependence is so structural that it is hard to correct quickly with the price mechanism alone. This is a serious strategic shortcoming the country faces, perhaps without appreciating its full implication.

Policymakers seem to be seized of the problem of a contraction in the investment rate. Recent announcements of large projects in the manufacturing sector to reduce import dependence (semiconductor chips, for example) and boost employment (Tata’s proposal to assemble iPhones as a contractor for Foxconn) seem to suggest an upturn in investment is coming. The falling NPAs of the banking sector could improve the supply of bank credit to industry.

However, the private sector still seems hesitant, given global geopolitical uncertainties and the lack of domestic demand. But with deindustrialisation and a structural dependence on China, the government cannot simply wait for the private sector to wake up. It will have to step up public industrial and infrastructure investment to create policy certainty for the private sector. Raising public investment without jeopardising the fiscal and external balances will require making efforts to raise the domestic savings rate and boost long-term financial institutions.

(This is a slightly edited version of the annual lecture delivered at the Telangana Economic Association in Hyderabad on 11 February 2023. The lecture was prepared when the author was a visiting professor at the Centre for Development Studies, Thiruvananthapuram.)

R. Nagaraj was earlier with the Indira Gandhi Institute of Development Research, Mumbai.